Economic conditions are deteriorating. Here’s how and when the Fed might intervene.

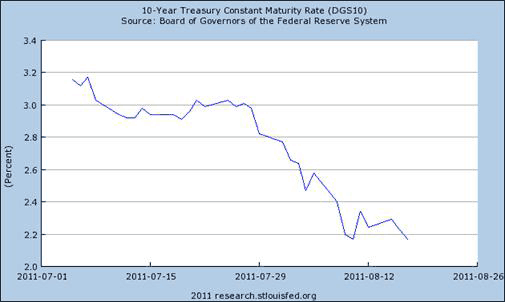

Bond yields on perceived safe assets have plunged as pessimism over global economic conditions takes hold. The 10-year U.S. Treasury rate has fallen 100 basis points since the start of July, signaling expectations of a profoundly weak economy and a very low inflation rate over the next decade.

Source: FRED

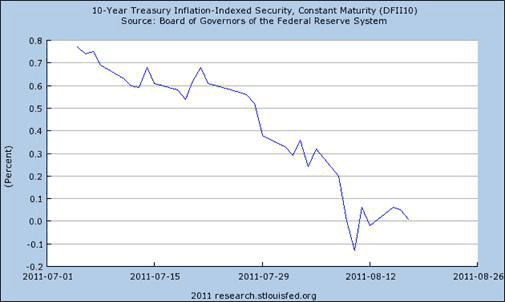

The yield on Treasury Inflation Protected Securities, whose coupon and par value are guaranteed to go up with any increases in the headline consumer price index, fell by almost 80 basis points over the same period. That suggests to me that lower inflationary expectations have made only a minor contribution to falling nominal yields, with perceptions of a weaker economy the dominant factor.

Source: FRED

And in response, the Fed should do what, exactly? A new phase of large-scale asset purchases (which doubtless would be referred to in the press as QE3) could sop up a few more percent of publicly-held Treasury debt. Conceivably that could put pressure on the nominal or TIPS yields to decline even further, and I suppose that one might hope that a 10-year real Treasury yield of -0.2% would be slightly more stimulative than the current real yield around zero.

I would suggest that the more important and achievable goal for the Fed should be to keep the long-run inflation rate from falling below 2%. The reason I say this is an important goal is that I believe the lesson from the U.S. in the 1930s and Japan in the 1990s is that exceptionally low or negative inflation rates can make economic problems like the ones we’re currently experiencing significantly worse. By announcing QE3, the Fed would be sending a clear signal that it’s not going to tolerate deflation, and I expect that would be the primary mechanism by which it could have an effect. Perhaps we’d see the effort framed as part of a broader strategy of price level targeting.

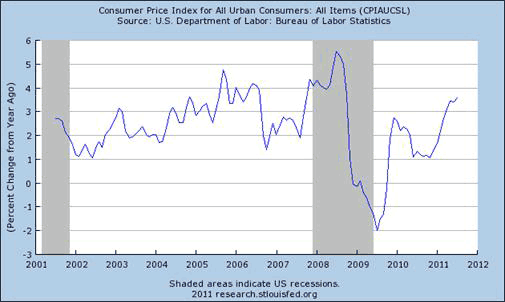

The graph below plots the annual percentage change of the headline CPI over the last decade. Defenders of the Fed could argue that QE1 helped kick the economy out of a dangerous deflation scare in 2008-2009 and that QE2 helped bump us out of the disinflationary environment in the fall of 2010.

Source: FRED

The Fed’s critics, however, see something more insidious. Governor Rick Perry (R-TX) got a lot of attention last week with a criticism of the Federal Reserve that makes Rep. Ron Paul (R-TX) look like a moderate:

..If this guy [Fed Chairman Bernanke] prints more money between now and the election, I don’t know what y’all would do to him in Iowa, but we would treat him pretty ugly down in Texas. Printing more money to play politics at this particular time in American history is almost treacherous, or treasonous, in my opinion.

David Glasner (hat tip: Economist’s View) responds:

Well, let’s take a look at Mr. Bernanke’s record of currency debasement. The Bureau of Labor Statistics announced the latest reading (for July 2011) of the consumer price index (CPI); it stood at 225.922. Thirty-six months ago, in July 2008, the index stood at 219.133. So over that entire three-year period, the CPI rose by a whopping 3.1%. That is not an annual rate, that it the total increase over three years, so the average annual inflation rate over the whole period was less than 1%. The last time that the CPI rose by as little as 3% over any 36-month period was 1958-61.

Some may read the 12-month (as opposed to 36-month) rates in the graph above as suggesting we’ve left that episode behind and inflation is now headed higher. I believe it’s more likely instead that we’ll soon see the series moving back down with inflation rates well below 2%, and that in retrospect more observers will be inclined to view this episode from Glasner’s perspective of a prolonged, ongoing disinflation. I’d also guess that once the evidence of renewed deflationary forces becomes clearer, then the Fed would once again signal with some version of QE3 that it doesn’t intend to let such a situation continue.

Another related possibility is that the European sovereign debt concerns morph into a freezing of international credit markets, leading to some repeat of the ugly events of the fall of 2008. Here again there is little doubt that the Fed would need to intervene preemptively not with large-scale asset purchases but instead with the kind of emergency credit facilities that we saw 3 years ago.

And while I’m offering predictions, I might as well make it a triple. If events do take this turn and Bernanke does act again, he’ll be the subject of personal political attacks even more vicious than we’ve seen so far. But I expect the Fed chair to go ahead with the policy in those circumstances anyway, because he knows it’s the right thing to do. I could even imagine the Texas Governor delivering a rousing speech, praising in his appealing drawl those who have the courage to make a personal sacrifice for the larger good.

But I don’t expect the Governor to include in such a speech recognition of one person who deserves such praise.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply