Large external imbalances persist and remain a significant concern. This column estimates a set of medium-run “fundamental equilibrium exchange rates” compatible with moderating external imbalances that might guide international policy efforts. It says that the US dollar is overvalued and the Chinese renminbi is undervalued.

Most writing about exchange rates forecasts how exchange rates are about to change. Most of these writings are not worth the paper they are written on – short-run exchange rate movements are, to a good approximation, a random walk (Meese and Rogoff 1983). We believe it to be socially more valuable to attempt to evaluate what exchange rates could help to support a viable medium-run equilibrium position for the real economy. That is the purpose of the estimates of “fundamental equilibrium exchange rates” we prepare (of which the latest are in Cline and Williamson 2009).

Assumptions

In undertaking such an exercise, one needs to make assumptions both about the course that external balances would take if policy did not attempt to address these disequilibria, and assumptions about the objectives that should be sought by policy (as well as assumptions built into the model deployed). In our most recent work we have employed as a frame of reference most of the assumptions reflected in the IMF’s latest World Economic Outlook for 2012. Unfortunately we think the IMF is too complacent in forecasting that at the exchange rates of last March the US current account deficit would basically stabilise at 3% of GDP (the forecast for this year) rather than suffer a new deterioration, and that the oil price would stabilise next year at a real level of $62.50. We therefore modified the 2012 current account forecasts of the IMF model in two respects – by adding to the IMF forecast for each country other than the US a sum equal to their proportionate share of the increased US deficit that would materialise under Cline’s forecast, and the impact of the higher oil price. After adjustment to secure international consistency, this gave us forecasts of actual current imbalances.

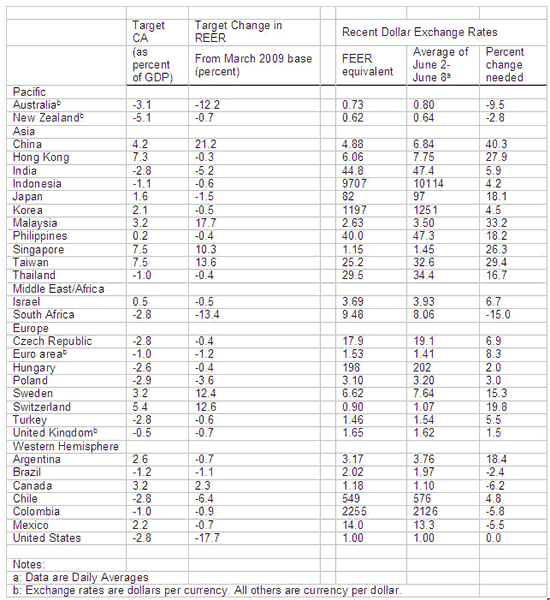

The key assumption regarding objectives is what current account target should be pursued by each country. We employed two rules to determine these, based on the philosophy that countries should be left alone except where their decisions either impinge on the rights of others or jeopardise their own stability. In general we argued that countries should strive to keep imbalances (surpluses and deficits) under 3% of GDP. Reflecting the philosophy, countries with smaller forecast adjusted imbalances were assumed to be within the target range and require no adjustment. However, we recognised that countries with large inherited stocks of foreign assets or liabilities might have difficulty in achieving this aim, so countries with a forecast imbalance in excess of an absolute 3% of GDP were treated as also within the target range provided that the a larger imbalance did not threaten to further increase the absolute ratio of net foreign assets to GDP. This gave figures for presumed desired current imbalances (see Table A at the end of this column). The gap between each country’s forecast current account balance and the target limit (either 3% of GDP or net foreign assets-based) constituted the desired change in current account balance to be accomplished.

The model employed to translate assumptions about the difference between forecasts and desirable outcomes into exchange-rate estimates was Cline’s work, notably his estimates of impact parameters (which measure the impact of a change in real exchange rates on current account outcomes) and his Symmetric Matrix Inversion Model (SMIM) (Cline 2005, 2008). The desirable changes in current account outcomes and the impact parameters gave desired changes in real effective exchange rates.¹ The purpose of the SMIM is to convert the set of desired changes in real effective exchange rates into a set of changes in dollar exchange rates.

Dollar overvaluation, renminbi undervaluation

The table shows the results of these exercises for the 29 countries for which we formed estimates.² The target changes in the real effective exchange rate are against the March 2009 base used in the IMF forecasts. Because the dollar has declined significantly since then (by about 5% on a trade-weighted basis), in some cases the extent of correction needed now is considerably smaller, and some currencies have even overshot.

The euro area and even the UK are still found to be marginally undervalued against the dollar, though both are slightly overvalued on a multilateral basis. The same is true for Japan and indeed a majority of the small currencies. Both of the immediate neighbours of the US, Canada and Mexico, are now estimated to be somewhat overvalued against the dollar, even though in March the Canadian dollar was undervalued. The only other currencies found to be more than marginally overvalued against the US dollar are the Australian dollar and the South African rand.

The main counterpart to the overvalued dollar is the undervaluation of the Chinese renminbi, along with a few of the smaller Asian currencies. We are somewhat nervous because our estimate (based on the figure of RMB 4.88 to the dollar) of Chinese undervaluation is even larger than it was a year ago (RMB 5.81 to the dollar), despite the fact that the RMB rode the dollar up by 14% in effective terms in the intervening year. It may be that our estimate is now too large because the IMF’s projection of the Chinese surplus seems not to have declined despite the RMB’s real appreciation, although the fall in commodity prices in the past year has presumably worked in China’s favour. But all the other potential biases, notably the way of formulating the Chinese current account target as a substantial surplus rather than the deficit suggested by the FDI inflow, are in the direction of minimising estimated undervaluation. Our analysis is one more piece of evidence that the major macroeconomic imbalance in the world today stems from China’s exchange-rate policy.

Moderating external imbalances

Whatever one thought about the importance of moderating external imbalances a year or two ago, one’s concern about the importance of reducing imbalances should be greater today. We are not among those who argue that the primary cause of the financial crisis was a savings glut in Asia – China’s surpluses did not force the quants to invent asset-backed securities, the rating agencies to overrate mortgage-backed securities, AIG to take a position on only one side of collateralised debt swaps, nor Lehman and others to leverage at 30 to 1.

But the system is far more fragile than we had thought two years ago. Large external imbalances can only aggravate, not moderate, fragility in the financial system. One sign of that fragility is Chinese nervousness about whether it should continue to build up US Treasury securities. Moreover, in a world economy fighting global recession, it is especially important to avoid the competitive devaluations that spurred increasing conflict and protection between the two world wars and led to the Bretton Woods system of fixed exchange rates. A meaningful pursuit of reduction in international imbalances and corrective movement in exchange rates has been on the international agenda for some time now, including in the IMF’s mandate to provide multilateral surveillance. It is in this context, then, that we prepared this second set of “fundamental equilibrium exchange rates” estimates, and we hope that they will provide a useful input into international policy efforts toward reducing imbalances.

References

•Cline, William R. (2005). The United States as a Debtor Nation. Washington: Institute for International Economics.

•Cline, William R. (2008). Estimating Consistent Fundamental Equilibrium Exchange Rates. Working Paper 08-6. Washington: Peterson Institute for International Economics.

•Cline, William R., and John Williamson. (2009). 2009 Estimates of Fundamental Equilibrium Exchange Rates. PB09-10. Washington: Peterson Institute for International Economics.

•Meese, R.A., and K. Rogoff (1983). “Empirical Exchange Rate Models of the Seventies: Do They Fit Out of Sample?” Journal of International Economics 14, 3-24.

Appendix

Table A. Key results

1 The current account targets and the changes in real effective exchange rates relate to the period for which the IMF made forecasts, which was March of this year. But from this we calculated “fundamental equilibrium exchange rates”-consistent dollar exchange rates which (since this is not an age of high inflation) can be assumed to have remained constant, thus permitting the comparisons with recent market exchange rates in the final columns of the table.

2 Four oil-exporting countries – Norway, Russia, Saudi Arabia, and Venezuela – are included in the analysis, but “fundamental equilibrium exchange rates” were not estimated since these depend critically upon savings strategies and the oil price and we have no credible forecasts of these variables. The rest of the world was forced to have zero change in its current balance, but there is no corresponding currency.

![]()

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply