I recently came across a very interesting essay written by Paul McCulley (of PIMCO) in 2001. At one point he discusses a bizarre idea that got a foothold at the Fed in 1989:

For the last decade, the Fed has played something called “opportunistic disinflation,” and it, too, has worked.

The term actually entered the public arena on July 10, 1996, when the Wall Street Journal leaked an internal Fed report by staff economists Orphandies and Wilcox, detailing the Fed’s “new” approach to inflation-fighting: the Fed should not take deliberate action to reduce inflation, but rather “wait for external circumstances – e.g., favorable supply shocks and unforeseen recessions – to deliver the desired additional reduction in inflation.”

Simply put, the theory said, the Fed should not deliberately induce recessions to reduce inflation, but rather “opportunistically” welcome recessions when they inevitably happen, bringing cyclical disinflationary dividends. A corollary of this thesis was that the Fed should pre-emptively tighten in recoveries, on leading indicators of rising inflation, rather than rising inflation itself, so as to “lock-in” the cyclical disinflationary gains wrought by recession. While the label “opportunistic disinflation” was a clever one, the Fed had actually been practicing the policy for a long time. Indeed, former Philadelphia Fed President Edward Boehne elegantly described the approach at a FOMC meeting in late 1989:

“Now, sooner or later, we will have a recession. I don’t think anybody around the table wants a recession or is seeking one, but sooner or later we will have one. If in that recession we took advantage of the anti-inflation (impetus) and we got inflation down from 41/2 percent to 3 percent, and then in the next expansion we were able to keep inflation from accelerating, sooner or later there will be another recession out there. And so, if we could bring inflation down from cycle to cycle just as we let it build up from cycle to cycle, that would be considerable progress over what we’ve done in other periods in history.”

Before discussing the Boehne quotation, think for a moment about just how strange this “opportunistic disinflation” idea really is. Suppose you are trying to lose weight. You notice that extremely ill people often lose weight. Voila! A cancer diagnosis is a perfect “opportunity” to lose some weight. Of course you don’t want to go on a diet when suffering from cancer, (that would be going too far), but on the other hand don’t go out of your way to eat food either. Just enjoy the weight loss.

There are basically two types of macroeconomists in academia. Those (mostly right-wing) who favor a strict inflation target. In that case inflation would be the same whether we are in a recession or boom. Others favor some sort of flexible inflation target. NGDP targeting is a good example. When real growth falls, you allow inflation to rise a bit. This reduces the severity of the business cycle during supply shocks.

But within the halls of the Fed a third and very dangerous idea took hold during the 1980s and 1990s, opportunistic disinflation. This ideas suggests that the fall in inflation rates often observed in recessions is not a failure of demand management, not a highly procyclical monetary policy, but something to be welcomed.

Now at this point I know my more sensible readers are starting to roll their eyes. “Yes, a few oddballs at the Fed put forth this theory, but you don’t mean to seriously suggest that such a wacky idea, with almost no support in academia, would be embraced by the Fed itself?”

Go back and read the Boehne quotation. As of 1989, inflation had average about 4.5% over the previous 7 years. The bond markets clearly indicated that inflation was likely to stay high, indeed go even higher. But Boehne had inside information, he worked at the Fed and understood that in the next recession the Fed was determined to reduce inflation to 3% and keep it there until the following recession. And in the following recession they would reduce it a bit further, and so on. And that is what happened. Inflation fell to 3% percent in the 1990s. The next cycle didn’t see much further reduction, but only because of the huge 2006-08 oil shock. If not for Asian oil demand, the Fed would have delivered a further reduction in inflation. Now that oil prices are down, we have inflation falling to about 1% in this cycle.

Boehne was very accurately predicting a Fed policy that would almost inevitably drive the economy off the cliff, only he didn’t realize it. Opportunistic disinflation means that inflation falls at the same time that RGDP is falling. If you start from a position of already minimal inflation, and have a steep recession, and the Fed does nothing to offset the fall in inflation typically associated with steep recessions, then you can get a fall in NGDP. As I keep pointing out, NGDP in 2009 fell at the sharpest rate since 1938. And both 1938 and 2009 saw near-zero interest rates. Boehne did not recognize that this sort of policy could drive the economy into a liquidity trap. But he can be forgiven for that oversight, after all, with Treasury-bill rates up around 8% in 1989, few people even considered the possibility of 1930s-style liquidity traps returning.

Bernanke and Greenspan saw what happened in Japan in the 1990s, however, and that ’s why the Fed seemed to ease aggressively in 2002. In fact, monetary policy was not very expansionary, but at least they understood the problem. Unfortunately, they didn’t recognize just how dangerous the Fed’s opportunistic disinflation policy had become.

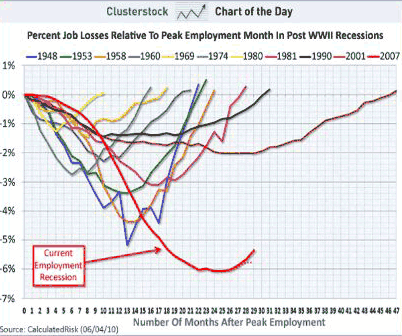

The following graph shows that the jobless recovery of 2010 is nothing new, the previous two cycles had the same problem, it’s just that they were much milder, so fewer people noticed.

I found this graph in Erik Brynjolfsson’s blog, which also contained this provocative post:

As growth resumes, millions of people will find that their old jobs are gone forever. The jobless recovery is one symptom.

Two points. There are no jobless recoveries. If you don’t generate jobs, you have no recovery—regardless of whether RGDP is growing. And second, people normally don’t get their old jobs back, in this recession or in any other recession. How many people return to their old jobs after being laid off? I read somewhere that during a typical year there are about 32 million jobs lost and about 33 million jobs created. I’d wager that very few of those jobs created are people getting their old jobs back.

The post was entitled “The Great Recalculation.” But if the Fed is doing its job then recalculation should produce stagflation. Lower output should mean higher inflation. But that’s not what we are seeing. It is possible that there is an unusually large amount of recalculation going on, although in my view that mostly occurred before the severe phase of the recession began in August 2008, but in any case it is observationally indistinguishable from opportunistic disinflation.

I recall reading about opportunistic disinflation in the 1990s, and making a mental note that it was a silly idea, obviously procyclical, and that surely the Fed would not take the idea seriously. Shame on me. The Fed warned us what they planned to do as far back as 1989. We ignored them. Then they went ahead and did it. And they are still doing it. This expansion will have even lower inflation that the last one.

PS. Paul Krugman deserves some credit for anticipating this problem.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply