Yesterday morning I attended a fascinating session in Palo Alto that points to the future of venture capital in Silicon Valley. Provocatively framed as a “smackdown” between traditional VCs and a new class of Super Angels, it instead highlighted the future rebirth of innovation in Silicon Valley.

Yesterday morning I attended a fascinating session in Palo Alto that points to the future of venture capital in Silicon Valley. Provocatively framed as a “smackdown” between traditional VCs and a new class of Super Angels, it instead highlighted the future rebirth of innovation in Silicon Valley.

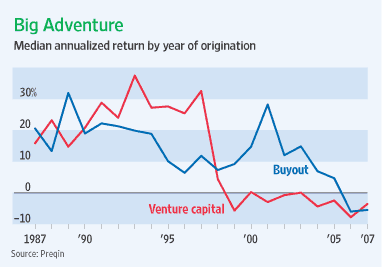

Venture Capital has been in its own Lost Decade with negative returns since 2000 after three glorious decades during the Era of Moore’s Law. Moore’s Law continues, but innovation has moved higher in the technical stack at the same time as the Politics of Envy have greatly plucked the Golden Goose of American innovation. This last decade brought us horrific laws like Sarbanes-Oxley, which raised the cost of IPOs, and tragic policies such as the demonization of stock options which have been pecking the growth engine to death.

Silicon Valley, however, finds ways around blockages.

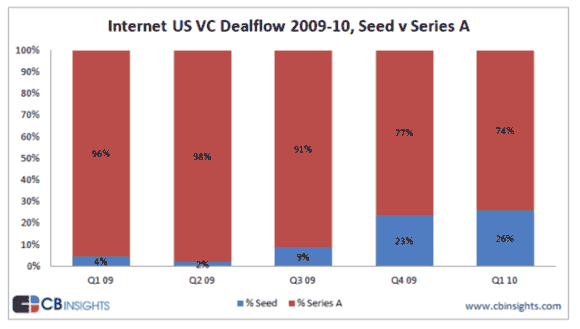

We have now entered the Era of Cheap, where great companies can be launched on the cheap. The first wave of Consumer Internet franchises are racing towards big IPOs: Facebook, Zynga, Twitter, Chegg, Groupon. These ventures were started with capital from a new breed of investor, the so-called SuperAngels – institutionalized seed funds that embrace the Era of Cheap. As this chart from CBInsights shows, in the past year the SuperAngel seed funds have grabbed over 25% share of new fundings from the traditional VCs.

What the smackdown series of debates (which you can find on VideoCrunch) show is how the Era of Cheap is disrupting the venture business itself. After funding disruption to traditional industries for thirty years, the big VC funds are finally getting a taste of their own medicine. How they will respond is unclear. There is a lot of chatter that the traditional VC model is broken. Certainly with the poor returns for the past decade, the pension funds which invest in the venture category are pulling out.

But is the model itself at fault, or the exogenous factors that have plagued all financial sectors in the past decade? I argue that the New Normal of low returns for an extended period affects venture capital as well. I conclude that even granted the effect of exogenous factors, the VC industry should stop expecting it to go back to the old normal right away. Instead, venture capital needs to figure out how to deliver returns in its new nromal: an environment with few IPOs and smaller m&a exits. They need a new model.

The SuperAngels have been the first to figure this out. The Era of Cheap lets them fund Internet deals which can be quickly tested on small capital. They may exit with a quick flip, or raise boatloads of VC capital and go for the big win; but the modest capital allows them the time to experiment and find a market before big money removes the quick exit.

The final smackdown event went back and forth on this issue. The Big VC argument is that you need the big money to build a real company. The SuperAngel counter is that for both founders and buyers the small exit might be a better outcome, and they can preserve the big win if the company hits in the consumer Internet lottery of consumer appeal and fickleness.

My take: in the old model, after the seed round, traditional VC was a necessity, In the new seed model, Big VC is but an option.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply