Once a trend makes it to a major newsweekly, it is usually over. By the time the mainstream media spots a trend, it has already been fully baked into the market and is about to reverse. Historically the newsweekly is Time, although it is hardily the trendsetter it used to be. This week’s issue of The Economist has Currency Wars on the cover. Does this signal the end of the free-fall in the Dollar?

I have been noting that 76 in the Dollar Index is a key level, representing the confluence of two trendlines: the down-sloping trendline of the dramatic fall this past two months, and the up-sloping trendline off the prior two bottoms.

The Dollar Index (DX) fell to 76.14 on Friday, and then bounced to 77.13, a large move. This Sunday evening it has gone above 77.20, then stepped back a bit. When the machines come on in Europe, we may find out where the Dollar is really headed, but this sort of V-shaped bounce is what we should expect at the bottom after such a sharp fall.

If the Dollar does bottom, it could be expected to run up towards DX100 by 2012, a strong move that would reflect expectations of deflation coming from debt destruction. Possibly the foreclosuregate scandal will lead to mortgage write-downs that spawn the debt-deflation spiral we have so far avoided. Consensus expectations remain that the Fed can prevent deflation, especially with the injection of QE. In the short run, expectations of QE may be so baked in that any slippage of resolve may by itself reverse the Buck. In the longer run, however, it cannot be presumed that QE will prevent deflation. Massive injections of liquidity since 2000 have failed to reflate, as measured by CPI or the GDP deflator. Velocity of money continues to decline.

The argument that the Fed cannot prevent deflation is one of Prechter’s core assertions going back over 10 years. I first blogged about it in 2003. You can read his argument in this excerpt from his book, Conquer the Crash. He has been way ahead of the curve on this issue. His short term update service (STU) has been focusing more on the Dollar lately than stocks, with this observation Friday:

The U.S. Dollar rally appears to be starting. The stock rally is overbought and overbelieved. The conditions are in place that makes a stock market decline a high probability.

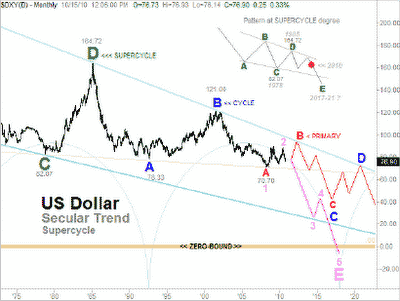

In the larger picture, however, the Dollar may still be doomed, which means it has farther to fall in the Dollar Index. Joe Russo provides a Big Picture view of the Dollar, using the next chart as a backdrop to several scenarios going forward.

The chart shows the bottom (listed as green C) at the end of the Carter years, followed by the Volcker Rally into 1985 (green D), when the Plaza Accord coordinated a rapid 50% drop in the Dollar. Under Robert Rubin during the Clinton years (blue A), the Dollar strengthened until the dot-com bubble top (blue B). Since then the massive injection of liquidity by Greenspan and Bernanke has driven the Dollar down to historically low levels (red A).

Russo views this falling wedge pattern as “no better pattern from which our financial masters of illusion could better engineer the most orderly and flexible destruction of currency.” He proposes three scenarios:

- bounce off 76, continuing a cyclical bull into 2012 (red B in the chart)

- continued slide to 70.70, testing the recent low (red A), before the rally

- “total destruction” of the Dollar by 2017 if we break 70.70

Whew! We found a technician more bearish than Prechter! I think what Russo is overlooking is that the US is not acting in a vacuum, and has much less leverage now then it had in 1986 (Plaza Accord) or 1971 (going off gold), let alone after the wreckage of WWII (Bretton Woods). Already economic indications are showing an effect of the possibility of QE2 driving the rapid drop in the Dollar: the Eurozone is slowing, and Japan is on the verge of recession. The developed countries therefore have an incentive to stop the Dollar slide. In effect, the US needs to coordinate debasing the buck along with the Euro, the Pound and the Yen; by debasing them together the emerging market currencies (particularly the Chinese) will be forced to rise.

We shall see how this plays out in fairly short order, as G20 is soon to meet. My bet is the Dollar rises into those meetings and continues up into the next election.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply