If history is any guide, the Chinese renminbi will soon be due to overtake the US dollar, just as the dollar replaced the pound sterling last century. But will the renminbi be ready for reserve currency status? This column discusses the issues at hand and explains why some experts would prefer the IMF’s Special Drawing Rights as the next global reserve currency.

Just ahead of the G20 London Summit in April, Zhou Xiaochuan (China’s central bank governor) proposed replacing the US dollar as the international reserve currency with a new global system controlled by the IMF. The main global reserve currency would be represented by a basket of significant currencies and commodities, an extended version of the Fund’s Special Drawing Rights (SDRs). China’s call for an overhaul of the global currency reserve system has been echoed by Russia’s President Medvedev as an important building block of a new global financial architecture.

Major emerging economies, often net creditors to the rest of the world an with substantial holdings of US government debt, fear the potential inflationary risk of the US Federal Reserve printing money to finance bank bail outs. Their fears may be based on the “Triffin Dilemma” that postulates the necessity of US external deficits as long as the US dollar is the only global reserve currency. In a famous warning to Congress in 1960, the Belgian Yale economist Robert Triffin explained that as the marginal supplier of the world’s reserve currency, the US had no choice but to run persistent current account deficits. As the global economy expanded, demand for reserve assets increased. These could only be supplied to foreigners by America running a current account deficit and issuing dollar-denominated obligations to fund it. If the US stopped running balance of payments deficits and supplying reserves, the resulting shortage of liquidity would pull the global economy into a contractionary spiral (Triffin, 1961). Note that demand for foreign exchange reserves forces developing countries to transfer resources to the countries issuing those reserve currencies – a case of “reverse aid”.

China holds a huge official portfolio of US government bonds. It has already suffered valuation losses on its sovereign wealth funds that invested heavily in US financial intermediaries. But could China suffer valuation losses as a result of inflation and dollar devaluation, as is often maintained? Dollar weakness – against other key currencies – will not by itself inflict valuation losses on China’s central bank as there would be no change in the renminbi value on the dollar component of China’s huge FX reserves. It is renminbi appreciation against those currencies held in the FX reserves – often claimed by the West – that would inflict valuation losses as measured in renminbi.

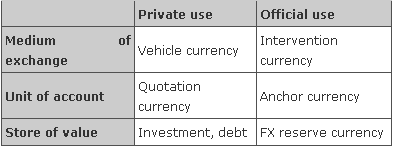

In the recent decade, the US has used (and perhaps abused) the privileges that its reserve currency status has conveyed to the host country. To see this, look at Table 1, which displays a matrix of the global functions of money often attributed to Peter Kenen (Group of Thirty, 1983).

Table 1. Matrix of international currency use

By enlarging the scope of issuers and investors, the reserve currency lowers borrowing costs and facilitates balance of payments financing; Americans have outspent their national income by an accumulated 47.3% of GDP since 2000, depressing US treasury rates until 2005 up to 130 basis points as the world (mostly Asia) reinvested the corresponding surpluses mostly in US treasury bills (Warnock & Warnock, 2006). The additional demand for money creates seigniorage revenues; last year the US Fed made a net interest income of $43 billion, as the US dollar in circulation is, in effect, an interest-free loan by the public to the central bank (Economist 2009). And, though its benefits are harder to quantify, currency use in key markets for commodities or trade invoicing shifts exchange rate risk to third countries, insulating the reserve currency host country.

In turn, the US dollar is providing (microeconomic) network benefits; it has the attributes of a natural monopoly – like the English language these days. (By contrast, the IMF’s Special Drawing Rights – SDRs – are no more than the equivalent of Esperanto). Sixty-four percent of the world’s official foreign exchange reserves are currently held in US dollars; roughly 88% of daily foreign exchange trades involve US dollars (Humpage, 2009). Global trade is facilitated by the use of just one currency, liquid debt markets allow Central Banks to intervene in foreign exchange markets as to smooth currency fluctuations, savers can escape inflationary governments by deposit dollarization, and commodities can be priced homogenously wherever traded.

While the US has been enjoying the spoils of reserve currency status, this is by no means assured for the future. As emphasised by Avinash Persaud (2004):

“…reserve currencies come and go. They don’t last forever. International currencies in the past have included the Chinese Liang and Greek drachma, coined in the fifth century B.C., the silver punch-marked coins of fourth century India, the Roman denari, the Byzantine solidus and Islamic dinar of the middle-ages, the Venetian ducato of the Renaissance, the seventeenth century Dutch guilder and of course, more recently, sterling and the dollar.”

Is the renminbi the next global reserve currency?

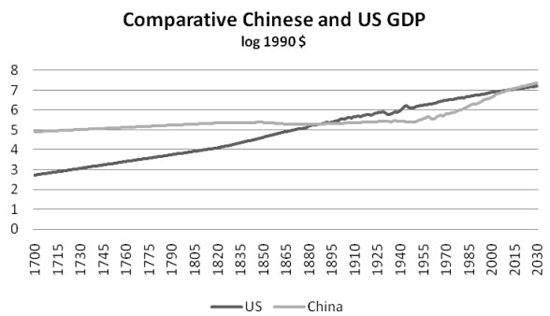

If history of the last switch in reserve currency (from pound sterling to the US dollar) is any guide, the Chinese renminbi can be expected to replace the US dollar as a reserve currency around 2050. The UK lost its position to the US as the world’s largest economy in 1872 and the largest exporter in 1915. The switch in net debtor/creditor positions started 1914, and as the US dollar emerged as a convertible net creditor currency, its use in finance and trade widened. By 1945, the pound was dethroned (Chinn and Frankel, 2008). Today, the US is in a net debtor position similar to Britain after the WWI, with China being the world’s largest creditor. In PPP terms at least, Angus Maddison predicts that China will surpass the US by 2015; China is on its way to becoming the world largest exporter. So these historic parallels might imply a switch in the reserve currency by the mid-21st century.

Figure 1. China’s re-emerging supremacy

Source: Maddison (2007)

Nowadays, the renminbi is far from ready to achieve reserve currency status. China would first have to ease restrictions on money entering and leaving the country, make its currency fully convertible for such transactions, continue its domestic financial reforms, and make its bond markets more liquid. Hong Kong has had the freest capital account for two decades, according to the Chinn-Ito index. Moving from closely managing its currency to greater market determination, China’s renminbi would appreciate against the US dollar and thus alleviate several concerns – the China-US imbalances would shrink and China could lower its risky exposure to dollar-denominated assets. But it would incur renminbi valuation losses on its key currency assets.

Change is underway. China has already flexed its muscle by setting up currency swaps with several countries (including Argentina, Belarus and Indonesia) and by letting institutions in Hong Kong issue bonds denominated in renminbi, a first step toward creating a deep domestic and international market for its currency. Brazil and China are now working towards using their own currencies in trade transactions rather than the US dollar. Invoice of more trade in emerging-market currencies suggests that the US will no longer enjoy full seller finance on its trade deficit.

Special drawing rights

The Commission of Experts of the UN General Assembly on Reforms of the International Monetary and Financial System, led by Joseph E. Stiglitz, has suggested a gradual move from the US dollar to the SDR. Following upon the G20 Summit in London, the IMF is issuing Special Drawing Rights worth $250 billion. This will increase the share of SDRs in total international reserves to no more than 4%. So some specific steps are needed to improve the role of the SDR as a global reserve asset.

In order to make the SDR the principal reserve asset via allocation, close to $3 trillion in SDRs would need to be created. Onno Wijnholds (2009) has thus suggested a so-called SDR Substitution Account. The idea is to permit countries whose official dollar holdings are larger than they desire to convert dollars into Special Drawing Rights. Conversion would occur outside the market and thus would not put downward pressure on the dollar. This suggestion, however, requires settling who will bear the exchange (dollar) risk as the SDR Substitution Account is likely to mostly hold dollars as assets.

Another step to enhance the role of the SDR is to make its currency composition more neutral to global cycles and more representative of the shift in economic power witnessed over the last two decades. This implies an increase in the commodity content and the inclusion of major emerging-market currencies. Today, the SDR is constituted as a basket of four fiat monies. To the extent that free convertibility is required for inclusion into the SDR composite, the Australian, Canadian, Chilean and Norwegian currencies could be included to give the SDR a link to the raw material cycles, as these currencies proxy price developments of copper, iron ore, gold, and oil. Major emerging-country currencies would be included in the SDR mix as soon as they reach a predefined level of convertibility.

Other avenues to better the reach of the SDR as a reserve asset are to improve its trade invoice and vehicle functions. Pilot programmes such as the Real/Renminbi deal mentioned above could be extended as could regional currency arrangements; the proviso is that they should not introduce friction and higher transaction costs into regional and global trade. IMF bonds issued in SDR are already much in demand, reflecting concerns about the dollar, and will enhance its store of value function.

References

•Chinn, M. and J. Frankel (2008), “Why the Euro Will Rival the Dollar”, International Finance, Vol.11.1., pp 49-73.

•Economist, “The Hedge Fund of Foggy Bottom”, 30 April 2009.

•Humpage, O.F. (2009), “Will special drawing rights supplant the dollar?”, VoxEU.org, 8 May.

•Kenen, P. (1983), “The Role of the Dollar as an International Reserve Currency”, Occasional Papers No.13, Group of Thirty.

•Maddison, A. (2007) Chinese Economic Performance in the Long Run, OECD Development Centre 2007.

•Persaud, A. (2004), “Why Currency Empires Fall”, Gresham Lectures.

•Triffin, R. (1961), Gold and the Dollar Crisis, Yale University Press.

•Wijnholds, O. (2009), “The Dollar’s Last Days?”, Project Syndicate, May.

![]()

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply