The last few days have seen a number of reactions to St. Louis Federal Reserve President James Bullard’s recent speech, inflation targeting in the USA. Critical reactions came from Scott Sumner, Noah Smith, Mark Thoma, and Paul Krugman. I think so far the only real support for Bullard comes from David Andolfatto here and here.

Bullard was moving in this direction last month, but he really didn’t outline his thinking. Now he has, and sadly revealed that there really wasn’t that much thinking at all. Bullard attempts to argue against the “output gap” framework shaping monetary policy:

The recent recession has given rise to the idea that there is a very large “output gap” in the U.S. The story is that this large output gap is “keeping inflation at bay” and is fodder for keeping nominal interest rates near zero into an indefinite future. If we continue using this interpretation of events, it may be very difficult for the U.S. to ever move off of the zero lower bound on nominal interest rates. This could be a looming disaster for the United States. I want to now turn to argue that the large output gap view may be conceptually inappropriate in the current situation.

First off, Bullard just flat out does not understand the definition of potential output:

The key to the large output gap story is the use of the fourth quarter of 2007 as a benchmark for where we expect the economy to be today. The idea is to take that level of real output, assume the real GDP growth rate that prevailed in the years prior to 2007, and project out where the “potential” output of the U.S. should be.

Estimates of potential GDP are not simple extrapolations of actual GDP from the peak of the last business cycles. They are estimates of the maximum sustainable output given fully employed resources. The backbone of the CBO’s estimates is a Solow Growth model. So I don’t think that Noah Smith is quite accurate when he says:

So, basically, what we have here is Bullard saying that the neoclassical (Solow) growth model – and all models like it – are wrong. He’s saying that a change in asset prices can cause a permanent change in the equilibrium capital/labor ratio.

Bullard can’t be saying the Solow growth model is wrong because he doesn’t realize that such a model is the basis for the estimates he is criticizing.

Second, as as already been widely circulated, Bullard then attempts to use a demand side shock to justify his contention that estimates of potential GDP are too high:

A better interpretation of the behavior of U.S. real GDP over the last five years may be that the economy was disrupted by a permanent, one-time shock to wealth. In particular, the perceived value of U.S. real estate fell substantially with the 30 percent decline in housing prices after 2006. This shaved trillions of dollars off of the wealth of the nation. Since housing prices are not expected to rebound to the previous peak anytime soon, that wealth is simply gone for now. This has lowered consumption and output, and lower levels of production have caused a significant disruption in U.S. labor markets.

Follow the links above to Sumner and Krugman for rebuttals to this line of thought. Brad DeLong tries to give Bullard a little help by noting that the bubble may have influenced labor force participation rates, but DeLong also notes these are at best small and were not Bullard’s argument in any event. Bullard’s chain of thinking is not so sophisticated. Sure, you can argue that he does have labor in the equation:

I mentioned that a wealth shock significantly upsets labor market relationships. This is because output declines, so less labor is required. It takes a long time for those displaced by the shock to find new working relationships.

But again, this is a demand side story. If output were higher, then so too would be the demand for labor. Simply put, Bullard simply moves from the wealth effect to a drop in consumption, and assume that drop in consumption represents a shock to potential GDP, inexplicably confusing demand and supply.

I don’t think there is much of a viable defense of Bullard – he gets both the empirics and the theory wrong. He doesn’t attempt to define a change in the factors of production that would lead to a shift in potential GDP, nor does he attempt to argue that the estimates of potential GDP are wrong, either from a time series trend/cycle decomposition framework or a CBO Solow growth framework. But note that it gets worse when he extends his faulty logic to policy:

I have argued that the large output gap view may be keeping us all prisoner—tethering our expectations for output, in effect, to the collapsed bubble in housing. It is setting a very high bar for the U.S. economy, one that may not be appropriate given the nature of the shock that the economy has suffered. Importantly, it may influence the FOMC’s near-zero rate policy far into the future, since output is continually viewed as falling short of the high-bar benchmark.

But the near-zero rate policy has its own costs. If we were proposing to remain near-zero for a few quarters, or even a year or two, one might argue that such a policy matches up well with the short-term business cycle dynamics of the U.S. economy. But a near-zero rate policy stretching over many years can begin to distort fundamental decision-making in the economy in ways that may be destructive to longer-run economic growth.

In particular, the lengthy near-zero rate policy punishes savers in the economy…

According to Bullard, monetary policy is stuck at near zero-interest rates because of overestimation of the output gap, and as a consequence savers are suffering. First, if the output gap is smaller than estimated, or the economy outperforms, the Fed can change course and raise interest rates. They have only issued a forecast, not a commitment.

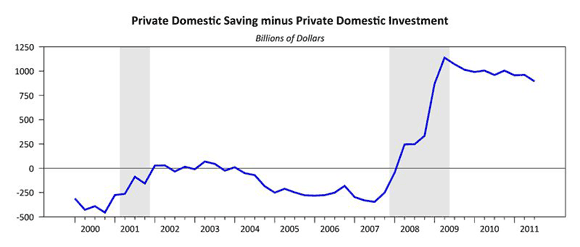

And, second, I have been through this before – while I am very sympathetic to the plight of savers, Bullard does not consider that the Fed is merely following the lead of the economy. Another way to think about the situation is that the supply of savings and the demand for investment currently would clear only at a negative interest rate – see Paul Krugman here. Also note the excess of private saving over private investment, which is exactly what you would expect if the market clearing interest rate was below the zero bound:

If the Fed’s zero-interest rate policy is leading to fundamental distortions in the economy, it is because the Fed is not taking seriously enough the need to lift the economy away from the zero-bound. And I don’t know that they can push the economy off the zero-bound if they limit their policy options with a strict two percent inflation target.

Bullard also shows significant sympathy for the notion that Fed policy is a net drag on activity:

These low rates of return mean that some of the consumption that would otherwise be enjoyed by the older, asset-holding households has been pared back. In principle, the low real interest rates should encourage younger generations to borrow against their future income prospects and consume more today. However, this demographic group faces high unemployment rates and tighter borrowing constraints, which may limit its ability and willingness to leverage up to finance consumption. Consequently, the consumption of the older generations may be damaged by the low real interest rates without any countervailing increase in consumption by other households in the economy. In this sense, the policy could be counterproductive.

If you truly believe this argument, then you must believe that a higher Federal Funds rate will have a net positive impact on output. But I have yet to see a convincing argument as to why this should be so – raising rates will only make matters worse if the market clearing rate is already negative. Note also that the ECB’s last two forays into the realm of tighter policy have not been particularly successful, to say the least.

Bottom Line: Bullard really went down an intellectual dead end last week. He criticized the focus on potential output, but revealed that he doesn’t really understand the concept of potential output either empirically or theoretically. He then compounds that error by arguing against the current stance of monetary policy, but fails to provide an alternative policy path. And the presumed policy path, tighter policy, looks likely to only worsen the distortions he argues the Fed is creating. I just don’t see where Bullard thinks he is taking us.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply