I’ve had a number of articles on the topic of the Federal Financing Bank (“FFB”). This is the doghouse lender run by our good friend Tim Geithner. I check the reports on a monthly basis, there is always something that makes me laugh/cry.

-FFB is the lender of last resort for the good old Post Office. They have $12 billion outstanding to the PO. Interest rates? Don’t ask. The FFB is lending at 0.25%

-FFB has $600mm outstanding to various Universities. Once again the rates are dirt-cheap. The maturities? Some go out to 2028

-FFB is also the lender to Ford, Tesla, Fisker, Solyndra, Arizona Solar and Kukuku Wind. The amounts outstanding to private sector names now totals $4 billion.

-Even the military is involved. The FFB has $370mm outstanding under the dubious heading of “Military Sales”. I wonder just whose military are we financing with that loot.

The FFB came out with its annual report recently. An outside auditor, KPMG, performed the audit. I poured through all 24 pages. The second to last paragraph caught my eye:

We noted certain matters that we have reported to Bank management in a separate letter dated November 10, 2010.

A separate letter? What’s that about? My read of this is that the nice folks at the KPMG had something they wanted to say to the management of FFB, and they did not want the contents of that letter to be public. By the way, Tim Geithner is the Chairman of the FFB. So he is the “management” that got the letter that we can’t see.

I love side letters. You have to assume that a dozen or so lawyers and accountants looked at the final draft of the report and argued about the necessity to put in the language that is confusing me. After all, if the side letter is a secret why make it known that there is a side letter to begin with? Possibly a bit of CYA on the part of good old KPMG.

So I contacted the FFB and asked them what this was about and haven’t heard a word. The fact is that I don’t know what might be in that letter. But because I don’t have the answer from Treasury I think I am allowed to speculate on just what this might be about. If I’m wrong, then Treasury can let me know and I’ll publish a correction.

There are some things going on at FFB that don’t quite pass my smell test. Consider this from the Annual Report:

FEDERAL FINANCING BANK

Notes to Financial Statements September 30, 2010 and 2009 (Dollars in thousands)Additionally, at September 30, 2010 and 2009, the Bank had borrowings of $10,238,990 and $11,921,240 and an associated unamortized premium of $180,007 and $228,927, respectively, from the Civil Service Retirement and Disability Fund (CSR&DF), which is administered by the Office of Personnel Management (OPM).

Why would the Civil Service Retirement fund lend money to FFB? $22 billion is not chump change. It’s a third of FFB’s total liabilities.

CSR&DF has a surplus and invests that money in Special Issue Treasury securities in its normal operations. This is exactly the same for the other federal trust funds. Social Security is a perfect example. SS holds $2.6 trillion in Special Issue Treasuries. But it does not hold a penny of paper issued by the FFB. Why is the CSR&DF lending FFB 22b? The answer is not that the FFB is having any difficulty in raising money directly from its parent (Treasury). The rules are pretty clear; FFB has a blank check:

The Bank is authorized to issue obligations in unlimited amounts to the Secretary and, at the discretion of the Secretary, may agree to purchase any such obligations. (BK note: Secretary = Geithner)

I wonder if the unusual funding arrangement between FFB and CSR&DF is in anyway connected to this sentence from the KPMG report:

While the Bank is permitted to charge a spread on new lending arrangements with government-guaranteed borrowers, the margin is not retained by the Bank, but rather is retained by the loan guarantor.

Ah!! Spread income is diverted out of FFB back to some Agency. How much? What Agency? Why is any Agency in the credit business?

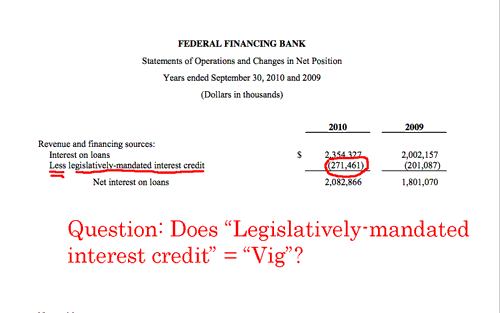

I can’t answer any of these questions. I wish I could. I think the answer on “How much” is in the line item marked: Legislatively mandated interest credit. It only comes to $270 million. Chump change, right?

UPDATE: Shortly after I posted this piece I did hear from the FFB. They sent me a link to the letter I make reference to below. The letter is not a smoking gun. It deals with minor security issues. Rather than “fix” the following I’ll leave it the way it is. The matter of the side letter is resolved. The other points I make are still valid. The FFB borrows money from the Civil Service retirement fund. This is unusual in comparison to other federal Trust Funds. Some of this money is on lent with the benefit of a “guaranty” from the federal Agency making the loan. A “spread” is paid to the Agency. The original piece, warts included.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply