Friedman and Schwartz showed that if the Fed remained passive in the face of rising demand for base money, then they were effectively tightening money policy. This was essentially my argument about the fall of 2008. During the late 2008 banking crisis the Fed remained too passive in the face of a huge increase in the demand for liquidity. Thus caused deflationary expectations to set in, which caused crashes in all sorts of asset markets, and the falling asset prices greatly intensified the financial crisis.

The conventional view reverses the causation. The US financial crisis is viewed as an exogenous real shock, which actually caused the big drop in NGDP.

Let me say right up front that I don’t expect a double dip recession, nor do I believe the markets expect this to occur. On the other hand I also think it is clear that the risk of a double dip recession has recently risen, let’s say from 5% to 20%. (Yes, I’m pulling these numbers out of a hat, just to give you a sense of what I think the markets are telling us.)

Suppose I am right, and that an increase in the demand for dollars, plus Fed passivity, recently made monetary policy effectively more contractionary. Here’s what you’d expect to see in the financial markets:

- Falling commodity prices

- Falling TIPS spreads

- Falling equity prices

- An appreciating dollar

Here’s what I have recently noticed (from Yahoo.com):

Oil prices rose to near $78 a barrel Friday, halting an 11 percent sell-off this week as the euro recovered against the dollar and world stock markets steadied.

So oil has fallen sharply this week. I wasn’t able to find a graph of TIPS spreads, but this Yahoo table shows that 5 year bond yields have recently fallen 55 basis points, and I believe that 5 year TIPS yields have been much more stable. Thus implied inflation forecasts have recently fallen from well above 2% to well below 2%.

US Treasury Bonds Rates

| Maturity | Yield | Yesterday | Last Week | Last Month |

| 3 Month | 0.08 | 0.13 | 0.14 | 0.14 |

| 6 Month | 0.15 | 0.20 | 0.22 | 0.24 |

| 2 Year | 0.77 | 0.86 | 1.00 | 1.13 |

| 3 Year | 1.27 | 1.39 | 1.54 | 1.70 |

| 5 Year | 2.15 | 2.29 | 2.45 | 2.70 |

| 10 Year | 3.40 | 3.54 | 3.73 | 3.95 |

| 30 Year | 4.20 | 4.39 | 4.59 | 4.83 |

……….

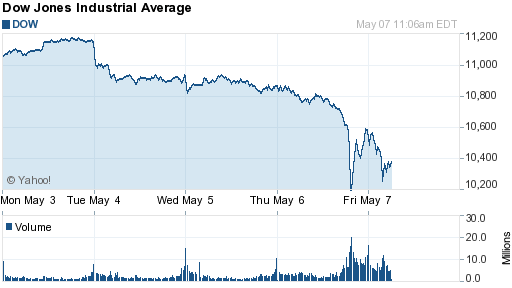

I don’t think I even need to tell you what has been going on with the stock market:

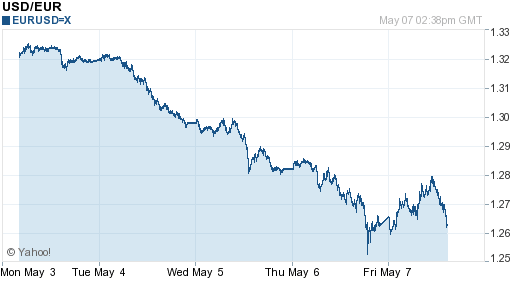

Of course there has been a lot of focus on the sharp downward spike at 2:45 yesterday afternoon. Apparently there was some sort of glitch in electronic trading. Although I know next to nothing about this issue, let me throw out a hypothesis as to a possible contributing factor. Notice that even before the glitch, the market was falling at an accelerating rate. Perhaps the impact of the error was bigger than normal because it occurred in a very sensitive period (from the perspective of technical analysts.) And why might the market have been falling sharply even before the glitch? Take a look at this graph of the euro/dollar exchange rate:

This graph uses GMT, which is 5 hours ahead if I am not mistaken. If any of you are better investigators than I am, perhaps you could check to see whether the sharp plunge in the euro (to below 1.26) occurred around 6-7:30 GMT (or 1-2:30 pm EST.) Just eyeballing the graph it does seem to have occurred at about that time. Perhaps the plunge in the euro weakened stock prices right before the glitch, leading traders to think (for several minutes) that the sharp plunge in the DOW might be real.

In any case, it is clear that all four variables behaved much as you’d expect if the Fed adopted a tighter monetary policy. Of course the real reason was Fed passivity, but the effect was the same. All of these things also happened (to a far greater extent) in October 2008. If the market reaction doesn’t get any worse, we almost certainly won’t get a double-dip. But the market has pretty clearly signaled that its consensus forecast of NGDP growth over the next few years is a bit lower than the implicit forecast from a month ago. And that’s not good news.

A few months back the blogger Ambrosini asked why I don’t give up my push for easier money. The damage has already been done. He didn’t say this, but the implication was that I risk looking like a crude inflationist. I have some sympathy for that argument. But here’s something to think about. Rates are still near zero. That means the Fed still cannot use conventional tools to offset any renewed weakness in the economy, coming from something like a crisis in Europe. Yes, they could and should use unconventional tools, but they have already proved unwilling to use higher price level or NGDP targets back when the need was even greater than today. I really can’t feel comfortable about our situation until the economy is strong enough to push rates above zero. And we are not there yet. Sure the Fed could artificially raise rates above zero right now, but that would be madness given that near term NGDP growth is already likely to be far below target. Indeed 2 year TIPS spreads are still far below 2%.

Here’s something else to think about. The people who think my “nominal shock” model of the 2008 crisis is naive, tend to view financial crisis as a real shock. Banking turmoil makes it difficult to get loans, and hurts business and residential investment. OK, but then explain the last few weeks. The problem is now Greece; the US banking system is just as able to dole out credit as it was a few weeks ago. So why are the markets signaling lower inflation and lower real growth than a few weeks ago? In other words, why has AD dropped slightly? The answer is that monetary policy has effectively tightened due to an increase in demand for dollars.

As I keep emphasizing, tight money always looks like something else. Back in 2008 I can certainly understand why people would focus on the highly visible financial crisis, and not the much more invisible impact of rising money demand (or falling velocity.) But does anyone really believe that the real effects of a debt crisis in tiny Greece (or even Spain) could have produced the sort of large swings we have recently seen in equities, TIPS spreads, oil prices, etc? The last few weeks have been like a miniature version of the October 2008 crisis, but without the US banking panic. And the effects were qualitatively similar.

PS. I am not arguing that the euro and Dow are always positively correlated. When the Dow rises for supply-side reasons (as during the 1999-2000 tech bubble) the euro may well weaken. The correlation occurs when monetary conditions are driving the market.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

The year’s not over yet!

BB