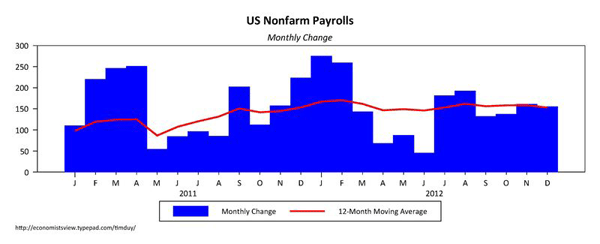

Employment Report for December 2012 nothing if not consistent.

On his Twitter account, Neil Irwin runs the numbers:

Consistency! Dec. payrolls (+155k); 3 mo avg (151k); 6 mo avg (160k); 12 mo avg (153k); 24 mo. avg (153k).

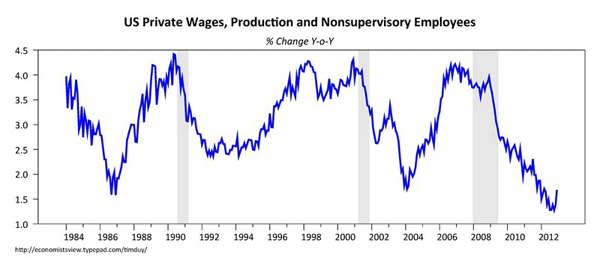

No exciting year-end ramp up like at the end of 2011, just more of the same. Something a little different, however, in the wage data:

Statistical bounce? Or evidence of enough improvement in labor markets that firms actually need to step up the pace of wage growth? I would certaintly see that as good news, although I will let the equity analysts puzzle over what that means for corporate margins.

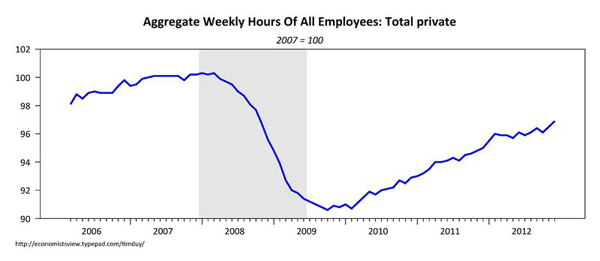

Aggregate hours worked made a healthly gain in December:

suggesting that the underlying economy continues to chug along at a moderate pace despite the ups-and-downs of quarterly GDP reports.

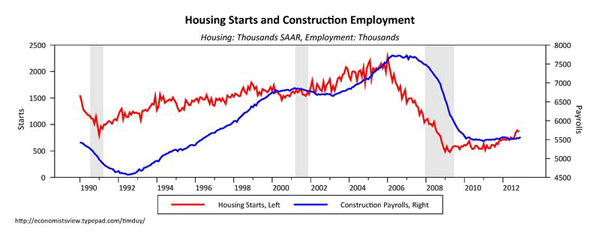

Construction gained 30k jobs. This may be a Sandy-related increase or, as some will suspect, a reflection of improving housing starts:

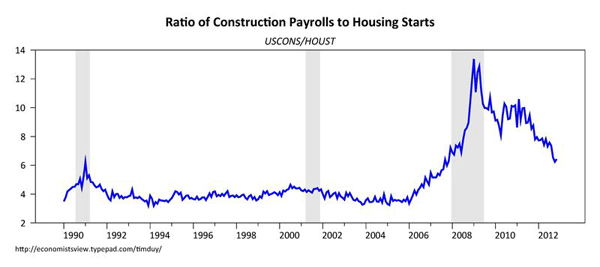

On the latter point, I would add that the construction sector still looks employee-heavy relative to the level of starts:

Prior to 2006, the ratio held remarkably steady at 4. This suggests to me that housing starts need to go higher until construction firms begin hiring more aggressively. Until then, expect firms to increase the hours of existing workers.

Manufacturing gained 25k, seemingly at odds with the softness of recent months reported by the ISM and core-manufacturing orders data. Professional and business services gained just 19k, with the subcategory of temporary help basically flat – is this where fiscal cliff angst impacted hiring? Education and health services had a solid, although expected, gain of 65k, leisure and hospitality gained 31k.

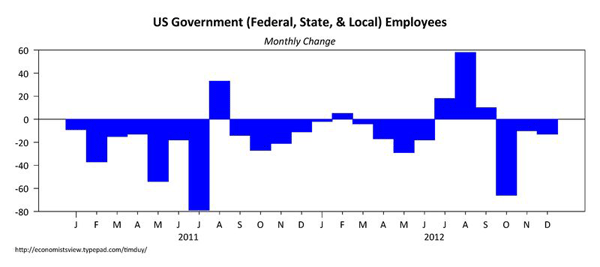

The government sector continued to shed jobs, loosing 13k employees, including 11.5k in local education:

There is some hope that the government sector offers more job support this year as state and local finances improve. I am skeptical that we get better than just holding steady on average. Anecdotally, local finances are still very tight. Although housing starts are increasing, in many cases the new construction won’t come on the tax roles for 9 to 12 months or longer. In addition, I suspect the first wave of revenue relief will end up in the pockets of public employees seeking to offset the weak wage growth of recent years.

The household survey details were not as strong as the establishment numbers, although differences between the two are not unusual. Employment grew by just 23k, while the ranks of unemployed gain by 164k. The labor force gained by 192k, leaving the unemployment rate flat at the revised November rate of 7.8%. The rise in the number of unemployed could indicate workers returning to the labor force, which would suggest improved confidence in the state of the labor market.

What does this report imply for the Fed? As it is largely consistent with past reports, it doesn’t seem likely to have immediate implications. Some were unsettled by this part of the most recent minutes:

In considering the outlook for the labor market and the broader economy, a few members expressed the view that ongoing asset purchases would likely be warranted until about the end of 2013, while a few others emphasized the need for considerable policy accommodation but did not state a specific time frame or total for purchases. Several others thought that it would probably be appropriate to slow or to stop purchases well before the end of 2013, citing concerns about financial stability or the size of the balance sheet. One member viewed any additional purchases as unwarranted.

The key part of this section is “considering the outlook for the labor market and the broader economy.” If you believe that although 2013 growth will on average be modest, but accelerate in the second half of the year, you might reasonably believe that job growth will accelerate as well. Moreover, it is reasonable to expect that the various financial and fiscal risks will ease throughout the year as well. If this is true, then the Fed will start easing back on the asset purchase program. This is especially true if the unemployment rate moves closer to 6.5%; they will want to be done with asset purchases prior to considering a rate increase. Of course, if none of this comes to pass – for example, fiscal multipliers are higher than anticipated and the economy continues to muddle along – then the Fed will continue asset purchases. As always, it is data dependent.

Bottom Line: The employment report is, on average, more of the same. Ongoing slow but steady improvement. The year-over-year gain in wages might be a precursor to a more positive dynamic in the labor market, but one month does not make a trend. In and of itself, the report is likely consistent with the Fed’s forecast, and thus not a motivation for an imminent policy change.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply