This year the Xmas decorations appear to have gone up earlier than ever leaving the wait for Xmas inexorably long. And so it has been with the wait for Santa Ben. But at last it is FOMC Eve and we are sure we are not alone in feeling jubilation that finally Santa is about to come down the chimney and leave all of us market participants the presents we’ve been waiting patiently for. He always gives good presents. Let’s just hope that he doesn’t forget to include the batteries.

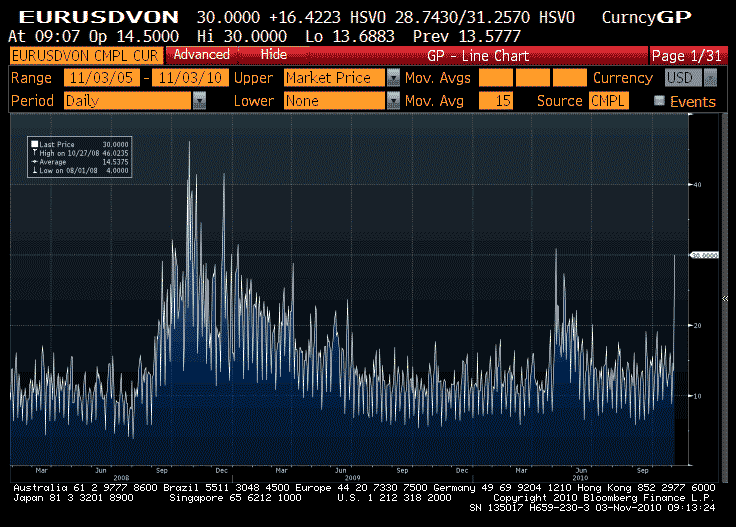

In terms of anticipation, the FX option market is pricing the highest overnight volatility (see chart below) since the depths of the EMU-crisis in May. And for good reason. We are unsure exactly what market expectations are, although it seems something in the region of $500-600 Gigadollars over six months is the consensus, at least from the surveys we have seen from economists and traders. But even if we knew the outcome of today’s meeting, we have no idea how markets will react, with contradicting anecdotes about positioning and reactions leading them to conclude that sitting on the sidelines seems like the best strategy.

(click to enlarge)

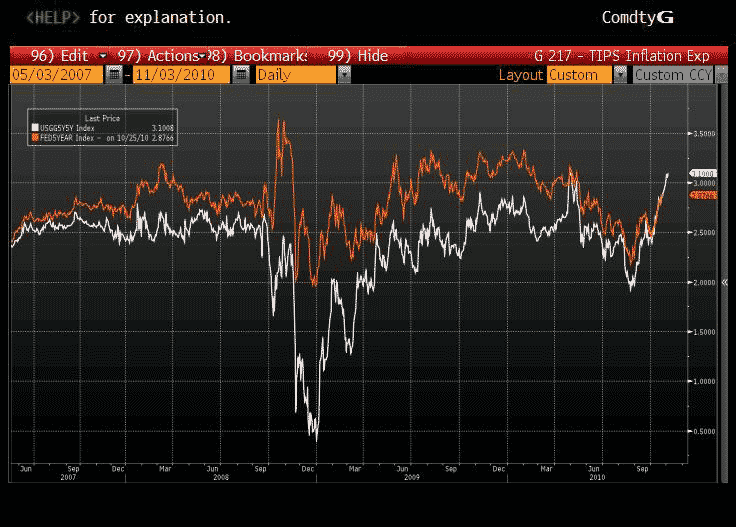

As readers know, we don’t do predictions . We do “non predictions”. So in line with tradition, TMM predict that the Fed will NOT announce more than $700bn and will NOT announce less than $400bn over a six month period (or equivalent). Now this is something of a cop out, but not for good reason. Experience suggests that the Fed will try their damnedest to avoid surprising the market in a bad way, and the recent leaks and furore about the Primary Dealer questionnaire illustrate that they have a pretty good handle on things. That suggests the downside floor is pretty high. On the upside, we are sure that the FOMC will be utterly delighted by the increase in inflation expectations since Jackson Hole, with 5y5y TIPS Breakevens (see chart below, white line) surging 1.17% to 3.09%, essentially equaling the highs back in April. Now this would suggest that the Fed would be cautious in terms of driving breakevens even higher for fear of deanchoring inflation expectations. The truth, as always, is somewhat more nuanced, as the Fed’s own model for deriving inflation expectations from TIPS (attempting to strip out the usual caveats: funding, inflation risk premia and valuation of the deflation floor) has not risen quite as much, by 68bps (see chart below, orange line). Unsurprisingly, a good portion of this is inflation risk premia: QE2 is essentially the last roll of the Dice – there is nothing left after this. A more careful look at the chart shows that while 5y5y Breakevens did not reach March 2009 lows, the Fed’s measure *did*, and was within a whisper of the levels reached in late-2008. Anyway, the point here is that the 5y5y breakeven is more followed by market participants and thus the Fed is left with a difficult balancing act between that, which argues caution, and their own model, which suggests there is more scope. In TMM’s book, that argues that the upside surprise is also capped.

(click to enlarge)

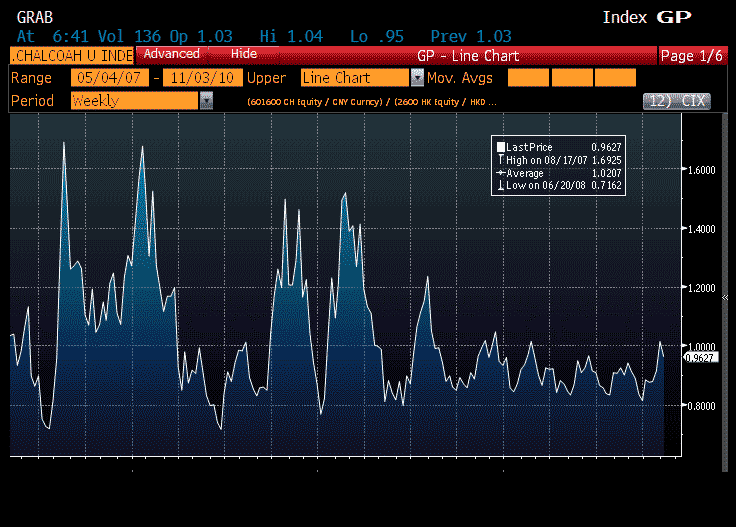

That being said, if you want the upside on the EM bubble and QE look no further than Hong Kong as the team a large US ex-investment bank have pointed out. Hong Kong is an odd market because thanks to the USD peg it is basically a China fundamentals story powered by USD liquidity dynamics. Whereas the Shanghai Composite tends to move in line with mainland fundamentals and liquidity conditions HK tends to be driven by what is going on in the markets more broadly. The best way to demonstrate this is looking at the premium/discount between companies with both a Shanghai and Hong Kong listing. As can be seen here, Chalco, one of our least favorite companies traded at a truly bizarre premium onshore in China in 2007 as liquidity was flush onshore, rates were high in the USD market and there was something of a property investment crackdown underway. That collapsed into mid-08 as aggressive China monetary tightening came through and loosening went on in the US. The difference this time of course is that now liquidity is flush everywhere and if anything China is cracking down on property again and talking about tighter loan quotas. For those not brave enough to play the “limit long HK, damn the torpedoes” game buying the H share premium does look fairly sensible as EM countries including China have to brace for impact from the QE Tsunami.

(click to enlarge)

The other side effect of the QE announcement is to lift the veil on everything else that has been ticking on in the background for the past 3 weeks. European news as been completely shrouded and as the market has been holding its collective breath. Actually the analogy we would prefer is it has been gagging with its hand over its mouth on a bad Irish/Greek prawn waiting for the speeches to be over before it legs it to the toilets and chucks its Euro guts up. Six months ago Irish spreads going to where they are now together with bombs going off in Athens’ Embassies as someone tries to incite revolution may just have seen EUR/CHF FALL. Not Rally. We are are pretty close to reloading EUR/CHF shorts just in case (we also like the soothsayer signals in it). We cant be that far off SNB relief exit levels either. It also ties in with our view on Euro rates.

Ooooooo.. is it Christmas yet? Pleeeaaase can it be. We are just SO excited, can we open it now please? Or just peak inside the paper ???

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply