When countries are members of a single currency are, such as the Euro, they cannot depreciate their currencies to boost their exports. The only way to produce the equivalent of a depreciation is to keep costs growing at a lower rate than other countries. This can only be achieved through wage moderation – not in absolute terms but relative to productivity growth. This is sometimes called an internal devaluation and it is normally thought as being more difficult to achieve than a straight devaluation or depreciation of the currency because it involves changes in wages. Many see this today as a challenge for Souther European countries as they might have been losing competitiveness relative to the other Euro countries and now they cannot just use their exchange rate to gain it back.

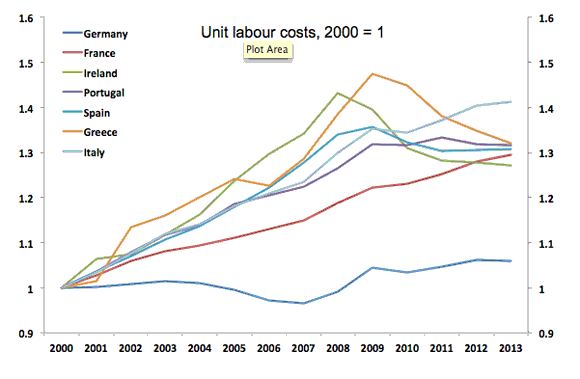

The recent OECD economic outlook talked about all this and had a chart that I am reprinting below.

The chart shows unit labor costs of selected Euro countries. The striking pattern of the chart comes from Germany. Germany managed to keep unit labor costs constant while all other countries in the chart saw increasing labor costs since the creation of the Euro. It is important to notice that this is not just about the usual suspects, France looks very similar to all the “club med” Euro countries. What is really remarkable is the behavior of Germany!

What I find interesting in this chart is that with the creation of the Euro, Germany managed to “engineer” such an increase in competitiveness while it did not manage to do it when it had its own currency. The German Mark, as any of the other large currencies in the world (the US dollar) fluctuated in directions that might not always have been in the interest of the country. In that sense, one could argue that Germany had a stronger control of its real exchange rate post-1999 than before. Of course we are talking about the intra-Euro exchange rate. Relative to the US, there is still an exchange rate that Germany cannot control: the Euro/Dollar. And this runs contrary to the way we normally think about exchange rates. It is when you control your own currency that we assume that you can better to influence your real exchange rate.

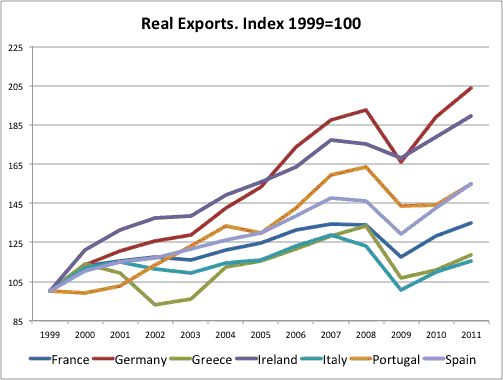

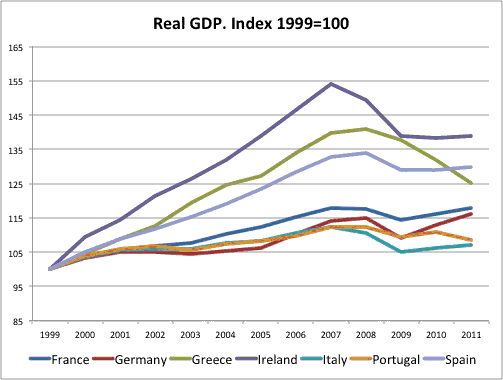

Just to complement the chart above, I produced two additional charts with the behavior of exports and GDP (both in real terms) during the same period. There are, of course, many other factors that affect these two variables but it is interesting to check what happened to both during the same years. Did Germany benefit from the behavior in unit labor costs?

When we look at exports we see that Germany did better than any of the other countries, although the behavior is not as extreme as one would expect from the behavior of unit labor costs. When we look at GDP then Germany is not an outlier at all and in fact it is one of the countries with the lowest performance during these years (only Portugal and Italy performed worse). There are reasons why we do not expect Germany to grow faster than the other countries (Germany has a higher GDP per capita than all of them) so the absolute comparison might be misleading but it still provides a sense on how the behavior of unit labor costs was reflected in economic activity and exports.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply