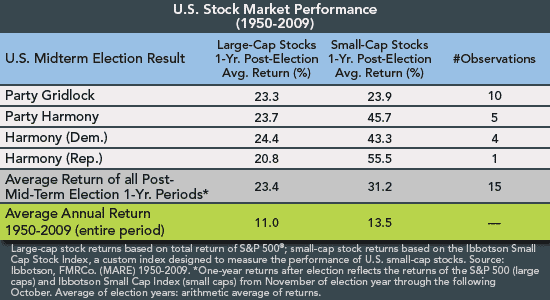

There is a high expectation that the Repubs take at least one house of Congress, blocking any further expansion of the Obama agenda, and leading to gridlock for the next two years. There is a general view that gridlock is good for stocks, so a post today that looked at the data caught my eye. PragCap reported on a Fidelity analysis that shows NO positive correlation between mid-term gridlock and stocks:

Large-cap stock returns during post-midterm election years have been about the same, whether or not the outcome resulted in gridlock or harmony (i.e. one party controls both houses of Congress and the White House). Small-cap stocks, meanwhile, outperformed in years of political harmony compared to gridlock.

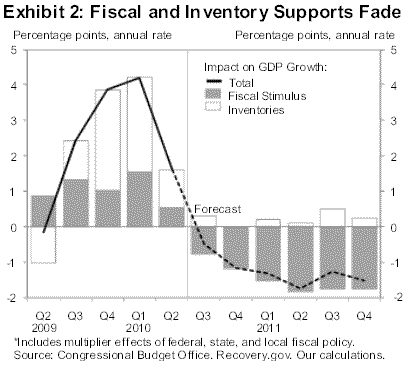

PragCap goes on to comment that gridlock may be bad for the economy in the circumstances we are in. The next chart shows how the stimulus at least buoyed GDP during the past 18 months, and (as I have commented) once past Peak Stimulus the shrinking stimulus is actually a drag on GDP growth that makes a coming double-dip more likely (the black line is the drag from less stimulus plus less inventory rebuilding):

There is hope that the private sector can more than overcome the drag, and expectations have been that the Q3 GDP report (which is released right before the mid-term elections) would be at least flat to Q2.

In August, however, the trade deficit widened, and it acts as an additional drag on GDP growth: the change in exports less imports is a major component of GDP growth, and a wider trade deficit means it could come in more negative relative to the prior quarter. There had been an import surge in Q2 which was largely based on slightly higher oil prices plus restocking for holiday sales, so expectations were for this component to decrease between Q2 and Q3, which would have pushed Q3 GDP growth up on this component.

Now, the NYT reports that Macroeconomic Advisors has reduced Q3 GDP expectations to 1.2%, a decline from Q2’s 1.6%. Calculated Risk had expected a 2% Q3, but calculates that the trade deficit will end up about the same as Q2, meaning it will not improve GDP growth, and now estimates 1.5% GDP in Q3.

Ironically, a poor GDP report boosts the odds of QE2, which should boost stocks until they run up enough to account for the purported benefits of QE. If gridlock results in less fiscal stimulus and less effort to fix serious structural problems (unemployment, exports, bank lending), the normal rise in stocks between the mid-terms and the next election may be less than expected.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply