During the good years, the economic benefits of the common currency in Europe were fairly easy to recognize. The countries on the eurozone’s periphery — Spain, Portugal, Greece, and to a lesser degree Italy — had improved access to international capital markets, enjoyed lower borrowing costs, and experienced substantial investment booms as a result. Meanwhile, the countries in the eurozone core such as Germany, France, and the Benelux countries enjoyed a surge in exports to the rapidly-growing periphery. Importantly, they also enjoyed the higher returns that they could earn by investing in companies and projects in southern Europe. The gains from the common currency were shared by north and south.

Now, of course, Germany is pondering just how much it is willing to pay to keep the currency union intact. An important part of that calculation is an understanding of what the benefits to Germany were during the good years. There’s been some debate about that in recent weeks, for the most part focusing on whether and how much Germans benefited from the export boom of 2004-08. But another element of the calculation should be the higher investment income that German individuals and corporations earned from the new investment opportunities afforded by the common currency.

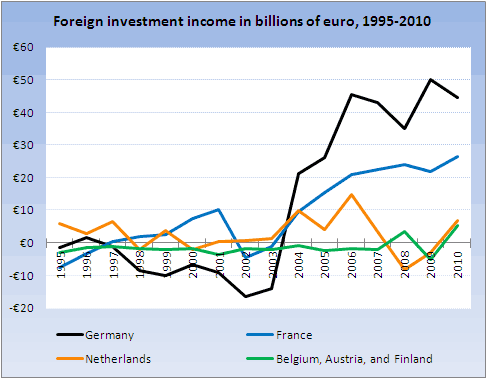

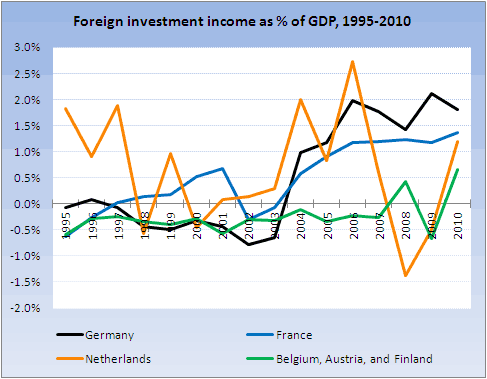

The following charts illustrate the surge in investment income earned by the core eurozone countries during the 2000s. The first expresses foreign investment income in billions of euro, while the second shows that income relative to GDP. (Data is from Eurostat.)

A couple of important caveats. First, this data is from national balance of payments statistics, which measures foreign income earned by each country from the entire rest of the world. We don’t have an easy way to directly measure how much of the increased investment income earned by these countries was specifically from the eurozone periphery. However, given everything else we know about the pattern of capital flows within Europe during that time, and the timing of the surge in investment income (the euro was adopted in 1999, and the boom really happened right after the economic slowdown of 2001-02 ended), it seems a safe bet that the much or most of this increased investment income was from southern Europe.

Second, we don’t know what the pattern of investment income earned by the core eurozone countries would have looked like in the absence of the common currency. In the absence of the counterfactual, we can only make an educated guess about the impact of the euro. In this case, however, I think there’s every reason to believe that the massive capital flows from core to periphery, the associated investment boom in the periphery, and the surge in investment income enjoyed by the core during the years leading up to the crisis would not have happened without the euro. I would therefore attribute the vast majority of the increased investment income earned by the core from the periphery during the 2000s to the euro.

Given that, this data suggests that the euro enabled Germany to enjoy increased investment income of perhaps €30 to €40 billion per year, or between 1% and 2% of GDP. The Netherlands also enjoyed an income boost of up to 2% of GDP during the best years of the 2000s, while the euro helped France to earn higher investment income equal to perhaps 1% per year.

Are these figures large enough to justify substantial additional spending by Germany to keep the eurozone intact? I have no idea. Keep in mind that this does not tell us anything about the economic benefits that the core eurozone countries enjoyed thanks to their increased exports to the periphery. And most importantly, the benefits of the common currency have always been perceived to be at least as much about politics as economics, and I’m not sure how we would go about quantifying those political benefits. But this sort of analysis does at least give us some rough sense about the magnitude of one specific type of benefit that countries like Germany and France enjoyed from the euro during the good years, and therefore puts a floor on our estimate of the overall benefits of the euro to those countries that are now considering whether to save it.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply