Well, it may (or may not) be the case that bonds are trading rich, but regardless, the valuation gap (insofar as it exists) remained wide open yesterday. Had Macro Man not unsuccessfully tried to call the top in equities more than once throughout the year, he’d be tempted to label yesterday’s price action as a classic blow-off high.

Low volume and a bearish candlestick on the index are ample reasons for caution. However, digging beneath the surface, it certainly appears as if the quality of the equity rally has deteriorated significantly. Among the top performers in US equity land, on on heavy volume to boot, were well-known turds Freddie Mac (NYSE:FRE) and Fannie Mae (NYSE:FNM).

Now it’s true that another turd, AIG (NYSE:AIG), has been enjoying a renaissance for a number of months now, much to Macro Man’s disbelief. But this month the Agencies are tracing out what appears to known in the trade as a “Lazarus” pattern, e.g. coming back from the dead.

Macro Man asked one of his banks, a US institution that is generally assumed to be extremely well-placed, WTF was going on with FNM and FRE. And the answer that he got virtually defied belief. To paraphrase, he was told that interest in these stocks is primarily driven by retail, who believe that the low share prices mean there is less downside and that the stocks have the furthest to rally.

Now, Macro Man doesn’t know if this explanation is true or not (any readers with more insight are encouraged to chime in!) But if it is, it must represent the apotheosis of stupidity as an equity investment strategy. And that is usually the sign of a market headed for a fall.

Beyond that, Macro Man cannot concerns over the divergences that he’s observing. Yesterday, he highlighted the divergence between a relatively bid fixed income market and equity strength. He was somewhat surprised to see bonds and front ends rally after the Bank of Israel hiked rates yesterday.

As far as he can recall, this is the first tightening by and central bank coming out the other end of the easing cycle. What made it particularly interesting is that a) the BOI adopted QE in February, b) BOI governor Stanley Fischer was at the Jackson Hole conference that seemed to adopt a “lowre for longer” consensus, and c) Fischer himself punches above the BOi’s weight, having held senior positions at the World bank and IMF.

Might this be a road map for a surprisingly early exodus from QE by more important central banks? Perhaps, but markets appeared to dismiss the possibility yesterday with a wave of the hand.

Closer to home (or at least, Macro Man’s book) has been the interesting and frustrating divergence between equities and other pro-risk assets such as emerging market foreign exchange rates. Ordinarily, one expects a strong negative correlation between Spoos and EMFX, and indeed that’s what’s been observed for most of the year, including this month. So what’s the problem?

Well, the issue is that return correlations capture the direction of daily moves without saying too much about their magnitude. And what’s been happening recently is that on the days when stocks do well, EMFX goes up a little, but when stocks go down, EMFX gets butchered.

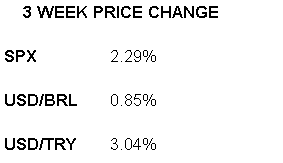

So while the 3 week daily return correlation between the SPX and USD/TRY and USD/BRL is somewhere around -0.8, the aggregate return to the friendly macro punter has been less impressive. Indeed, over the past three weeks USD/BRL and especially USD/TRY have both risen (i.e., the emerging currencies have gone down versus the dollar) even as the SPX has tacked on a 2% plus gain.

So in a sense, EMFX has given you none of the upside and all of the downside of a “risk-on” position. Great! At the same time, bonds have traded persistently bid, the Baltic freight index has been pummeled, and Chinese stocks have gone from rock star to reality-show reject.

Oh, and a strange bid has emerged for the worst of the worst of the US equity market.

Interesting divergences, to stay the least, particularly as we approach a period of seasonally poor performance for stocks. Perhaps this time, equities are “right” and everything else is “wrong.”

Then again, perhaps not……

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply