Paul Krugman recently claimed we should not be concerned about whether China will continue to finance U.S. budget deficits since they are being funded by U.S. private savings:

The US private sector has gone from being a huge net borrower to being a net lender; meanwhile, government borrowing has surged, but not enough to offset the private plunge. As a nation, our dependence on foreign loans is way down; the surging deficit is, in effect, being domestically financed.

When I read this claim back in March my reaction was that it makes sense but I also wondered if it were supported by the data. The evidence Krugman showed at the time was that private sector borrowing had declined and was being offset by increased public sector borrowing. While this evidence was consistent with his view, it did not directly show the actual saving rate from each sector or the national saving rate. Consequently, I had some lingering doubts as to whether the U.S. budget deficit was being entirely financed by increased U.S. private savings.

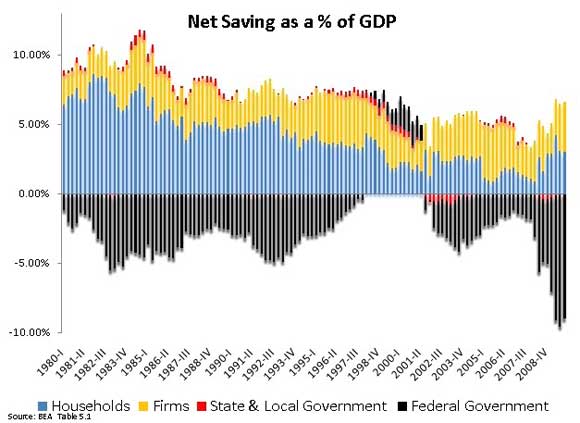

Yesterday I had the chance to reexamine this question while I was putting together some graphs on U.S. saving rates for my class. Below is one of the graphs I created. It shows the net saving rates for the private sector (households and firms) and the public sector (state and local government and federal government) and is based off of data from the BEA’s National Income and Product Account Table 5.1.

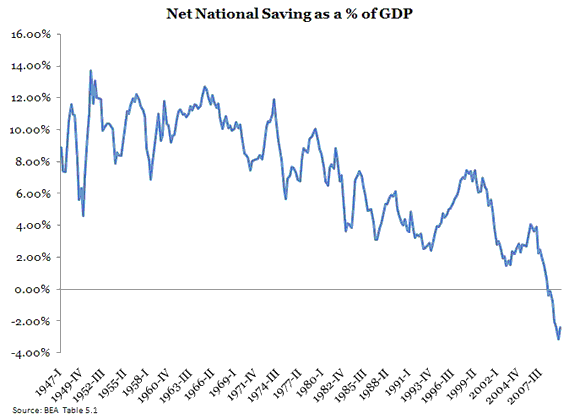

Consistent with Krugman’s claims, the figure does show that the private sector saving rate has increased with most of the gains coming from households. However, the figure also indicates the public sector dissaving is far larger than the saving gains in the private sector. If we sum up the sectors we get the net national saving rate which is graphed below over a longer period:

Here we see the net U.S. net saving rate is negative in 2009 with an average rate of about -2.5%. This net saving shortfall amounts to about $356 billion dollars that had to be financed by foreigners last year. Now to be fair to Krugman, the figures above show U.S. net savings which is equal to U.S. gross savings minus savings allocated to maintaining the existing U.S. capital stock. If one looks at U.S. gross savings in 2009 it is positive. This means the actual budget deficit was financed domestically. Note, however, that the $356 billion dollar shortfall in net savings means the U.S. economy is currently not saving enough to replace its existing capital stock let alone create new capital. That last time that happened was in early 1930s. Luckily for us, though, foreigners are still willing to invest in the United States and make up the difference. So while Krugman is correct that the concerns about China threatening not to finance our budget deficit are misplaced, it also true that the U.S. economy is now more than ever dependent on China to maintain and grow its capital stock.

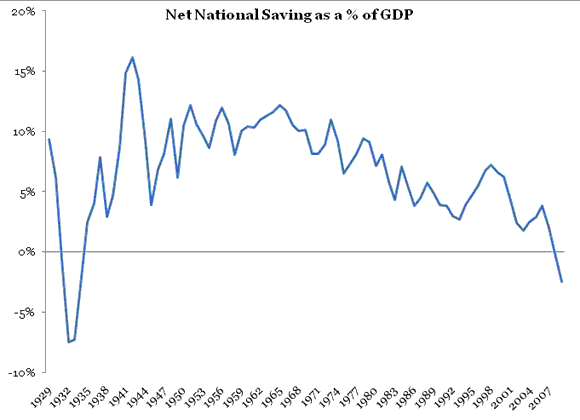

P.S. Here is the net saving rate per year going back to 1929. The source, again, is Table 5.1 from the BEA:

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply