There was a period of time when I got stuck working on deal-teams that were trying to finance airlines. In corporate finance you usual work on a deal until it happens and then you move onto something different. Not the case with airline finance. These dogs always need more money. No one wanted to work on the deals (they were always shitty and very hard sells). The list of my “AAA” clients included: Eastern Airlines, TWA, and Continental Airlines. Two of my clients seized to exist; Continental went BK again and again.

This was in the 80’s when finance was not as sophisticated as it is today. But I tried to be creative. We hocked everything we could get a UCC filing on. Spare tires and parts (even used tools), engines so old they could not be used, landing rights and other things that had no real value. One of my highlights was when I financed the gangways that connected the planes to the gate.

Years later I got smashed in the head again when I got involved with a (very) failed effort to LBO United Airlines.

So add me to the long list of folks who have sworn off ever putting up a dime for the airlines. It’s one of the surest ways to lose money. My advice to anyone thinking of putting money to work in airlines is that before you write a check, hold your breath for three minutes. As (virtually) no one can do this, then no one would lose money in this cesspool. My investment rule works perfectly.

With that as an intro I take you to this article in the FT today:

The title says it all. No one should be surprised that the EU banks have turned off the spigot. They are all trying to broadly deleverage. They are already full up on dodgy aircraft paper. What I want to add is that the EU banks have been major providers of liquidity to the global air carriers for decades. The reason that I got involved with this mess was that I knew many European banks. They were all in love with high yielding asset backed lending. Airlines and the EU banks were a perfect match. That these banks are now out of the picture is a very big deal indeed.

A Boeing VP, Randy Tinseth, had this to say recently about those EU banks: (Bloomberg Link)

“There’s been a lot of concern in the market about the availability of capital, especially the situation with European banks.”

So what’s Boeing (BA) going to about the shortage of debt capital for the air carriers? Simple. They are going to take the paper right back on their books. From Commercial Chief Executive Officer, Jim Albaugh:

“Our strategy will be that Boeing capital will be much more than a lessor of last resort.”

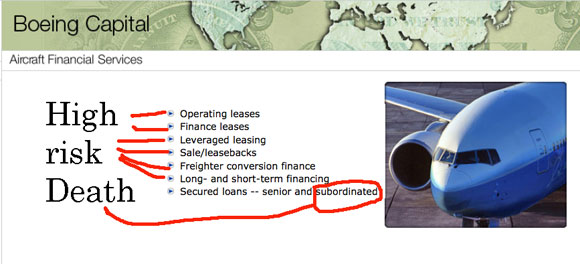

Oh boy! Look out! Boeing is going to be financing its own sales. (Just like GE does.) I looked at the Boeing Capital home page. This is a list of financial products the nice guys at BA are offering:

The first two categories are the safest of the lot. All the other stuff is very high risk lending. The last on the list, Subordinated Debt, has proven to be a guaranteed way to lose money.

It’s not that leasing (finance or operating) are without risks in this industry. The article that I quoted from is from November 13th, not a month ago. In that article the same Boeing Execs were crowing about their big success in leasing:

Boeing’s strategy to use its capital arm as a tool to gain an edge on strategic competitions was highlighted in July by an agreement with AMR Corp.’s American Airlines, where Boeing committed to providing 100 single-aisle jets to the airline on lease.

Well, 17 days later their best customer did a flame out:

Possibly Boeing Finance will end up doing better at this than I did. I doubt it. If they have any questions on where this strategy leads, they should ask Carl Icahn. He’s been bruised as much as anyone.

BA’s stock is at 14Xs earnings today, not so cheap at all. Possibly investors considering a punt on BA should hold their breath for 3 minutes. That 2.3% dividend everyone likes so much is not nearly enough to cover the risk.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply