Well, the choppiness across markets continues, with Asia selling off on the back of potential US bank lawsuits and rumours of a Spanish and/or Greek snap election, only for Europe to reverse most of the overnight move. Or then again, like yesterday it could just be a case of “fill the gap” and then roll-over again. TMM still sense that punters are trying to hold onto long risky asset positions, or at least still attempting to follow the JBTFD strategy and it doesn’t seem to us that there has yet been a capitulatory “baby with the bathwater” moment as of yet.

It is particularly striking that the PhD community has only just begun to downgrade their 2Q11 GDP forecasts, with JPM overnight lowering theirs from 3% to 2.5%. While TMM’s survey-based GDP proxy underperformed the official GDP figures in early-2010 (largely, we believe, due to the impact of the fiscal stimulus), since then it has re-converged, and after implying a brief growth spurt in Q1, it has come off sharply, and is now consistent with 1.5% annualized rates of growth. Now TMM completely accept the idea that this is downwardly biased by seasonal issues related to the timing of Easter, but even if we generously add 0.7% to that figure, we still sit at 2.2% while consensus are at 3.3%. TMM reckon the PhD community have some capitulation to do, and with them, erstwhile risky asset longs.

The other argument TMM have heard is that “it’s all just the Japanese supply chain effect”. Sure, some of it is – the obvious stuff like Toyota etc – but if this were really the driver of the slowdown, then it would show up in inventory/sales ratios… and the below chart of ISM Orders/Inventories shows a clear downtrend.

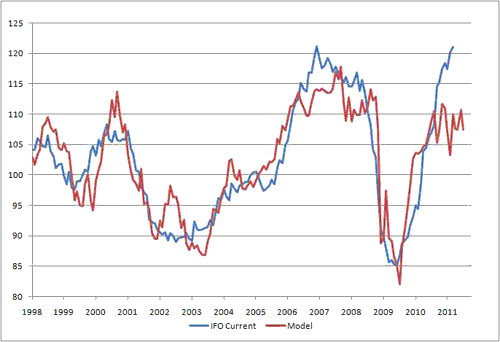

Continuing along the lines of TMM’s belief that global growth has rolled over and is moving into a soft patch and, ultimately, growth scare, we decided to take a closer look at the post-crisis powerhouse that is Germany. Yesterday’s IFO survey seemed to point to continued vigorous growth, but TMM are sceptical given that Germany is leveraged to China and the rest of Europe, and still has shown itself unable to sufficiently produce its own domestic demand. So, along these lines of thinking, TMM decided to construct a set of FCI-like models for IFO, the Manufacturing PMI and, most importantly, GDP. The logic behind using the components of an FCI is that it can provide a basis for the conditions of domestically-generated growth.

So, first off, the IFO (see chart below: IFO – blue line, model – red line). The model fit here has been OK, but not brilliant, and despite financial conditions having flattened out over the past year, the IFO has gone on to hit highs not seen since 2006. TMM are aware that the construction of the IFO survey has changed recently, so that may be behind some of the divergence, and possibly, the strong cash position of small-medium German corporates (who make up the bulk of the survey responses) may well be reason here, with less need for financing.

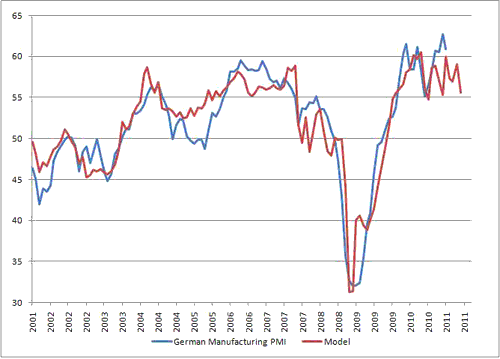

Next up, the Manufacturing PMI (see chart below – blue line, red line – model). As this is primarily made up of larger companies, it is more reflective of global demand growth and, given their funding nature, more sensitive to financial conditions. The fit is much better here, and shows the PMI falling to around 55, so still decent growth but not at the exceptionally strong rates seen over the past year or so. Given the tightening path the ECB is on, it is likely that this will continue to drift lower.

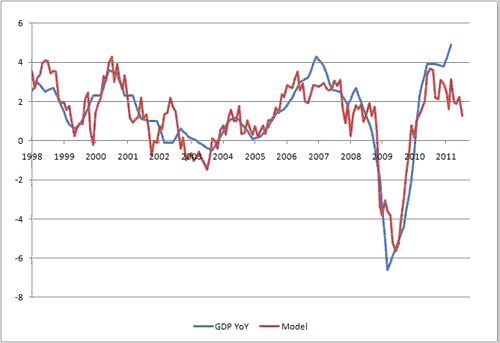

Finally, GDP (see chart below – blue line, model – red line). Q1 2011 saw a very strong print from Germany, that is flattered by a high rate of Government Spending (+1.3% vs. expectations of just 0.2%), something that TMM reckon will revert in the next print. Indeed, apart from that, the model does a pretty good job of predicting German GDP, and the direction is clear: sub-trend growth.

To summarize, it seems that while German SMEs aren’t doing too shabbily, outperforming what one might expect given financial conditions, that is yet to show up as significant domestic demand (Q1’s was just 1.1%, following on from -0.2% the previous quarter). The more important large corporates look set to experience the squeeze in financial conditions as the ECB moves to hike rates and worries regarding collateral damage from the PIGS widen credit spreads. It seems clear to TMM that German growth is also moving into a mid-cycle slowdown along with the rest of the world and that is the last thing Europe needs.

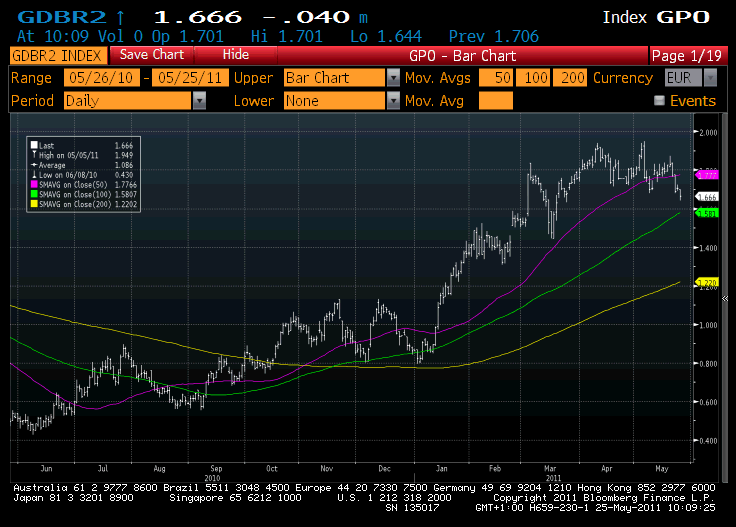

However, with Schatz yields 20bps lower (see chart below) in just a week (see chart below) it’s hard to get too long of the front end here. TMM are still holding their September 107.40 calls, though, which given the slow motion train crash occurring in Greece (which could be particularly disastrous should the proposed austerity referendum fail), look like a good bottom drawer trade for what they expect to be a choppy month of trading as markets try and make sense of where we are in the global cycle.

(click to enlarge)

And TMM didn’t even mention Marmite.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply