Since the launch of the Euro, there has always been a question about the benefits that Germany could enjoy of sharing a currency with other countries. While for the other countries (the “periphery”) the benefits in terms of credibility and stability of a strong currency were obvious, for Germany the benefits were simply the additional trade integration that the Euro would produce. Some believed that this benefit was too small to compensate for the potential risk of being part of a club with riskier countries. The current crisis has provided arguments for those who believed that Germany should have never been part of the Euro.

There is, however, a different perspective of the first 12 years of the Euro when looking at the performance of the German economy. During those years Germany managed to engineer a reduction to its relative labor costs that paid off in terms of increasing exports, a large surplus in the current account and faster GDP growth. A model that some see today as an example for others to follow. As Paul Krugman has pointed out several times, this model cannot work for everyone, not all countries can run current account surpluses!

In his most recent article Paul Krugman argues that the current German model needed the Euro to work. Germany had tried to keep labor costs under control in the past but without success. The launch of the Euro locked the exchange rate and sent capital flows to the periphery producing inflation in those countries. Even if German inflation was still positive (so no painful disinflation), there was an inflation gap with others, one that allowed Germany to be more competitive as the periphery became less competitive.

Quoting from Krugman’s article:

“Or to put it differently: Germany believes that its successful adjustment was the result of its own virtue, but in reality it was successful in large part because of an inflationary boom in the rest of Europe. And here’s the thing: the Germans are now demanding that the European periphery replicate its achievement (and actually surpass it, because the required adjustment is much bigger) without providing a comparably favorable environment — they’re demanding that Spain and others do what they never did, which is deflate their way to competitiveness.”

The corollary of this argument is that Germany benefited from the Euro in a way that was not expected at the time when it was launched: by allowing an increase in competitiveness relative to the other Euro members.

I agree with this argument but I think that there is part of the story that is missing. Not all other members of the Euro area had high inflation. Let’s compare Germany to France.

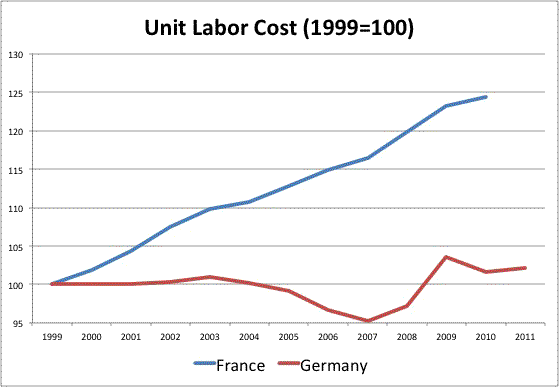

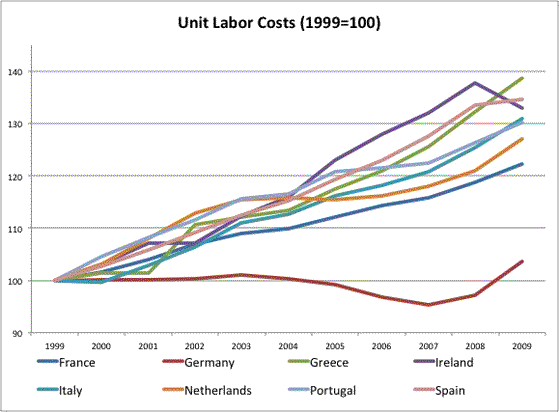

Since the launch of the Euro unit labor costs in France increased faster than in Germany. By the way, France resembles many of the other “periphery” countries in terms of unit labor costs, as I have discussed earlier. Here is the early chart.

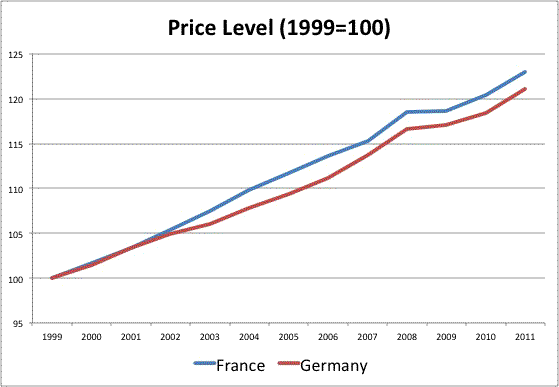

But France did not lose competitiveness through higher inflation. Prices in France and Germany behaved in a similar way, there was no inflation gap.

So in the comparison between France and Germany the story above does not seem to work, adjustment did not come from inflation in other countries but by the relative control of wages in Germany (relative, of course, to changes in labor productivity and all of this relative to French wages). But here is where I the Euro could still have played a role: when Germany had its own currency, it was very difficult to engineer a “competitive devaluation”. Reductions in wages or prices could easily be compensated by a stronger currency (the German Mark). This might run contrary to our intuition that competitive devaluations are easier with flexible exchange rates. For a country very committed to keep inflation low and a strong currency, it is difficult to deliver a competitive devaluation through monetary policy. But once the exchange rate is fixed, a combination of control on labor costs and the inflation that was generated in some of the periphery countries finally allowed Germany to produce a reduction in unit labor costs and growth via expansion of exports. And that is how Germany benefited from the Euro.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply