Who would have thought that the ballooning of fear would be deflated by the sedentary Swiss. But that is certainly what appears to have happened with the hysteria levels much lower as our IB chatometers have returned from doom+ levels to a more balanced outlook with stories of hope tentatively being offered. So for now the equation is:

Global Terror + SNB + Hope(G7+HIA+ECB+UKQE) = Relief

Which suits TMM just fine.

TMM have, as you may have detected, been erring between tentative equity buyers in the style of “on the one hand” hedge me calls analysts, to outright “so excited we cant pee straight” buyers. Of course, the SEWCPS signal is usually a sure indicator of unreasoned stupidity, so we thought we d better have a closer look and see if it is justified.

And that brings TMM onto the DAX, which has taken a very large pummeling in recent weeks. Obviously, the imposition of short-sell bans in Europe, preventing the EuroStoxx future from being used as a hedging mechanism has played a large part in its under-performance as “hedgers” moved to short the DAX instead. TMM use the term “hedgers” loosely, as it seems to them that given the wild cheering on their IBs and email messages the past couple of weeks to the move lower in the DAX, that there are a great deal more players short the index than merely hedgers alone. Indeed, TMM’s sales coverage has highlighted a lot of interest from macro hedge funds in being short, meaning that there are a significant number of “Tourist Traders” in that market. The trouble with this is that the DAX is a lot less liquid than the EuroStoxx. Now, TMM have learned very painfully in the past that when trying to get out of positions that are illiquid when everyone else is positioned the same way that the door isn’t big enough and you get Pink Flamingo-ed.

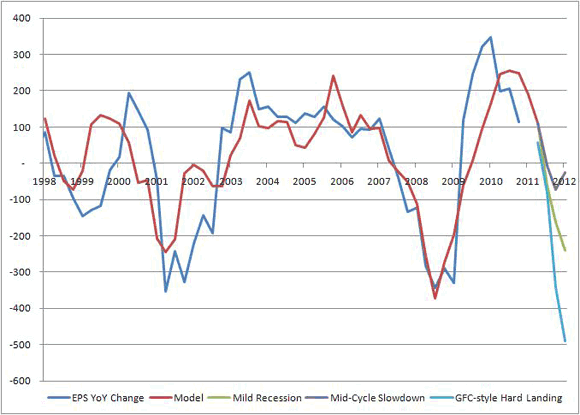

Now, TMM admit, positioning is not a sufficient trigger for reversals, and neither are valuation-based arguments – which as many point out – are vulnerable to becoming value traps. But for completeness, TMM reckon it is worth considering what the downside in DAX could be. As with all models, the below (very) naive model for the YoY change in EPS for the DAX (based upon lagged ISM, IFO, CPI, PPI and Wage growth) is meant only to be illustrative from the macro level, rather than fully explain earnings growth or margins or any particular specifics. [Stats Geeks: the large tech-related write-downs in 2001-3 make it not particularly meaningful to look at YoY % EPS growth when modelling, but looking at the straight change in EPS growth should eliminate the root unit problem in the regression.]

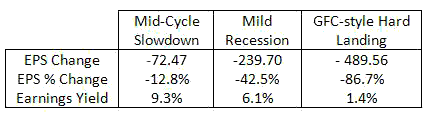

The last model print in the chart assumes that IFO falls 4pts this month to 102 (which seems reasonable given the falls in the PMI etc), and the final three lines are rough forecasts of the underlying variables for a Mild Recession (e.g. 2001-3), a Mid-Cycle Slowdown (e.g. 2005) and a Global Financial Crisis-style Hard Landing (e.g. 2008/9).

Translating these into more meaningful %age changes and the implied Earnings yields under those scenarios, and making the exceptionally conservative assumption that the current DAX price discount ZERO fall in earnings (while it clearly does)then in a GFC-style crisis, this would imply earnings falling nearly 87%, leaving an earnings yield of around 1.4% (vs. Bund Yields at 1.89%). Now, TMM tend to think this model is perhaps too pessimistic, given that in 2008/9, earnings actually only actually fell about 60%, and that would leave the earnings yield sitting around 5.8%.

Either way, the point of this exercise is to demonstrate that the DAX already pricing in a pretty dire macroeconomic outcome. In fact, TMM reckon that it is hard to argue that the DAX does not already price in EPS falls of some degree, and thus the above numbers understate the actual Earnings Yields in such scenarios. And thus, it is pretty hard to argue that the DAX is anything but exceptionally cheap in this framework, with a forward P/E of just 7.3x.

Now lets look at the background. Interestingly news-flow has begun to improve, with the German Constitutional Court ruling and Italian fiscal packages voted through, the US economic data stabilizing, a US Jobs Plan in the offing and the potential for a G7 policy response that is likely to target the recapitalisation of Europe’s banking system (judging by recent leaks), all falling onto a market that has been up until recently been wrist slittingly suicidal. The technical picture is also supportive of a run higher with dojis/island reversals in various equity markets and even a soothsayer signal in the DAx itself, we reckon that the conditions are in place for a more dramatic rally.

SO, are we still at SEWCPS levels? Yeah… why not…? Where’s the fun in life if you can’t jump around like a 9 year old at the sound of the ice cream van coming down the road*?

—————

* TMM have a friend whose dad told them at a very early age about the tune the ice cream van plays: “Well they play it when they have run out of ice cream and have to go back to the yard”. Masterful parenting.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply