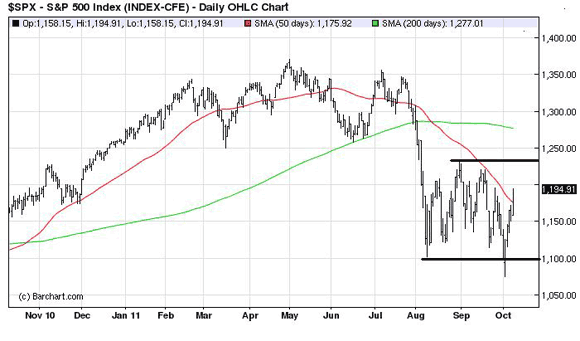

We asked last week if the S&P500 (our proxy for risk markets) was capable of clearing the “red zone”, the zone of resistance between 1175-1195, which included the 50-day moving average. The market’s answer? Like a hot knife through butter!

Interestingly, the S&P500 closed at its high of the day at? 1194.91! Not a sold out crowd yesterday as the volume was super light. Nevertheless, impressive. The bears need to take a goal line stance right here and push back the momentum or the next stop is S&P500 1230, the top of the recent trading range which began with the August collapse.

We have posted several pieces on the three macro bears that have been weighing on equities: 1) Europe’s sovereign debt and banking crisis; 2) The slowing of the U.S. economy and employment problem; and 3) China hard landing concerns. We’re not sure — and have our doubts — all three bears have gone into hibernation for the winter, but they do appear to be, at least, napping.

Yesterday’s intervention to support the banking system by the Chinese government was a big, yet under appreciated, catalyst for the rally, in our opinion. The FT writes,

Central Huijin, the domestic arm of China’s sovereign wealth fund, will purchase shares in Agricultural Bank of China, Bank of China, China Construction Bank and Industrial and Commercial Bank of China, the official Xinhua news agency announced on Monday. Xinhua added that the purchases by Huijin – its first such public intervention since a similar decision at the onset of the financial crisis three years ago – would “support the healthy operations and development of key state-owned financial institutions and stabilise the share prices of state-owned commercial banks”.

The announcement came too late for the Chinese stock market, which had closed at a 30-month low, but had an immediate effect on late trading in Hong Kong. ICBC’s Hong Kong-listed shares, which had been down 3 per cent, rallied to close up 1 per cent.

The U.S. economic data looks to be improving and Europe has a plan to have a plan to recapitalize the banks and fire break the contagion of a Greek default.

We’re always flying blind with China due the country’s lack of transparency, but the equity markets have been hammered over there and should rebound on the intervention news providing more confidence for the global markets. The announcement of intervention came after the market closed but Asian ETFs were up big in New York trading.

The U.S. data, including Friday’s employment number, are not great, but beating to the upside. The key now is for earnings to confirm the U.S. economy is not sliding into recession. Company outlooks are more important in this season than almost any we can recall.

We’re most worried about Europe. There is more time for the markets to continue to hope as the E.U. summit meeting has been postponed to October 23rd to give policymakers more time to hammer out the details. They really need to get this right.

A big commitment by a national government to backstop its banking system could have adverse consequences for the sovereign’s credit rating, which negates the positive contribution of the recapitalization. This destablizing feedback took down Ireland and the worries seem to be the biggest point of disagreement between Merkel and Sarkozy.

The markets aren’t focused on these concerns and want to believe the three bears are hibernating for winter. They want to rebound from the August collapse like a beach ball held underwater. And that they are. Stay tuned.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply