Paul Krugman talks about the causes of the current sovereign default crisis in terms of what economists call “the original sin”. The concept was developed to describe situations in which a country borrows in someone else’s currency. When faced with a crisis, large devaluations of their exchange rates make the value of debt increase, which leads to default and possibly a deeper crisis. Krugman argues that a similar logic applies to Euro countries today: Italy has borrowed in a currency (Euro) that they do not control and this is a problem. If Italy had borrowed in their own currency they will always be a way out of a high debt situation: printing more Italian Liras.

Let me take a step back before I comment on how the “original sin” applies to Europe. What is a government default? Government debt is a result of spending decisions that have not been financed with tax revenues. If government debt is to be paid back it simply means that some future tax payers will pay for the spending done in previous years. If debt is not paid back and government defaults, it is simply a shift in the burden of paying for the debt from current and future tax payers to someone else (bond holders). In that sense, default of a government has nothing to do with default of a company where we tend to think about a failure of a business model. It is simply about finding someone else to pay for our spending, not tax payers.

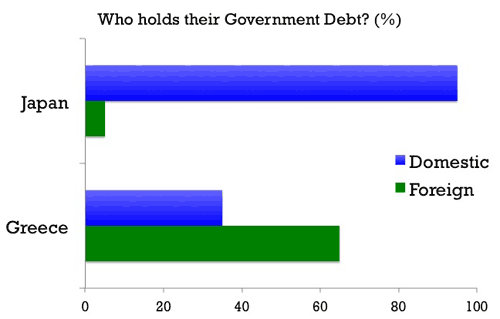

But who else will pay for it? In a closed economy (no international trade or capital flows, think about the world), it is not obvious to find “others” who will pay for our spending. You can shift the burden from tax payers to bond holders but in a closed economy both are citizens of your country, in some cases they are the same individuals. No economy is closed but some do not look far from this example. Below is a chart comparing Greece and Japan in terms of who holds their government debt (domestic versus foreign investors).

In the case of Japan, most of the Japanese government debt is held by Japanese citizens. If the government of Japan defaults it is equivalent to sending a tax bill to only bond holders. But they are Japanese tax payers so there is very little difference between default and taxes, there is no choice! I am, of course, simplifying what is a more complex situation: not every tax payer in Japan has an amount of government bonds which is proportional to their income and Japan is an open economy but to a large extent we are talking about a redistribution decision. The comparison to Greece is a good way to understand that the trade offs and consequences of a decision to default are not the same for Greece. Greece can potentially pass the burden to others (foreigners) who are currently holding its debt.

Back to the “original sin” discussion. When a government borrows in its own currency, there is a third alternative to taxes and default: printing money. Conceptually, it not different from the other two: you need to grab someone else’s resources. Printing money leads to seignorage via inflation and this is an alternative source of income that can be seen as a tax on those whose assets are denominated in nominal terms. Some of these individuals are also tax payers, some are the ones who are currently holding your bonds, so you might be passing the bill to the same people but in different proportions (as in the Japanese example).

At the end of the day, default, taxes or seignorage are three ways to pay for the spending governments have already done. They are not that different conceptually. In a closed system there is no way to avoid grabbing resources from your own citizens – in some sense deciding between the three choices is simply a redistribution decision. In an open economy you might be able to grab resources from other countries by defaulting on debt held by foreigners. Although conceptually similar, each of the three methods differ in terms of the political consequences or even feasibility. Passing the bill to foreigners will tend to be easier from a political point of view although it will have more damaging effects in terms of credibility. In some countries raising taxes is more feasible than creating inflation. In other cases it will be the other way around. From an economic point of view it might be that the same individuals end up paying the bill but sending them a bill in a different format or color just happens to be easier.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply