I am often asked, especially by my Peking University students, to list what I think is the sequence of steps China will take to address its economic imbalances. Remember that rebalancing, in the Chinese context, has a very specific definition. It means raising the consumption share of GDP. This is just a way of saying that consumption growth must outpace GDP growth, and over the next few years it inevitably will, if the rest of the world is unable to absorb a rising Chinese trade surplus.

But there are many ways this can happen. The good way is by a surge in consumption growth that allows GDP growth to remain strong. The bad way is for consumption growth to slow, and for GDP growth to slow much more rapidly.

So how will China rebalance? Unfortunately there is no obvious answer. I always tell my students that even if I were smart enough to know the optimal sequence, it would nonetheless be very difficult to make any reasonable prediction since the sequence is not likely to be subject to economic analysis. This is as much or more a political issue as it is economic, for at least two reasons:

- The rebalancing process will cause short-term pain and perhaps a rise in unemployment. Postponing it will make both of those problems worse when the adjustment finally takes place. China has to choose when is the best time to begin that process, and this depends on a lot of social and political factors. Most obviously, the 2012 succession process is a key variable.

- Because rebalancing mainly means increasing the household income share of national income and, with it, the household consumption share, it implicitly means redistributing income from businesses and governments to households, and exactly which businesses, governments, and households depend on which adjustment mechanism. There are several ways to rebalance, each with different implications for social policy, making it an issue that must be determined not by economists but by political leaders.

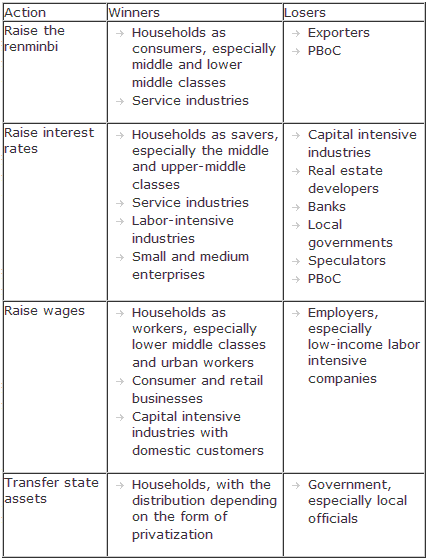

I want especially to address this second point. In previous pieces I have discussed four main ways of boosting the household income share of national income. Over the rest of this entry I will try to set out the very different sets of winners and losers under each policy, and suggest how different policies and sets of policies might change the underlying economy.

China can raise the value of the renminbi. An undervalued currency affects the domestic and trade imbalances by shifting income from households (who are net importers) to net exporters. This automatically increases the gap between what is domestically produced and what is domestically consumed, and so expands the trade surplus. By increasing savings (savings is equal to production minus consumption), an undervalued exchange rate increases the excess of savings over investment, which is by definition equal to the current account surplus.

By revaluing the currency, Beijing reverses this transfer and helps rebalance the economy. So who benefits?

Clearly households in the aggregate, as consumers, benefit because the reduction in import prices implies a real increase in their income. The greater the import component as a share of income, the greater the real increase in income. My guess is that middle and lower middle classes benefit most since the very poor (especially the rural poor) are likely to have a relatively low import component in their consumption, and the rich consume a very low share of their total income.

A second group of winners includes companies that sell imported goods (for example large retailers) and companies that otherwise benefit from an increase in domestic consumption but who don’t have an important export market. This includes most importantly the labor-intensive service industries.

The losers are, first and most obviously, the export sector, who will see a rise in their costs relative to their revenues, and second, if these rising costs lead to bankruptcies, households to the extent that they are employees of the export companies. Part of the rise in unemployment in the export sector will be mitigated as new workers will in fact be employed by the winning industries, but a rapid rise in the currency could cause unemployment in the export sector to rise faster than employment in the other sectors, and so any change in household income could itself be constrained or even negative.

This, of course, is the big problem China faces. By now nearly everyone recognizes that raising the value of the renminbi is a necessary part of the process of raising the real value of household income and improving the balance between producers and consumers, but if the currency rises too quickly and so leads to rising unemployment, it will actually cause household income (and with it household consumption) to decline as unemployment rises. The imbalance will still improve, but it will improve in the “wrong” way, in the form of production declining faster than consumption.

Finally any entity that is long dollars and short renminbi will lose. The most obvious example is the PBoC, which loses greatly from revaluation. Investors who have stockpiled significant amounts of commodities funded by renminbi borrowing will also lose.

China can raise interest rates. Artificially low interest rates are, in my opinion, the single biggest cause of the imbalance in China. Very low interest rates shift income from net savers (mainly the household sector) to net borrowers (manufacturers, local, provincial and central governments, real estate developers, infrastructure investors). As with an undervalued currency this increases the gap between production and consumption or, put another way, the gap between savings and investment, and so forces up the current account surplus.

If Beijing raises interest rates the winners are clearly households, who are net savers, and the higher their savings rate the more they benefit. The rich save the most, but they have much better ways of saving than in bank deposits, and more importantly they own the assets (such as real estate and real estate developers) that benefit heavily from low borrowing costs, so I suspect that the rich benefit but nearly as much as one might expect. My guess is that the upper middle and middle classes will benefit the most.

Raising interest rates will also benefit retail industries, small and medium enterprises (SMEs) and especially service industries, since higher household income will increase consumption.

The losers are fairly obvious: capital intensive industries that borrow heavily from the banks, local and provincial governments, real estate developers, and infrastructure investors – all the sectors in which we are seeing serious overcapacity and toxic investment. Banks too are big losers because NPLs will almost certainly rise if lending rates do. Finally the PBoC loses because the cost of its funding will rise relative to the return on its assets.

Of course the same caveat applies as above: if interest rates rise too quickly so that bankruptcies and unemployment in the capital intensive sector rise faster than employment in retailers and SMEs, the resulting rebalancing will occur anyway, but in the most painful way possible: household income will rise very slowly or even decline while investment rises more slowly or declines more quickly. The longer Beijing waits to raise interest rates the worse the capital misallocation will become but, paradoxically, the harder it will be to raise them. High debt needs low interest rates to make them manageable,

China can raise wages. The key here is not the absolute wage level but rather the differential between wage growth and productivity growth. If productivity grows faster than wages, as it has especially in the past decade, the share of production that workers keep in the form of wages necessarily declines, and household income as a share of GDP declines with it. Of course consumption then grows more slowly than production and the trade surplus soars.

If wages rise faster than productivity, or at least the gap between the two is narrowed, workers benefit by increasing their share of national income. In the aggregate households benefit and probably most of the benefit accrues to the lower middle and urban working classes. Of course businesses that benefit from increased household spending also benefit, but perhaps not as much if they are heavily labor intensive.

Needless to say employers in the aggregate are the big losers. If too-rapidly rising wages lead to rising unemployment, the rebalancing, once again, takes place under very difficult conditions, with rising wages being more than offset by rising unemployment. Of course in a flexible market rising unemployment should itself put downward pressure on wages, so administrative policies and wage stickiness are important factors here.

China can privatize and distribute ownership of state-owned assets. The quickest way to give a big one-off boost to household income is to transfer ownership of state assets to the household sector. The winners are the household sector, but of course the distribution of the gains depend on how the transfer takes place. If companies are privatized in a very politicized way and the proceeds used, for example, to clean up the banks, the rich will probably benefit most. If the assets are simply transferred to the pension funds, the middle and lower middle class, and urban workers, will benefit the most.

The losers are government entities and individuals that benefitted most from control of the assets. This makes this option politically very difficult.

Winners and losers

To summarize very simply, the table below lists the options:

As the table implies, the discussion about the timing and sequencing of the necessary adjustment policies depends heavily on political considerations and on the relative ability of the expected losers and winners to influence the outcome. That is why I always argue that this is a political discussion more than an economic discussion.

The trick for any of the first three adjustment measures (which are the necessary ones for a sustainable adjustment) is to adjust just fast enough so that the employment created by the rise in household consumption offsets the unemployment created by financial distress among the relevant losers. This is easy to say, of course, but not so easy to do because the negative employment effects are likely to be quicker than the positive employment effects. If any of these adjustments take place too quickly, the net impact on household income (and thus household consumption) can actually be negative in the short term as rising unemployment reduces household income faster than the adjustment increases it.

Notice also that Beijing can address more than one of the target policies above and can even move them in opposite directions. This means that there are many ways of rebalancing (or even of avoiding rebalancing) and these will have very different sets of winners and losers.

For example China is raising wages dramatically, right? Maybe. I am a little skeptical that they can pull it off to nearly the extent that people seem to think, but I would guess Beijing can indeed raise wages dramatically only if they counteract the negative employment effect by lowering the cost of capital. Otherwise unemployment could rise much faster than Beijing can tolerate.

This will mean, however, that Chinese growth would become even more capital intensive than ever. In that case money will effectively be transferred from employers in the aggregate, especially labor-intensive employers, to capital-intensive industries. It will also almost certainly increase speculative activity.

Alternatively China can raise the value of the renminbi, perhaps because of US pressure, and then counterbalance it the way they did during the 2005-08 appreciation and the way Japan did it during post-Plaza appreciation – by lowering real interest rates and expanding credit. In fact one of the reasons I have disagreed with most economists about the likelihood of an interest rate hike in China this year is precisely because I expected increased pressure on the renminbi. By the way last week Bloomberg had a story on just this topic:

China’s five-year interest-rate swap fell the most in more than a month on speculation the central bank will hold off from increasing interest rates as it allows quicker yuan appreciation.

…“As the yuan’s appreciation pace picks up, it’s less necessary to raise interest rates because currency gains are also a tightening measure,” said Hu Hangyu, a Beijing-based bond analyst at Citic Securities Co., China’s largest listed brokerage. “The central bank won’t raise interest rates this year.”

At any rate what might happen in the case that China raises the value of the renminbi and then, to counter the impact, reduces real interest rates? As the box above shows, depending on the relative magnitude of the two opposite policies, it is very easy for the imbalances actually to get worse – i.e. lowering interest rates confiscates household income faster than raising the renminbi returns it – and for the trade surplus to rise.

This combination of policies will also almost certainly increase speculative activity, capital intensivity, and capital misallocation. That is frankly my biggest worry about excessive US focus on the currency. If the US does get China to revalue the renminbi dramatically, and China responds with a sharp cut in real interest rates and/or an increase in loan-driven investment, not only will the domestic imbalances get worse, China’s trade surplus and the US trade deficit could easily rise, and household consumption drop, while China’s capital misallocation will be significantly aggravated. China, in that case, would be following Japan’s late 1980s footsteps very closely, with all the dire consequences that this implies.

The key point is that there are many ways that the necessary adjustment can take place, and each of these has a different distributive impact. The other important point is that any Chinese adjustment must be slow because in the short term the negative consequences for employment can overwhelm the positive consequences.

Unfortunately the pace of China’s adjustment will in large part depend on the pace of the external adjustment – China needs trade surpluses to absorb excess capacity, but its trade surplus depends on the ability and willingness mainly of the US and trade-deficit Europe to absorb those surpluses. Because China has resisted adjusting for so long, I worry that the rest of the world is neither able (especially in the case of trade-deficit Europe) nor willing to wait long enough to allow China a relatively easy adjustment.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply