The Milken Institute is thumping the drum for another mortgage modification program. This one would have the government make mortgage lenders whole and take the burden of negative equity off the shoulders of the homeowner.

From the LA Times, here is what they propose:

One proposal for a debt-forgiveness program was floated this month by the Milken Institute in Santa Monica. The plan, authored by institute President Michael Klowden and regional-economics director Ross DeVol, would refinance existing mortgages of underwater homeowners with new loans from the government.

Klowden and DeVol call it the “homeowner principal forgiveness vesting plan.” Here’s how it would work:

Say an owner’s mortgage is worth $400,000 but his house is valued at $300,000. The government would refinance the $400,000 loan with two new loans. Fannie Mae, the mortgage financier now under government control, would provide a first loan for the market value of the house, in this case $300,000. The Treasury would issue the second loan, in this case for $100,000.

The Treasury loan would be interest-only and would provide the vesting part of the program. For each year that the homeowner keeps up payments on both loans, one-fifth of the Treasury loan would be forgiven.

“This gives homeowners the incentive of returning to a positive net-equity position before their hair turns grey — maybe even in time to pay for their children’s college education,” Klowden and DeVol wrote in a summary.

They estimate that the cost to Treasury (and thus to taxpayers) of saving 1.5 million homes from foreclosure or abandonment with this plan would be between $75 billion and $100 billion. That assumes the government wouldn’t jeopardize the original lenders’ balance sheets by forcing them to share in the cost via haircuts on their loans.

DeVol concedes that the Milken proposal would be a handout to the usual suspects in the housing crash — mainly, California, Florida, Nevada and Arizona — because those are the places where the negative-equity problem is dire.

I kind of thought we were past these ideas, you know, Obama has his plan out there working, it’s supposed to be saving more and more homeowners every day and lots of pundits keep saying that things are settling down in housing. So what’s the point in rolling this out now?

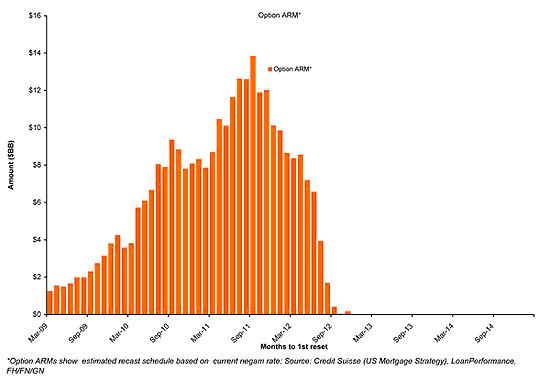

I’ll confess to not knowing the answer to the question but I suspect that it has something to do with Option ARMs. That would seem to be the biggest shoe left to fall and certainly the place where you’re going to see a lot of negative equity. If that’s the case then there is likely to be a lot of push back on this idea or anything similar.

As the article points out, the plan would be aimed at a group of borrowers that are able to afford their mortgage, they just don’t want to keep paying because they’re under water. In other words, I made a bad deal now someone get me out of it. Once you bail one of these borrowers out, how many others do you expect will continue to make their mortgage payments. If you guessed zero go to the head of the line. Once the word was out on this one it would be “Katy, bar the door.”

I don’t want to belabor this again. I’ve written about it extensively as have others. There is just too much give away in this type of scheme. Borrowers that had no equity to begin with are going and were effectively renters get bailed out. Option ARM holders who chose to use the negative amortization feature of their loans thus putting them farther into the hole were living on the cheap and now get bailed out on the taxpayers’ dime. There is so much wrong that it’s hard to find justification for the program.

Hopefully, this is just more think tank drivel. I don’t want to see this subject gaining traction once more.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply