Yesterday the CBO released new figures describing both its projections for the US federal budget deficit, and its estimate of the impact on the economy of the 2009 stimulus package (the ARRA). The budget forecast is grim, of course, and the CBO attributes much of the bad budget outlook to the bad economy.

But while there’s a lot of good stuff in both documents, I was particularly intrigued by a rather remarkable sidenote included in the budget forecast document. The CBO explained that they believe that the Great Recession will have very persistent effects on long-run economic growth in the US. From yesterday’s CBO budget update, p. 54 (pdf):

The financial crisis that began in 2007 had a sharp impact on the U.S. economy, nearly freezing credit markets and pushing the economy into the most severe recession since World War II. International experience shows that downturns following financial crises tend to be more prolonged than other downturns, and the return to high employment tends to be slower. In addition, because such recessions—more so than typical recessions—raise the level and duration of unemployment, reduce the number of hours that employees work, and dampen investment, they are more likely to reduce potential output for some time.

…Combining estimates of the effects on capital accumulation, potential hours worked, and potential total factor productivity, CBO projects that potential output will be about 2 percent lower, on average, between 2017 and 2021 than it would have been without the financial crisis and the recession.

This is a point that Brad DeLong has particularly emphasized (see for example here and here); it’s good to see the CBO incorporating the recession’s “shadow”, as Brad calls it, into their forecasts.

But this has important implications for projections regarding the costs and effects of stimulus spending right now. If a new stimulus plan had been implemented at the start of 2011, for example, the economy would be significantly stronger this year and the long-run effects mentioned by the CBO would be smaller going forward. And this in turn means that stimulus spending right now would, according to the CBO, significantly improve long-run growth prospects, and hence the budget outlook for the federal government.

In the other document put out by CBO yesterday there are estimates of the economic impact of the ARRA (pdf). And in the CBO’s January 2011 budget outlook (pdf) the CBO provides, in table B-1, some “rules of thumb” to translate changes in forecast economic growth into changes in the forecast budget deficit.

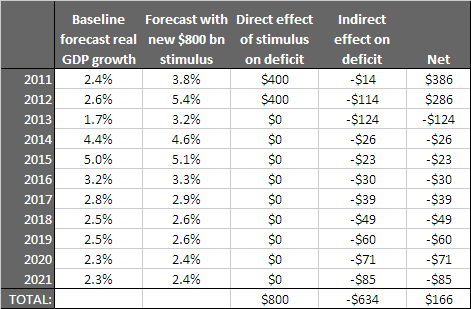

This gives us all the ingredients we need to create a back-of-the-envelope estimate of the long-run budgetary impact of new stimulus spending. Suppose that a new stimulus package of $800 billion (about the size of the ARRA) had been enacted early in 2011. Suppose that its impact on economic growth was half way between the CBO’s high and low estimates of the impact of the ARRA. And suppose, finally, that the resulting return to strong economic growth in 2011 and 2012 allowed the US economy to reduce by half the long-run, persistent impacts of the Great Recession highlighted by the CBO above (i.e. the recession’s “shadow”). Using the CBO’s rules of thumb for how this would impact the budget deficit, we get the following:

Using the CBO’s estimates, the additional economic growth that such a stimulus package would cause — particularly over the second half of the decade — would mean that the $800 billion stimulus would indirectly reduce the budget deficit by $634 over ten years. So the net deficit impact of such stimulus spending would only be $166 billion, or about 20% of the initial outlay. And of course, if we extended the time horizon beyond just the next ten years, the payback would be even greater.

Note that this is not a normal result for additional government spending. The beneficial effects on the budget deficit over the long run would disappear if the US weren’t trapped in this ongoing debilitating recession. But given our current situation, the US can actually get a remarkably good deal on new stimulus spending: for every dollar the US government spends to stimulate the economy and create jobs, the economy will pay back 80 cents as a way of saying thanks…

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply