With European governments cutting back on spending, many are asking whether this could make matters worse. In the UK for instance, recent OECD estimates suggest that ‘austerity’ will lead to another recession, which in turn may lead to a higher debt-to-GDP ratio than before. As the debate heats up, this column provides some cool economic logic.

Could ‘austerity’ be self-defeating? Could a reduction in government expenditure lead to such a strong fall in activity that fiscal performance indicators actually get worse?

It is sometimes argued that a cut in expenditure (or an increase in taxes) would be self-defeating because it reduces demand so much that tax revenues fall so strongly that as a result the deficit actually increases. In standard models this is kind of ‘Laffer curve’ effect is actually not possible. Moreover, if it were true, it would follow that an increase in expenditure could actually lead to lower deficits because higher growth could increase tax revenues so much that they outweigh the increase in expenditure. This proposition has been tested several times in the US, and always found failing.1

Can austerity raise debt/GDP ratios?

In Europe the concern today is instead with the debt/GDP ratio. The perspective here is that ‘austerity’ might be self-defeating in the sense that the resulting GDP drop is so large that the debt/GDP ratio increases. This matters since the debt/GDP ratio is often taken by financial markets as an indicator of the sustainability. Thus a lower deficit might actually heighten tensions in financial markets.

Here I show that this sort of outcome could indeed occur, but only in the short run. Over the medium to long run, the debt/GDP ratio must improve even if deficit cutting lowers GDP. Anticipating the results of the reasoning, it can be shown in a standard model that in the short run a fiscal adjustment can be self-defeating if the product of the starting debt/GDP ratio and the multiplier (of fiscal policy on output) exceeds one. (See Annex for details.)

For example, this condition might be satisfied for countries with debt/GDP ratio higher than 100% if we believe certain ‘Keynesian’ models with fiscal multipliers that exceed one (ie the impact of higher expenditure on output is larger than the amount of expenditure itself). However, in most ‘neo-Keynesian’ models the ‘multipliers’ are often considerably lower than this. If these models describe reality better it is unlikely that austerity could be self-defeating – even in the short run.

Simple calculations

Here is how the short-run self-defeating mechanism could work. Assume Italy – with its debt/GDP ratio of 120% reduces its deficit by 1% of GDP by cutting public expenditure.

- If the multiplier is 1.5, the spending cut would lower GDP 1.5%.

- The GDP drop would – on its own – increase the debt/GDP ratio by 1.8 percentage points.2

But this is more than the reduction in the debt achieved directly by the cut in expenditure.

The long-run calculation is slightly more involved. There are two reasons for the general result that a fiscal adjustment cannot be self-defeating in the long run:

- First, most models assume that a cut in expenditure lowers demand in the short run, but that the economy recovers after a while to its previous path.

In this case, the debt/GDP will be lower in the long run since GDP returns to path but debt does not – it remains lower than it would have been without the austerity.

It follows that any short-run increase in debt/GDP due to the short-run fall in demand must be fully compensated in the long run. Therefore the long-run impact of a lower deficit on debt/GDP is equal to the reduction in the deficit itself.

- Second, assuming both the cut in public expenditure and its impact on GDP are permanent, debt/GDP must improve in the long run.

The basic point is simple. The permanent deficit cut lowers the growth rate of debt, while the permanent impact on GDP is of the path-lowering type, not the growth-lowering type. Thus any initial increase in debt/GDP will be reversed over time.

Of course an even more extreme version would have it that permanent deficit cuts reduce the long-run growth rate, but this is not a result found in even the most extreme Keynesian models.

Does the short or long run matter?

The key question in the context of the current Eurozone crisis is thus whether financial markets focus on the short run or long run. Prospective buyers of Italian one-year bonds should look at the longer-run impact of deficit cutting on the debt level, which is pretty certain to be positive. Of course, if markets are not rational and react only to the short-run effect the result might be different.

Policy conclusions

So what should governments do? Abandon austerity because financial markets might be shortsighted? This would only delay the day of reckoning as debt ratios would increase in the long run.

- A country which enters a period of heightened risk aversion with a large debt overhang faces only bad choices.

- Implementing credible austerity plans constitutes the lesser evil, even if this aggravates the cyclical downturn in the short.

All in all, the conclusion is that it difficult to argue that the peripheral countries in the Eurozone should abandon attempts to reduce their deficits because the results will arrive only in the long run (de Grauwe 2011).

References

•Acconcia, Antonio, Giancarlo Corsetti and Saverio Simonelli (2011), “What is the size of the multiplier? An estimate one can’t refuse”, Voxeu.org 4 April 2011, http://www.voxeu.org/index.php?q=node/6314

•Cogan, John, Tobias Cwik, John B Taylor and Volker Wieland (2009), “New Keynesian versus Old Keynesian Government Spending Multipliers”, NBER Working Paper Series No. 14782.

•Cwik, Tobias and Volker Wieland (2011) “Keynesian government Spending multipliers and spillovers in the Eurozone”, ECB Working Paper Series, No 1267.

•De Grauwe, Paul (2011), “Who cares about the survival of the eurozone?”, Centre for European Policy Studies, CEPS.

•Krugman, Paul (2011) “Self-defeating Austerity”, New York Times column, 7 July.

Annex: Simple formal analysis

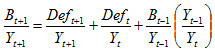

The dynamic connection between debt, deficits and GDP can be tracked using the debt stock identity: debt today equals the deficit plus the debt level yesterday.

(1) Debt = Deficit + Debt-1

where Debt and Deficit mean (respectively) the stock of government debt this period and this period’s deficit. The “-1” signifies the debt level in the period (year, month, etc.). To get Debt relative to GDP, we just divide both sides by GDP to get:

This is then divided by GDP to yield:

(2) Debt/GDP = Deficit/GDP + (GDP-1/GDP)(Debt-1/GDP-1)

but (GDP-1/GDP) is just the inverse of 1 plus the GDP growth rate, so the formula linking debt, deficit, growth is:

(3) Debt/GDP = Deficit/GDP + (Debt-1/GDP-1) /(1+g)

Assuming that the growth rate is directly affected by deficit spending, the impact of lowering the deficit has a good-news/bad-news effect. The good news is that the debt/GDP ratio falls directly with the deficit reduction. The bad news is that the austerity-induced slower growth means the denominator of the debt/GDP ratio rises less, so the ratio tends to rise. In symbols, the impact is:

The impact of a deficit on the debt ratio is thus given by:

(4) Change in (Debt/GDP) =1 – (fiscal multiplier)(Debt-1/GDP-1) /(1+g)2

where the fiscal multiplier is the first derivative of g with respect to deficit. This shows, as mentioned in the text, that the sign of the change in the debt/GDP ratio depends on the on the initial debt/GDP ratio and the size of the fiscal multiplier.

To make this easier on the eyes, we can use the approximation that 1/(1+g)2 is 1 so the formula becomes3:

(5) Change in (Debt/GDP) = 1 – (fiscal multiplier)(Debt-1/GDP-1)

It follows that a lower deficit will not improve the debt ratio if:

1 < (fiscal multiplier)(Debt-1/GDP-1)

This condition would be satisfied at typical European (or US) debt ratios if the multiplier exceeds unity. For example, it would be satisfied for a country with a starting debt ratio greater than 1 (Italy today has 120%) and assuming that the fiscal multiplier is also at least equal to one.

What would be a typical value for the multiplier in reality? It turns out that it is difficult to even determine a range given that there is little agreement in the literature on the magnitude of even the short-run multipliers. More ‘Keynesian’ models tend to have larger multipliers, often higher than one. More forward looking models tend to have lower multipliers because in more forward looking models agents tend to lower expenditure already today in anticipation of the higher taxes they will have to pay in future.

One additional problem neglected here is that the debt/ratio is obtained by dividing the nominal debt by nominal GDP whereas most macroeconomic models are constructed in real variables. However, given the low (and persistently) low level of inflation at present in the Eurozone this should not affect the results if all the variables are interpreted as deviations from a baseline. However, the short-run multiplier should be larger if one looks at the impact of a cut in expenditure on nominal GDP (as opposed to real GDP).

Longer run

To analyse the longer run one has to go beyond the current period. One could consider the current period as the short run and the next period the long run. The long-run debt would thus be given by the sum of the debt at the end of the current period and next period’s deficit.

Dividing through by next period’s GDP and forming debt/GDP ratios by dividing and multiplying by contemporaneous GDP, we see that the future debt ratio depends on future deficits and growth rates.

Analysis can be conducted using two simple cases.

- A temporary cut: the current deficit is cut, but the future deficit return to baseline and GDP along with it.

This implies that a temporary cut in the deficit must improve the long-run debt-to-GDP ratio – whatever the deterioration the debt ratio that might have materialised in the short run. Indeed, if the baseline deficit is zero, the improvement in the long-run debt/GDP ratio is approximately the size of the initial austerity. After all, the GDP is assumed to return to its normal path in the long run, but less debt has been added in the meantime (this simplification approximates 1+g as 1 as before). The (short-run) multiplier does not matter for the long run.

- A permanent cut in deficit. In this case one could discuss whether GDP returns to baseline or not.

In most macro models this would be the case, but it is useful to consider the rather extreme case where a permanent reduction in the deficit leads to a permanent drop in activity. In this case:

With the deficit ratio constant this implies:

This shows that the condition for fiscal adjustment to be self-defeating is now less likely to be satisfied since the product of the multiplier and the starting debt/GDP ratio must now exceed two.

__________

1 See for instance the report by the US Center of Budget and Policy Priorities on the expansionary policy of 2001-2007. Krugman (2011) provides an example of ‘Self defeating austerity’, but this example is based on the assumption that a loss of demand has external effects (loss of human capital of the unemployed).

2 For example, if GDP=100 and debt=120, then the 120/100 debt/GDP ratio rises to 121.8 if GDP falls to 98.5.

3 For example, if annual growth is 1%, 1+g=1.01, so 1/(1+g)2 is 0.98.

![]()

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply