I just finished watching Ben Bernanke’s press conference. I don’t think there was a lot of news in it. However, some impressions I had before were confirmed.

First and foremost, the bar to starting another round of quantitative easing is quite high, and thus it is unlikely to happen. Second, Bernanke views the unemployment problem as more serious than the inflation problem. That, however, is a bit of a contradiction to the first part. Seems sort of like a “diminishing returns”-type thing.

Bernanke would like to boost growth, but he does not think that QE3 would be all that effective in accomplishing that objective. He thinks that the current high rate of headline inflation is likely to be short-lived. After all, for it to continue it would mean that oil prices would have to continue to rise at a fast rate from here, not just stabilize at the current high levels. Barring more Middle East disruptions, I think he is right there, especially for the rest of the year.

Longer term, I expect that oil prices will continue to rise relative to other prices. That simply reflects the higher costs of finding and developing oil fields to replace the super-cheap ones that are being depleted. The other side of the equation for high oil prices (shorter term) is the huge demand growth from the emerging markets, most notably — but not exclusively — China. There is not a whole heck of a lot that any Fed Chairman can do about that.

Bernanke on Inflation

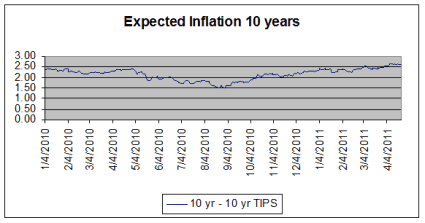

Like any central banker, he is worried about inflation, and in particular medium- to long-term inflation expectations. Since QE2 started last fall there has been a significant increase in the expected rate of inflation over the next decade.

The best measure of expected inflation is the difference between the regular 10-year T-note and the 10-year TIPS. That is a measure based on real people betting real dollars, not a flip response to a telephone interview. There is a very real consequence to making the wrong forecast when it comes to the TIPS spread; there is no consequence to making a bad forecast in a phone interview of what you think inflation will be over the next few years.

Since QE2 started there has been a 110 basis point increase in the expected level of average inflation for the next 10 years. However, for the most part, that just reversed a sharp decline in inflation expectations during the first half of 2010. Back then it looked like at least a temporary bout with deflation was likely. QE2 put those fears to rest.

The expected rate of inflation from the TIPS spread is now 2.60%. That is based on headline inflation, not core. It is very much within normal range that the economy has been able to live with very comfortably for the last 30 years.

Bernanke on the Dollar

While Bernanke did say that he thought that a strong dollar was in the country’s interest, he said the best way to accomplish that is to keep inflation low and the economy growing. Clearly, though, it was not his top priority.

The level and direction of the dollar feeds back into both growth and inflation. If the dollar is strong, then we pay less for the stuff that we import, and that helps keep inflation down. However, it also means that our exports are expensive. As a result, people abroad will buy products from competitors (including their own domestic manufacturers) that have relative weak currencies.

If the dollar is strong and the euro is weak, than an airline in China is more likely to buy from Airbus than from Boeing (BA). A hospital in France is more likely to buy MRIs from Siemens (SI) than from General Electric (GE). That means fewer jobs here.

A strong dollar also leads to a bigger trade deficit. Net exports, aka the trade deficit (or surplus), feeds directly into GDP growth. The improvement in net exports, a decline in the trade deficit, was the entire reason why we had solid growth in the fourth quarter. Had net exports not improved, we would have actually had a small decline in GDP in the fourth quarter, not the 3.1% growth we actually had.

Tomorrow we will get the first look at GDP growth in the fourth quarter. Based on the trade numbers we have seen so far for the first quarter, it is clear that net exports are going to be a drag on growth, and as a result GDP growth is likely to slow to less than 2%.

The trade deficit is THE reason we owe so much to the rest of the world — the trade deficit, not the fiscal deficit. That is not just an opinion, it is an accounting identity. The budget deficit plays in only indirectly. After all we ran massive budget deficits during WWII — much bigger than we are running now as a percentage of GDP — yet emerged from the war as the biggest net creditor the world had ever known (up until that point, depending on how you measure it, China today might have the U.S. of 1946 beat in that regard).

While many people are upset about the decline in the dollar, I think it is one of the best things the economy has going for it right now. Clearly we are not going to have residential investment lead us out of the current mess, nor will higher government spending. Net exports are going to have to be a key factor.

That is not going to make us that popular with the rest of the world. After all, any decline in the US trade deficit has to be matched, dollar for dollar with the reduction in some other country’s trade surplus, or an increase in another country’s trade deficit. Thus it would mean higher growth here, but lower growth somewhere else.

While I want to see the rest of world succeed, I am enough of a nationalist to prefer to see more of the world’s growth here. That is especially true when we still have unemployment running at 8.8%, and almost half of the unemployed have been out of work for more than six months.

Attack the Oil Part of the Equation

Yes, a weaker dollar means higher inflation, particularly for oil. We need to attack the oil side of the problem directly, not through keeping the dollar so strong that it chokes off the rest of the economy. Ultimately that means reducing our need for oil, and hence lowering demand. Some of that can happen through conservation and greater energy efficiency, but not all of it.

We need to develop alternative sources of energy. Top of my list for a replacement for oil in the short term is natural gas. We have massive amounts of it here in the U.S. thanks to the new shale plays. The technology of using it as a transportation fuel is well established, and we mostly use oil as a transportation fuel.

We already produce a lot of oil — we are the world’s number three producer and pump more than Iran, Iraq and Kuwait combined — and we have even seen a small rise in US production in recent years. However, we only have about 2% of the world’s proven oil reserves.

I don’t think drilling for more oil is a realistic solution. Longer term, we need to move to renewable sources, like wind, solar, geothermal and biomass from non-food sources (such as algae). Those, however, will take time to develop and scale up. Aggressive use of natural gas could happen much more quickly, and could pay huge dividends for the economy. More than half of the trade deficit comes from our addition to imported oil.

Ok I’m digressing a bit from the press conference. I think overall that conducting it in the first place was a good idea, and the quality of the questions was generally better than the ones he has to answer on Capitol Hill. He didn’t tell us a lot that we didn’t already know, but isn’t that the case with a lot of press conferences in Washington?

BOEING (BA): Free Stock Analysis Report

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply