Ben’s got his head in the sand?

The WSJ reported on the Fed’s (AKA:Bernanke World) reaction to the significant rise in long term interest rates since the 11/3 announcement of the policy:

Federal Reserve officials were unfazed by a rise in long-term interest rates at their December policy meeting.

Unfazed? I don’t think this is true at all. The backup in LT yields is exactly what the Fed doesn’t want. I think they are crapping in their pants over this development.

Fed officials have argued that bond yields would be even higher and financial conditions tougher if the central bank hadn’t started the purchases.

“Look at the graph guys; it’s QE that done it” is all I can say.

Fed officials noted that the tax-cut compromise between President Barack Obama and congressional Republicans had likely pushed rates higher by putting upward pressure on the budget deficit.

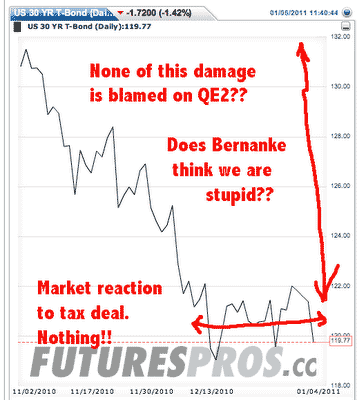

Baloney! Here’s the graph. Rates did not go up in the last weeks of December when the tax plan was approved. The Fed is blaming Congress for the bond market blow out? Weasels.

QE2 has created great uncertainty. We are six months (functionally five) away from the program’s end. No one has a clue what will come next. Uncertainty like this ALWAYS increases long-term bond yields. There are really only two possible explanations for the Fed’s refusal to acknowledge that QE2 has directly contributed to rising bond yields:

(I) They have absolutely no clue what is going on in the bond market. They have not read word one of the thousands of articles that have connected the dots between QE2…Uncertainty…Higher yields.

(II) They are lying to us.

I have never made the mistake of underestimating the Federal Reserve. Some of the brightest/best connected people in the world of finance are involved. They know exactly what is going on in great detail. They are keenly aware of all information that is made public regarding their activity. They speak with a broad spectrum of financial players including all the big banks, the primary dealers and the big bond-holders inside and outside of the United States. I don’t think they are clueless at all…..

An interesting (to me) side-story in China

A tax-lawyer friend sends me this note on the issue of transfer pricing in China.

Re PRC and inflation, they have been ramping up enforcement of tax rules that back-stop their capital controls to combat movement of hot money contributing to inflation. The tax rules are transfer-pricing, which govern the pricing of related party transactions, since those are a way to move money from one country to another, but keep it in the economic group. Evidence that PRC will try to combat hot money and inflation, which isn’t to say they’ll actually succeed!

From China-Briefing comes this on the transfer pricing issue:

Representative offices in China may find themselves having to comply with China’s transfer pricing regulations for the first time in the upcoming annual audit period. ROs and other foreign investments must now start to prepare their accounts for the year 2010 and to have these fully prepared for submission no later than the end of April 2011. Negotiations after audit submission have little chance of success.

These are significant regulatory changes. They will alter the way business is done for foreigners in China. Profits for some companies (car companies) will fall as a result. I read this as just more evidence that China is pulling out all the stops to combat inflation. What does this mean? The inflation problem is bigger than we think and growth is going to slow.

A break in the weather?

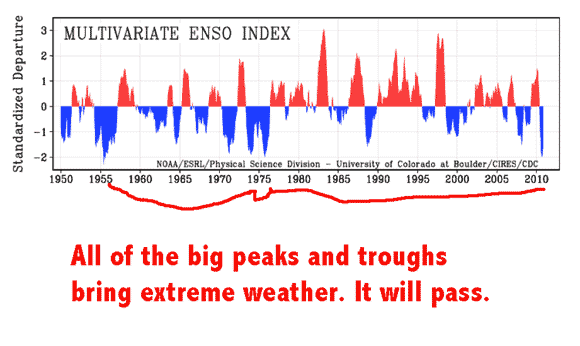

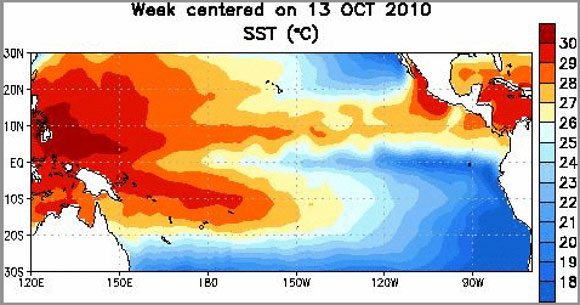

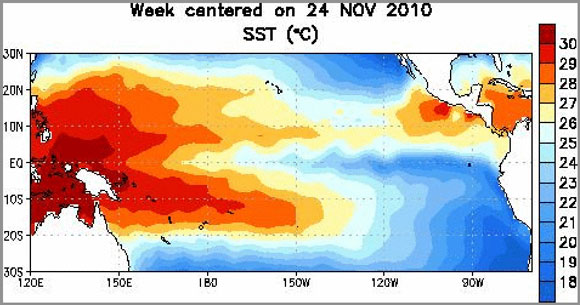

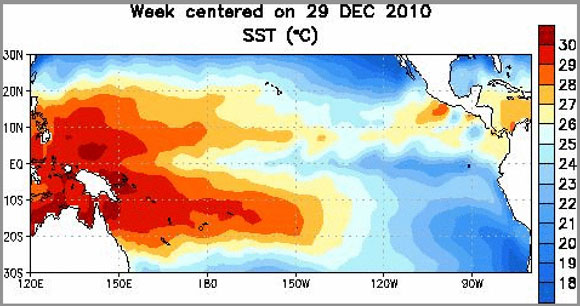

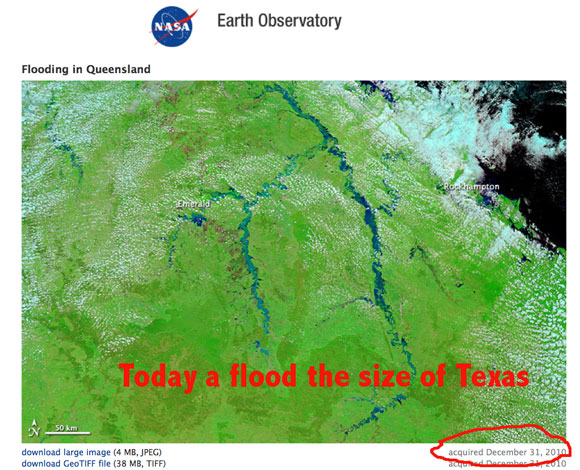

50-year weather records are being set around the globe. Rainfall in Australia/California is at the 50 year mark. The European weather has set the same records. It’s true for all of Asia and most of South America as well. Why now? For me it is La Nina. This change in pacific water temperature drives all weather patterns. It too is at a 50 year low. This chart show the current extreme condition:

These time elapses show how the hot water just slammed into Asia in the last few months.

Looking at the long term ENSO chart you see the rapid switches between El and La conditions. The cycles always end with blow out weather conditions. The violent storms suck the heat from the water and with that a new cycle begins. The next ENSO report is on Jan 7. I’m betting the cycle broke and with it the weather extremes.

Social Security: Terrible 10’; questionable 11’; a thought on NFP

The full year (including adjustments) came it at $49 billion in negative cash flow. In June I wrote about my expectations. My conclusion back then: “This translates to a~$50b deficit for the full year.”

The raw numbers for January’s payroll tax and expenses are out. Nothing new. Revenues down, expenses up.

January is always a surplus month as taxes come in. The YoY is down again however. The full year cash flow will be in the red again this year. I am projecting $35b of negative cash flow. (SSA forecast is -4b)

I look at the payroll tax data in the context of the Non Farms Payroll numbers. Does the data from SSA have any predictive information on this critical monthly statistic? Not with any precision; has been my experience (and frustration) to date.

With that as a caveat, I have looked at this and concluded that the ADP report this morning suggesting a 300k increase in payrolls is overstating the number. We shall see soon enough.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply