Yesterday’s statement from the FOMC, the decision-making body for the Federal Reserve, basically said that, yes, the economy has worsened since the FOMC’s previous meeting, but no, they’re not going to do anything about it. At least, not right now.

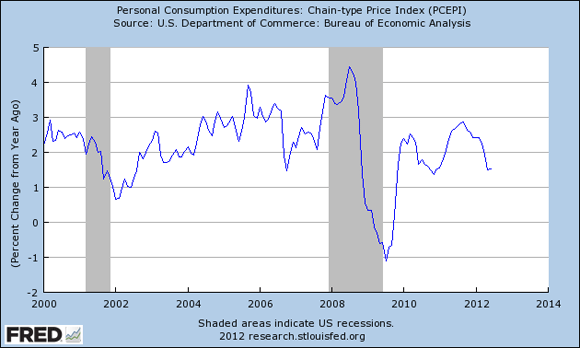

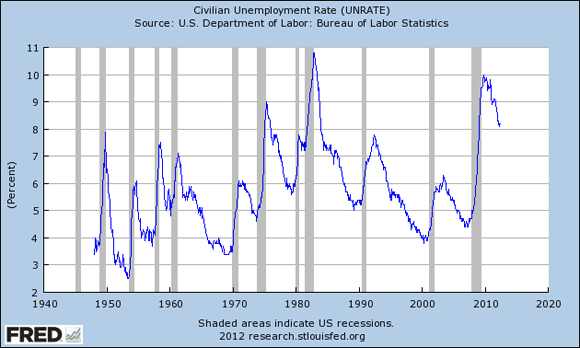

Over the longer run, the Fed says it is aiming for an inflation rate of 2% and an unemployment rate below 6%. Normally, the policy decision involves a short-run tradeoff between those two objectives. For example, if unemployment is much higher than the long-run target (as is the case right now), the Fed might tolerate inflation above target for a while in hopes of bringing unemployment down more quickly. But, as the numbers have been coming in for 2012, inflation is below target and unemployment is way above. That would seem to suggest the Fed would opt for more stimulus, end of story.

Year-over-year percent change in monthly PCE deflator. Source: FRED

Civilian unemployment rate. Source: FRED

itself was no rosy scenario). In those subtle changes in wording that Fed-watchers pore over, the Fed changed its statement to acknowledge directly that “economic activity decelerated somewhat over the first half of this year,” and “household spending has been rising at a somewhat slower pace.”

So why no new stimulus coming out of yesterday’s meeting? If we were talking about the historical operating environment in which the policy decision is whether the Fed should raise or lower the fed funds rate by another 25 basis points, there would be no question– yesterday the Fed would have delivered additional easing. But it is clear that the Fed sees the tools that it actually has available, namely more big purchases of Treasury or mortgage-backed securities, as measures that would have only modest stimulative effects but entail significant other risks.

Suppose we grant that assessment. Standard decision theory would still say the Fed should weigh those concerns, and operate at a point where the marginal benefit of additional easing equals the marginal cost. If the Fed had been operating at exactly such a point in June, and if changes in July brought inflation lower and unemployment higher than the Fed had been anticipating as of a few months ago, then they’d want to recalibrate at this time.

But the Fed has an additional policy objective– it wants to be very predictable about shooting its loud if not terribly effective guns. For purposes of that objective, waiting until the next meeting accomplishes two things. First, it gives FOMC members time to go on the road to send clear policy signals so that everybody knows what’s coming. Such a communication strategy also gives the Fed a chance to see the reaction in key markets such as sensitive commodity prices. Second, waiting another 6 weeks allows a little more data to come in to confirm how serious the summer slowdown really is.

It should become clear in the speeches we hear from FOMC participants over the next several weeks whether that’s the correct interpretation of yesterday’s announcement.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply