Some are greeting Friday’s employment report as an all-clear signal. But my advice is, keep your helmet on– they’re still shooting real bullets out there.

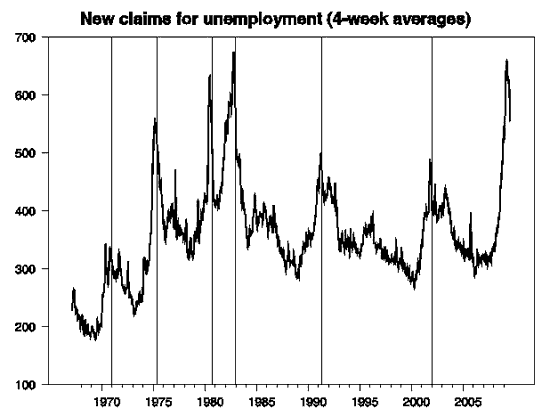

Let’s start with the good news. I first called attention to the favorable turn in new claims for unemployment insurance on April 9, noting that in each of the previous 6 recessions, an economic recovery began within 8 weeks of the peak in new claims. On May 7, I concluded we had enough statistical evidence to predict with 85% confidence that new claims for unemployment insurance had indeed peaked at the beginning of April. Although there was some concern as to whether seasonal adjustment could be confounding the July readings, it’s pretty clear now that the substantial decline in new claims is the real deal.

Black line: 4-week average of seasonally adjusted weekly initial claims for unemployment insurance, from Department of Labor via Webstract. Vertical lines mark the first month of an economic expansion as ultimately determined by the National Bureau of Economic Research.

And many cheered Friday’s BLS release showing that nonfarm payroll employment fell by 247,000 workers in July, the smallest drop since August, 2008. But the problem is, if a traditional economic recovery had actually begun in June (8 weeks after the April peak in claims), the number of people with jobs should have increased in July rather than fallen by another quarter million.

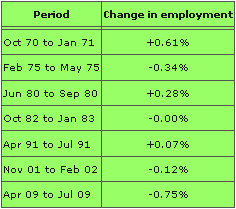

To put this in perspective, I took a look at where nonfarm payroll employment stood relative to where it had been at the time of the peak in unemployment claims for the current and each of the previous 6 episodes. I calculated the percentage change (measured as the change in the logarithm) in nonfarm payrolls between the month of the claims peak and the value 3 months later. To make sure we are looking at something comparable to the current real-time data available, in each case I used the figures as they would have actually been reported at the time (for example, the 2002 numbers come from the March 8, 2002 BLS release as reported by ALFRED). The current episode, in which employment has fallen by 0.75% since the April peak in new claims, is a clear outlier, even relative to the “jobless recoveries” of 1991 and 2002. President Obama had it exactly right when he declared, “As far as I’m concerned, we will not have a true recovery as long as we’re losing jobs.”

To put this in perspective, I took a look at where nonfarm payroll employment stood relative to where it had been at the time of the peak in unemployment claims for the current and each of the previous 6 episodes. I calculated the percentage change (measured as the change in the logarithm) in nonfarm payrolls between the month of the claims peak and the value 3 months later. To make sure we are looking at something comparable to the current real-time data available, in each case I used the figures as they would have actually been reported at the time (for example, the 2002 numbers come from the March 8, 2002 BLS release as reported by ALFRED). The current episode, in which employment has fallen by 0.75% since the April peak in new claims, is a clear outlier, even relative to the “jobless recoveries” of 1991 and 2002. President Obama had it exactly right when he declared, “As far as I’m concerned, we will not have a true recovery as long as we’re losing jobs.”

Jeff Frankel is cheered that the BLS index of the total number of hours worked held steady in July. That’s better news than if hours were still dropping, to be sure, but it’s far from enough to convince anybody that the tide has really turned if they weren’t already sold on the conclusion; see also Dean Baker on that ever-pesky seasonal adjustment issue.

Source: FRED.

Perhaps the loudest cheering over the BLS report was because the unemployment rate improved from 9.5% in June to 9.4% in July. But let’s look at how the net flows behind that calculation break down. The BLS only counts you as “unemployed” if you both (1) don’t have a job and (2) have taken active steps within the last 4 weeks to try to find a job. According to the household survey from which the unemployment rate is constructed, there were 155,000 Americans on net who quit or lost their jobs in July but didn’t immediately look for a new job, so those people newly without jobs don’t contribute positively to a higher unemployment rate. And 267,000 Americans who reported themselves to be unemployed in June still weren’t working in July but had also stopped actively looking for a job, so they’re no longer counted as unemployed. That last development is the reason the unemployment rate went down. But given the current environment, it’s hardly appropriate to interpret the fact that many people have simply stopped looking for jobs as reflecting an improving economy. Unless we get much better employment reports in September and October than we did in August, the unemployment rate is sure to climb back up.

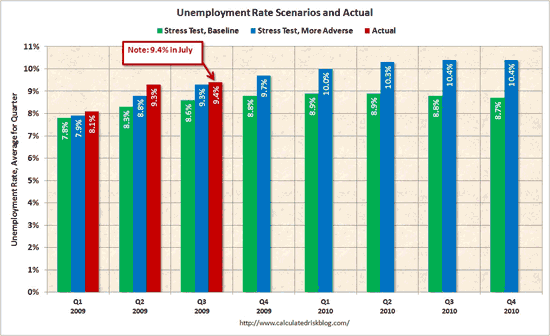

Rising unemployment could mean more foreclosures and bankruptcies, putting new stress on financial institutions. Calculated Risk notes that even the increases we’ve already seen put us above the “more adverse scenario” from the recent stress tests.

Source: Calculated Risk.

So party if you feel like it. The popular meme that the recession is now over could ultimately prove to be correct.

But it’s by no means guaranteed.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply