Paul Krugman has done a series of posts suggesting that recent policy announcements in Japan may have led to dramatically higher inflation expectations, and much lower real interest rates. I’d like to agree with him, but I’m having trouble processing some of the information. I hope to learn more by reading commenters’ reactions to this post. The first Krugman post noted:

And here’s an important point that has gone remarkably unreported, except on a few financial blogs: something dramatic does seem to be happening on the expected inflation front. Here’s the 5-year breakeven, the spread between indexed and non-indexed bonds:

. . .

The big move actually came before Abe took office, maybe reflecting the sense that the political environment had changed and that the Bank of Japan’s freedom to impose monetary orthodoxy was about to end. Whatever caused it, this is a remarkable change — it’s the kind of upward move in inflation expectations advocates of radical monetary policy in the US can only dream of. And coupled with a fiscal boost, it could mean that Japan’s long deflationary era is finally coming to an end.

There’s no maybe about it, the surge in the Japanese stock market and the big plunge in the yen began right when Abe announced he’d push for a 2% inflation target, well before the election. (It was mid-November.) But I don’t see a “dramatic” increase in 5 year inflation expectations in the graph he provides—just a modest boost that was even smaller than we got out of the various QE programs. Maybe I misread the graph, but it looks to me like inflation expectations rose by about 10 basis points between mid-November and today.

More likely, Krugman is referring to the nearly 100 basis point rise over the past 12 months. That is pretty large, although US TIPS spreads have occasionally moved by comparable amounts in recent years, but it doesn’t seem to be linked to either rumors about BOJ policy changes, or dramatic changes in the value of the yen (or Japanese equity prices.) The link between rumors of monetary easing and big stock/exchange rate moves is so obvious that I’m reluctant to attribute a big move in inflation expectations to policy changes, unless there is confirmation in other markets.

Please convince me I am wrong.

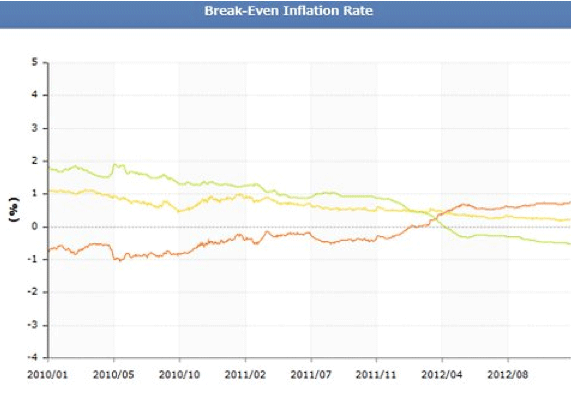

In the next Japan post Krugman provides this graph, using 10 year rates:

That data looks wrong to me. It seems to show 10 year Japanese bonds yields (yellow line) falling to about 0.25%, whereas they are actually over 0.80%. But is the nominal rate wrong, or is the breakeven inflation rate (red line) wrong? It appears to me that the nominal rate is wrong, as the other graphs Krugman provides suggest 10 year yields are near 0.80%, which is correct. In contrast, the inflation spreads seem right, as they are consistent with his other post, close to the 5 year spreads. But that means the real interest rate (green line) must be incorrect, it should be closer to zero.

Even stranger is the fact that the real interest rate estimates provided would be roughly correct for the US, where 10 year real rates have fallen from positive to significantly negative in the past year or two.

Putting aside the question of whether the real rate estimates are correct, what do we make of Krugman’s claim that easier money will reduce real rates, and not raise nominal rates? I have an open mind on this question. In the past I’ve seen easier money raise both real and nominal rates, but I don’t think it raises real rates all that often. The effect can depend on lots of factors, including whether the policy is a one time change, or expected to lead to permanently higher inflation and NGDP growth. With QE combined with IOR in the US there might also be a market segmentation argument. So Krugman might be right.

But I think it’s also possible he is wrong to get optimistic about the fall in Japanese real rates. (Never reason from a . . . ) David Glasner has talked a lot about the fact that the zero rate bound is a problem because it can prevent nominal rates from falling to equilibrium, and hence can hold real rates above where they need to be for macro equilibrium.

Now consider the fact that in the US the real yields on 10 year Treasuries has been on a downtrend since the early 1980s, from about plus 7.0% to negative 0.6%. That’s a huge drop, and it obviously is not all due to “easy money.” Indeed inflation has fallen sharply over that 30 year period, as has NGDP growth. Maybe the recent drop is easier money, that’s debatable, but surely not the entire 30 year downtrend.

Now consider that the reasons offered for lower trend real interest rates in the US, hold even more strongly in Japan, which is gradually dying out as a country. It’s very possible that the last 12 month’s worth of lower real yields on 10 year Japanese bonds in not easier money, but rather part of a long term trend similar to the US. If so, the zero bound problem might well get worse in the future.

The lower the equilibrium real rate, the higher the expected inflation rate required to keep (Wicksellian equilibrium) nominal yields above zero. If the equilibrium real rate falls to negative 1% on 10 year bonds, it’s probably even lower on short term debt. In that case even raising Japanese inflation from minus 0.3% to plus 0.7%, would do nothing but offset the fall in the equilibrium real rate, leaving Japan just as stuck at the zero bound as before, with the credit markets not able to reach equilibrium.

Just so I am not misunderstood:

1. I agree with Krugman that the modestly higher inflation expectations since November are policy related, and are good news.

2. I worry that the much larger fall in real rates over the past 12 months may reflect increasing pessimism about Japan’s long term equilibrium growth, and lower expectations of its long term equilibrium Wicksellian real interest rate. I hope I’m wrong. I hope it is due to expectations of stimulus. But we pretty much know that the recent big move in Japanese equities and the yen was driven by policy rumors, and yet the Japanese equivalent of our TIPS spread moved up only about 10 basis points on the news. That tells me that the markets are slightly more hopeful, but on balance are just as skeptical of Abe as Noah Smith.

PS. I do expect Japan’s birth rate to bounce back at some point, so the “dying out” comment should not be taken literally.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply