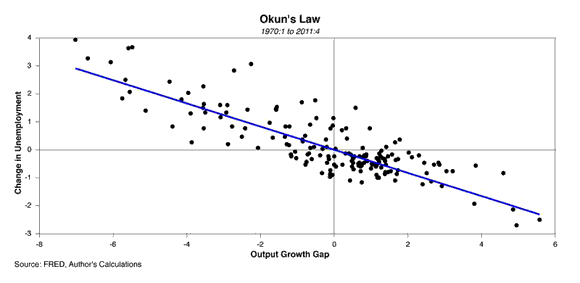

I have been thinking about Jon Hilsenrath’s article describing the breakdown of Okun’s Law. First off, consider the chart:

Note that while Hilsenrath describes Okun’s Law as the relationship between changes in the unemployment rates and the difference between actual and potential GDP growth, the chart that accompanies his article relates changes in unemployment rates and output growth. My chart illustrates the relationship between the year-over-year change in the unemployment rate (DIFFU) and the output growth gap (GAP), defined as the difference between the year-over-year changes in real GDP and and CBO potential GDP. The slope of the line above can be obtained from the regression equation:

DIFFUt = beta*GAPt

For the 1970:1 to 2011:4 sample, the slope (beta) is -0.41, suggesting that growth 1 percentage point in excess of potential growth yields a 0.4 percentage point decline in the unemployment rate. So far, so good. That said, even a cursory look at the chart will tell you that it would be a mistake to place too much weight on this relationship when considering near term forecasts. Observations are dispersed widely around the trend line; the R-squared is 0.71, leaving plenty of the change in unemployment unexplained by the output growth gap alone. Moreover, there are some curious points in the lower left-hand and upper right-hand quadrants which seem to be at odds with Okun’s Law. Indeed, the last two quarters of 2011 were such points, with unemployment falling despite output growth just below potential growth (year-over-year basis).

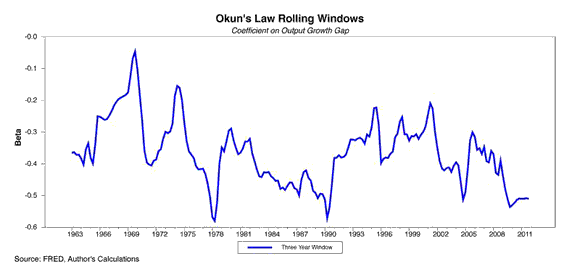

This suggests to me that Okun’s “Law” might break down on a fairly regular basis, which would not be a surprise given short run variations in productivity and labor force growth. To get at this question, collect the estimates of beta from three-year rolling windows beginning with the 1960:1-1963:1 sample and ending with the 2008:4-2011:4 sample:

And that is what we call job security for reporters and economists alike. The sensitivity of unemployment to the output growth gap ranges from almost 0 to almost -0.6, with recent estimates at the low end. Indeed, in the past few years, changes in unemployment have become more sensitive to the output growth gap. That said, how much should weight should we place on this deviation? After all, at something closer to business cycle frequencies, we can discuss the “breakdown” of Okun’s Law every few years as productivity fluctuates with the business cycle.

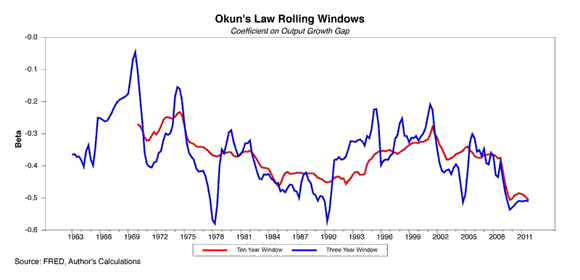

What about a longer estimation period that smooths the cyclical variation? Consider a ten-year rolling window:

As one might expect, the range of estimates is much more narrow. But still, the ten-year estimates following the three-year estimates down in recent years. Maybe something more persistent is happening, with the sensitivity of unemployment to the output growth gap changing from -0.3 to -0.5 over the last decade, a record low at this horizon. And notice that estimates of beta at the three-year horizon were decreasing prior to the recession; maybe what happened during the recession was in part just the continuation of an existing trend? Perhaps this is additional evidence of a trend productivity slowdown underway (I hope to tackle this issue more later).

Will the old Okun’s Law soon reassert itself? I don’t know, but looking at the ten-year trend suggests that we could continue to see fairly solid job growth even in a environment of relatively tepid GDP growth.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply