The Federal Reserve announced on Wednesday ([1], [2]) that it will sell some of its shorter-term assets in order to buy more longer-term assets. Here I assess some of the possible consequences of this move.

The maneuver is being referred to by some as “operation twist”, an expression that was originally used to describe a plan implemented by the Kennedy administration and the Federal Reserve in 1961, and given its moniker after a dance popular at the time. The idea then was that the Treasury would replace some of its longer-term debt with shorter-term obligations, and the Federal Reserve would simultaneously sell some of its shorter-term securities and buy longer-term Treasuries. Some of the early research (e.g., Modigliani and Sutch, 1966) concluded that the original Operation Twist was not terribly successful. However, Federal Reserve Bank of San Francisco economist Eric Swanson has a new paper recently presented at the Brookings Institution that makes a convincing case that Operation Twist did succeed in its goal of modestly lowering long-term interest rates.

The Fed announced on Wednesday that it is going to try something similar, intending over the course of the next 9 months to sell about $400B worth of its Treasuries that have maturity between 3 months and 3 years in order to buy securities with maturities of 6 years or longer. According to the latest H41 statement, the Fed currently only has $129B in Treasuries between 3 months and 1 year, meaning that much of what they plan to sell has to be in the 1-3 year range. The details of the plan released by the Federal Reserve Bank of New York indicate that about 2/3 of the securities purchased will be in the 6 year to 10 year range, and most of the rest will be over 20 years.

The idea behind this plan is that, in the current setting, dumping an increased supply of shorter-term Treasuries on the market should have little or no effect on the short-term interest rate. But by buying more of the existing supply of longer-term Treasuries, the intention is to nudge the price of those securities a little higher, or in other words, try to move the long-term interest rate a little lower. The hope is by lowering interest rates, there would be slightly more opportunity for households and firms to borrow or refinance and perhaps increase spending a bit. The new measure thus represents something the Fed could try, over and above what it already did in QE2, that might further stimulate the economy without expanding the overall size of its balance sheet any bigger than it already is.

In a research paper that I wrote with Cynthia Wu, which will soon be published in the Journal of Money, Credit, and Banking, we came up with a framework for evaluating the effects that policies like this might have. Our estimates are based on how changes in the relative supplies of publicly-held Treasury debt of different maturities correlated historically with changes in the basic factors determining interest rates on different securities, which factors we summarized by the level, slope, and curvature of the term structure of interest rates. We also built a simple model of how latent level, slope, and curvature factors have been influencing the evolution of interest rates in an environment like the current one in which the overnight interest rate is stuck near zero.

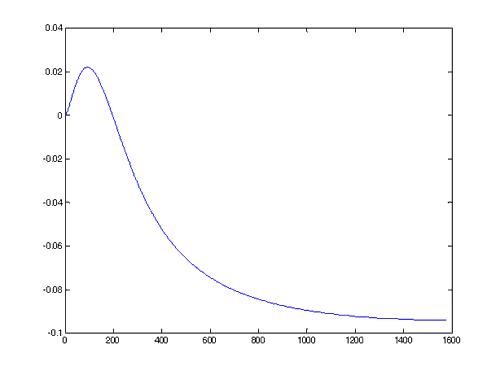

We decided to redo some of our earlier analysis in order to evaluate the potential effects of a policy like that just announced by the Fed. We conducted the following counterfactual experiment. Suppose that at some historical date t, the Federal Reserve were to have sold off its entire holdings of securities between 3 months and 3 years duration, and used the proceeds to buy an equiproportional amount of all outstanding Treasury securities between 6 years and 30 years duration. For example, if implemented in December 2006, this would have been an operation involving about $343 billion in securities. We calculated what this would have done to the level, slope and curvature factors, and what that would mean for interest rates of different maturities in the present setting where the overnight rate is stuck near zero. The result is plotted in the graph below. The horizontal axis reports the maturity of a given security (measured in weeks), and the vertical axis reports how the yield on that security (measured in annual percentage points) might change in response to operation twist.

Horizontal axis: maturity of security (in weeks). Vertical axis: predicted change in yield on that security (in annual percentage points) as a result of “operation twist”. Calculated using same methodology as dashed line in Figure 11 in Hamilton and Wu (2010). The figure plots 5200bn*’φΔ3 for Δ3 = (0.014313,0.012336,-0.0047943)’ corresponding to the average impact on q of the Fed historically selling all its 3m-3y and buying 6y and up.

We don’t claim to have very precise estimates for the outcome of this new counterfactual experiment– the values in the figure above are not statistically distinguishable from zero, according to our analysis. Nevertheless, they represent the best estimates I can give for the effects of operation twist. Our estimates suggests that a policy such as the newly announced operation twist might increase 1-3 year yields by 2 basis points and lower the yield on the longest term securities by a little less than 10 basis points.

In addition to the statistical accuracy, there’s another big caveat for these estimates, which is that we are analyzing the effects of Fed policy alone, assuming that there are no changes over the next 9 months coming from the Treasury. However, this assumption proved definitely not to be the case with QE2. There, while the Fed was trying to buy more long-term securities, the Treasury was preferentially issuing new long-term securities at an even faster rate, with the net result that the Treasury basically undid any stimulative effects of QE2. Thus, in contrast to the original Kennedy Operation Twist, in which the Treasury and Fed were working together, it’s quite possible that in the current environment, they will continue to be pulling the economy in opposite directions. So I expect the effects of the Fed’s latest measure could turn out to be significantly less than 10 basis points.

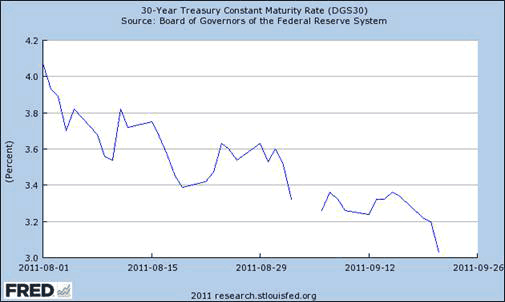

How then do I explain the fact that the 30-year Treasury yield fell 17 basis points on Wednesday? My answer is, this wasn’t just the Fed. News of a weakening European economy may have been more important. There also may have been some signaling effect with investors concluding, “Gee, if the Fed thinks they have to do this, the economy must be in even worse shape than I thought!” As evidence in support of such an interpretation, commodities and equities also fell significantly, moving in the opposite direction from what you would have expected if you believed new stimulus from the Fed was the key development driving markets.

Source: FRED

The modest effects that one could reasonably anticipate for a measure like operation twist are easily swamped by other developments, and even a sizable effect on 30-year Treasury yields would not in my mind provide a major stimulus. I think the correct interpretation is that the Fed would like to bring some more stimulus, this was something they could do in that direction, so they did it.

But if you were about to drown, I wouldn’t want to count on operation twist as your lifeline to safety.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

We have an economy larger than the Eurozone & are deliberately heading full throttle to oblivion as a former superpower. Our drivers of wealth; agriculture, natural resource development & manufacturing are abandoned while this consumer spending/service based economy moves money from one sector to the other putting nothing into the economy needed for true wealth/prosperity creation. This monetizing of treasury debt doesn’t add to the Fed’s balance sheet, it sets the stage for a treasury sale of long term bonds at lower rates. Meanwhile all the financial morons explain why the stock market plunges & rebounds, but the reality is total uncertainty, except heading as fast as possible to a world economy of debt that is collapsing social democracy. We have one more chance in 2012, Europe doesn’t. China now resembles the foundation of America’s economy more than America! The only question left to ask is will we be able to clean DC enough in 2012 to fix govt to stop the drift toward totalitarian socialism? Here are my thoughts on where we stand:

https://www.facebook.com/note.php?note_id=231962353516849