We enter yet another interesting week in Europe with the same discussions on how high interest rates will be in Italy or Spain, rumors on a possible IMF program for Italy (doubtful) and pressures on the ECB to do more. So far ECB officials argue that “bailing out” Euro governments will violate their legal framework and it is a bad idea. Without going again into the arguments of whether the ECB can and should buy Euro government debt, here is a quick comparison between the US Fed and the ECB in terms of holdings of government debt.

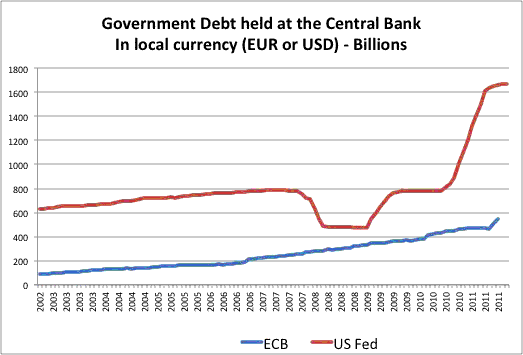

The chart below measures the holding of US government debt at the US Fed and Euro government debt at the ECB. They are measured in billions of local currency (USD for the US, EUR for the ECB).

If you look carefully at the last months you see a small increase in the ECB holdings that reflect their recent attempts to bring some stability to financial markets and keep bond yields under control. But how does it compare to the US Fed actions over the last two years?

Let’s first compare the end point. Today the US Fed holds about 1.7 trillion of US government debt. This represents about 11% of the 15 trillion of outstanding US government debt. For the ECB, the holdings of government debt are about 550 billion (EUR), which is less than 7% of the total outstanding debt of Euro governments (around 8.3 Trillion).

If we look at the evolution over the last years we can see that from mid-2009 the US Fed has doubled the holdings of government debt. If we use 2008 as the starting point then we are looking at an increase of more than 300%. The decrease in holdings of government debt in the years 2008-09 corresponds to the period when the Fed was exchanging treasury bills against other assets such as MBS.

The ECB has also been increasing its holdings of government debt. From 2008 to today it has increased its holdings by about 66%. But this increase is not that different from the previous trend and there seems to be very little change during the crisis except in the last months.

The actions of the Federal Reserve are part of its monetary policy strategy and not an attempt to provide a hidden bailout to the US government (not everyone agrees on this but let’s leave that discussion for the future). The comparison between the two central banks and the fact that the ECB is so reluctant to consider a similar action in the current environment where financial and macroeconomic stability are at risk makes the ECB decision even more difficult to understand.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply