In our post, The Biggest Bubble in History, we tried to convey that a monetization of Europe’s sovereign debt is not equivalent to the quantitative easing that has taken place in the U.S. , Japan, and the U.K. We had a lot of pushback on the piece so we’ll try and be more clear and concise.

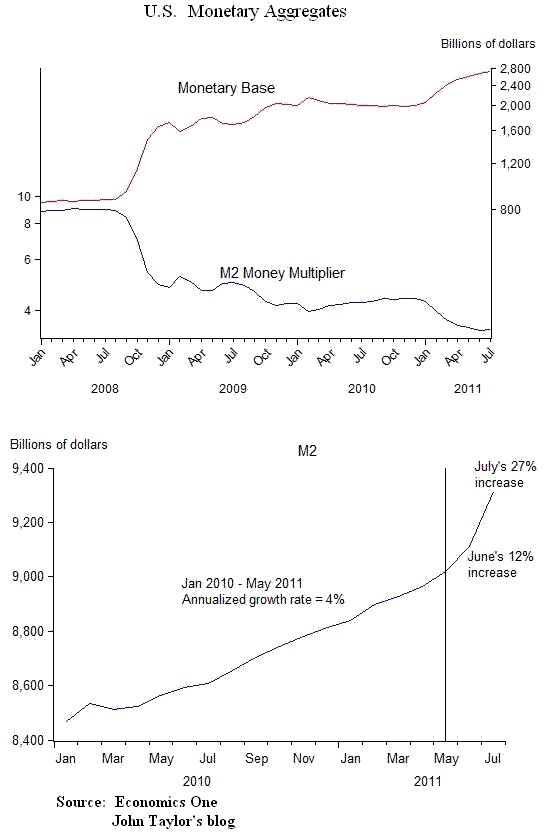

Quantitative easing in the U.S., U.K., and Japan is an attempt by the monetary authorities to offset the massive headwinds of the credit contraction caused by the collapse of the U.S. shadow banking system and the tightening of bank lending. Though the Fed has tripled the monetary base and has stepped in to become the de facto shadow banking system, the monetary aggregates have not experienced similar growth.

The recent market volatility has created demand for U.S. bank deposits as a safe haven and the traditional monetary aggregates, such as M2, are now beginning to show robust growth. It’s unlikely, however, that the uptick of the aggregates is the result of credit expansion.

The expansion of the Fed’s balance sheet through the purchase of treasury and mortgage securities has been largely financed by an increase in the banking system’s excess reserves.

This is totally different than if, say, the Fed had to step into the Treasury market because investors had lost confidence in the federal government’s ability or willingness to pay its debt obligations. First, the mechanics of such a Fed intervention would be unclear. Second, and more relevant for Europe, is what would happen to the demand for the dollars if the Fed was seen as printing money to pay off bad debt the Treasury couldn’t roll over?

If the ECB were to begin monetizing “bad” sovereign debt, we suspect that money demand in Germany and the stronger core countries could shift dramatically as the perception of the Euro as a hard currency would be begin to fade. Unlike many analysts who have no skin in the game, the German people understand the difference between the Federal Reserve’s quantitative easing and the money printing of, say, the Banco Central de la Republica of Argentina in the 1980’s. Such a loss of confidence in the ECB could cause the Euro collapse and set off a major currency crisis.

This is not to say the ECB doesn’t have room to engage in quantitative easing alá the Fed. As banks shrink their balance sheets, Europe will experience an acute credit crunch and monetary contraction. This could create “room” for the ECB to expand the monetary base a bit faster.

But let’s keep clear the difference between debt monetization and the quantitative easing that is taking place in the U.S., U.K., and Japan. The major stakeholders in the Euro currency certainly will.

This could be one factor in yesterday’ failed bond auction in Germany. As pressure increases on the ECB to monetize the rollover of debt maturities, we expect money demand to shift downward and capital flight out of Europe to accelerate. Stay tuned.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply