There was a bit of angst regarding yesterday’s Conference Board consumer confidence report. See, for example, Mark Thoma and Brad DeLong. The report appears to contradict the generally positive Univ. of Michigan report – still weak compared to pre-recession, but at least moving in the right direction. More interestingly, it is at odds with recent consumer spending reports, not just early reports of the best Christmas season (in terms of year-over-year gains) since 2005, but also the most recent trends in personal consumption expenditures.

Something is off-kilter, and has been since mid-year. Consumer confidence appears too low relative to actual consumption. Either confidence should be moving higher, as the Univ. of Michigan survey suggests, or consumption needs to slow dramatically. Place your bets.

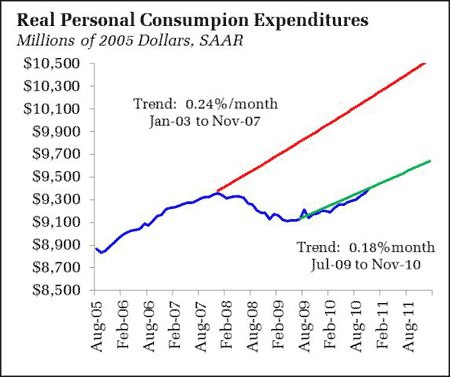

Consider the recent trends in real consumer spending (percentage change are log difference approximations):

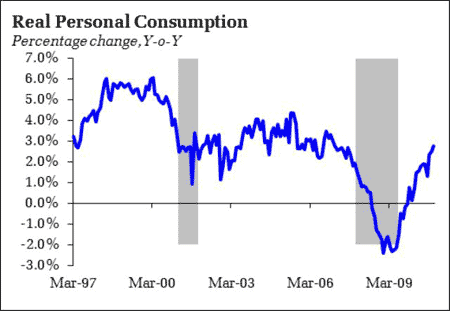

To be sure, the trend since the recovery began is decidedly lower than the pre-recession trend. But this trend hides a recent acceleration. Average monthly growth for 2010 to date is 0.2%, but for the most recent three months (Sept.-Nov.), the rate accelerates to 0.35%, well above the pre-recession trend and, dare I say it, something much more like the kind of “catch-up” we would be hoping to see – or would have been hoping to see earlier in the recovery. The pessimist in me, however, tends to think this acceleration is not entirely sustainable. Pessimism aside, this kind of growth has driven a nontrivial acceleration in the year-over-year figures:

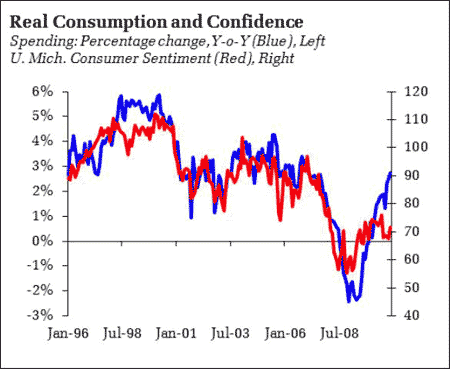

Now, compare year-over-year consumption growth with consumer confidence (UMich., because I have those charts on hand):

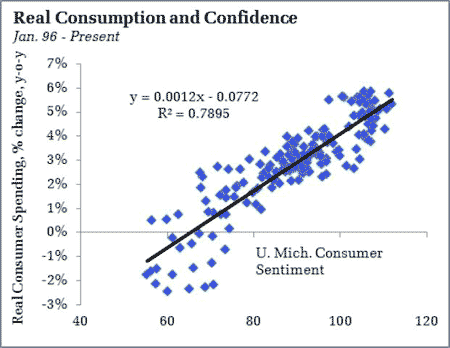

Note the divergence beginning in July of last year – confidence tumbles, and stays low despite growing real consumption. To be sure, this is a noisy relationship, but it appears the last five readings are anomalous. Consider a scatterplot and simple linear regression:

Now isolate the five most recent observations:

They are all consistently above the fitted regression line, and the one-sided nature of the error is sufficient to slightly lift the R-squared of the regression. Also note that the most recent reading, with UMich. confidence rising to 71.6, is a movement in the “right” direction, toward the fitted line.

But here comes the hard part – a movement in the “right” direction could also occur if consumption growth slowed, pushing the year-over-year figures to the 0.5-1.0 percent range. The expected policy path will obviously depend on which “right” move occurs. If confidence rises to match spending, expect the Fed to draw large scale asset purchases to a close when the current program expires. Also expect that the Administration will feel more confident to give the go-ahead to spending consolidation. Expect the opposite if spending growth falls to match confidence.

The reasons to expect more tempered spending growth in the months ahead are well known at this point. Weak job growth, need to rebuild wealth and/or the flip side of need to reduce debt loads, the related weak housing market (also angst over the Case-Shiller numbers yesterday, but I will try to address that tomorrow night), impending retirement needs, threat of zombie apocalypse, etc.). A seemingly endless list of pessimism, to be sure. And well justified pessimism at that. Still, all of these factors have been in play for the past year, yet consumer spending accelerates as if households are in blissful ignorance. Perhaps they are.

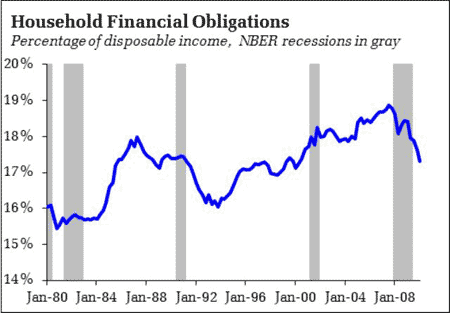

Ignorance aside, I think the acceleration needs an explanation of some sorts. Throwing out some ideas, first note that household balance sheets are in a better position, at least measured by the debt servicing costs:

Also, saving rates are well above pre-recession lows:

Consumption can be supported by taking savings rates back down to zero, or close to it. To be sure, you can respond angrily that consumers desperately need to rebuild their asset base, that policies such as ZIRP that encourage spending simply kick the can down the road, etc. And these things might be true. But, in the near term, one cannot deny the potential for consumer spending support via a falling saving rate. This is especially important given occasional concerns about rising oil prices. When the last oil shock hit in 2006-7, saving rates were hovering around 2%, not much cushion to absorb the shock. At least at 5.3% consumers have a little more wiggle room.

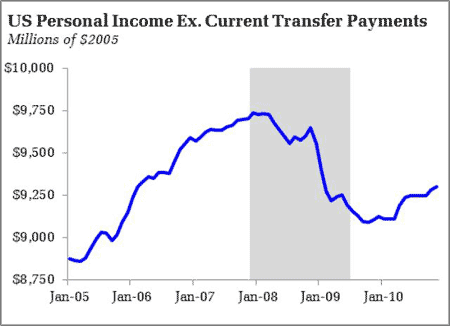

Finally, real income less transfer payments are on the rise:

Yes, yes, yes, well below pre-recession peaks and trends. But the direction is decidedly positive, and provides support for accelerated spending. And it provides some cushion as the 99er’s fall off the insurance rolls.

Bottom line: Consumer confidence figures appear inconsistent with actual spending patterns. That inconsistency will be resolved by either confidence rising or falling spending growth, with more or less obvious policy implications. There will be a tendency to assume the resolution will come from decelerating spending growth. To be sure, the recent trend appears unsustainable. But I also think it is worth paying attention to the more positive household spending data.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

The increase in spending is due to inflation, that explains the contradiction.

high fuel prices doesn’t help either,gas goes up consumer confidence goes down.