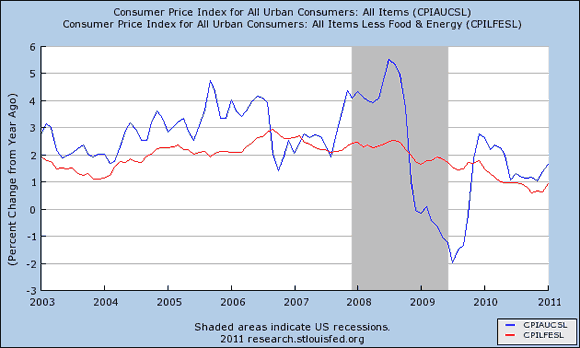

The BLS reported on Thursday that the inflation rate as measured by the headline CPI has been 1.6% over the last year. Excluding food and energy, the inflation rate would be 1.0%.

Annual inflation rate as measured by headline CPI (blue) and core CPI (red), 2003:M1-2011:M1. Source: FRED

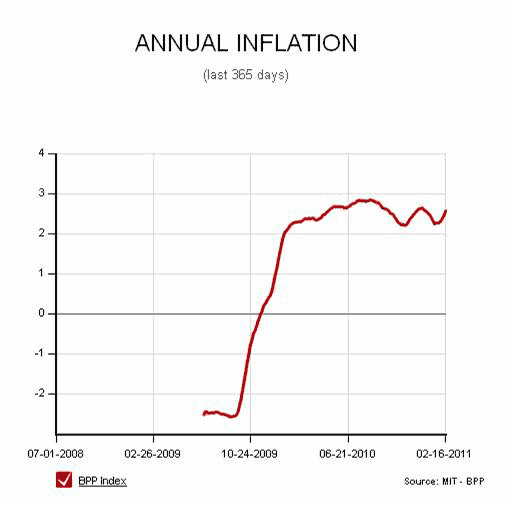

The MIT Billion Prices Project is recording a slightly higher inflation rate for the U.S. of about 2.5%. As Paul Krugman explains, the discrepancy between the indexes arises from the fact that the BPP excludes the cost of services, which have been experiencing more modest price increases than goods. The Wall Street Journal has more on the different inflation rates for goods and services.

U.S. annual inflation rate as estimated by Billion Prices Project

The BLS CPI does register a modest tick up from recent values. If the increase in the CPI for the months of December and January alone were to be repeated for the next year, we’d be looking at annual inflation rate of 5% for the headline CPI and 1.4% for core CPI. Should we be concerned that this is the first move toward a higher inflation environment?

The biggest factor in most firms’ costs is their wage bill. The unemployment rate is still at an extremely high 9%, and I don’t expect it to come down quickly. We’re also seeing solid gains in productivity. In those circumstances, telling a story of inflation driven by wage costs seems more than a little far-fetched.

There’s also much discussion of inflation pressures arising from all the money that the Federal Reserve is supposedly printing. But as noted here last week, currency in circulation has actually been growing at a 5.2% rate over the last two years, which is lower than the historical average, and, given real output growth in excess of 3%, is consistent with the very low rates of inflation confirmed in the latest observed annual inflation rates.

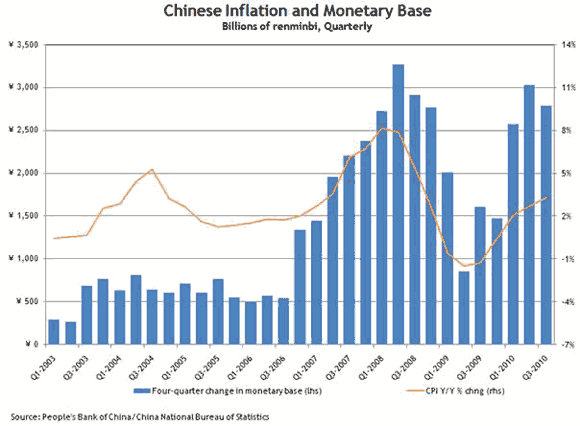

The main source of inflationary pressure today is coming from outside the United States. There are two factors in this. First, real economic growth at the moment is much stronger in emerging markets than here. Second, countries such as China have kept their exchange rates artificially low relative to the dollar.

Macroblog has a nice discussion of this issue. If a country tries to keep its nominal exchange rate from appreciating by using monetary policy to buy up foreign reserves, the predicted outcome is inflation in their own country.

Source: Macroblog

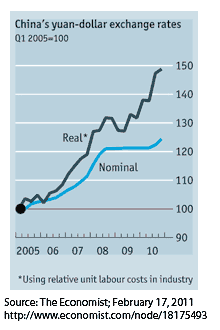

If the nominal exchange rate is prevented from doing the adjusting, the real exchange rate must.

Source: Economist

For these reasons, I see the principal inflationary pressures in the U.S. at the moment coming from the prices of internationally traded commodities and imported goods. Given the huge volume of U.S. imports from China, I think the impact from the latter channel could be noticeable.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply