Can or should the federal government balance its budget?

Nowadays the only thing on everybody’s mind is the level of government deficit and national debt. Deficit hysteria is being fueled by reports that the US budget deficit will reach “an all time high” this year. President Obama is going to appoint his own commission to study how to reduce the deficit—since Congress failed in its attempt to establish one. He frets that we will leave crippling mountains of debts for our grandkids. The deficit hysteria hydra is too big to cover in one blog—but here we will address the “deficit cycle” and the possibility of ending it.

There seems to be a deficit mania cycle with hysteria arriving after every recession (because, as we show below, recessions always generate big deficits), only to recede when economic growth resumes and deficits fall. And the fact that there is a Democratic president in office and a largely Democratic congress frees the hands of conservative deficit hawks who complain about spending profligacy and growing national debt (they usually fail to recall that much of this spending and especially tax cuts have been generated under a Republic president and Congress, not to mention the 780 billion Paulson bailout of Wall Street). This deficit hysteria is also a useful tool for distracting people’s attention from really important matters, such as a 10% unemployment rate, the possibility of a double-dip recession, underwater home owners, and rising mortgage delinquencies.

Can the government really balance its budget and run continuous surpluses for a number of years as some politicians promise to do? Here is some data to help you decide that for yourself. Every time the government has tried to balance its budget, the economy has fallen into a recession which has caused the automatic stabilizers to kick in and grow the budget deficit. The graph below depicts the federal budget deficit (or surplus) as a % of GDP with signs reversed (a surplus is below zero, a budget deficit is shown as above zero) and recessionary periods for the entire post-war period. As can be observed in this graph, every budget surplus over this period has preceded a recession. The remaining recessionary episodes have been preceded by reduction of the deficit to GDP ratios. Further, every recession except the one in 1960 led to a budget deficit; the 1960 recession was followed by a reduction of the budget surplus.

These movements of the budget balance are due to automatic stabilizers. When the economy slides into a recession, tax revenues start falling as economic activity declines. Social transfer payments, particularly unemployment benefits, on the other hand, increase, again automatically, as more people loose their jobs. On the other hand when the economy begins to grow, tax revenues grow quickly, moving the budget toward balance or even to a surplus.

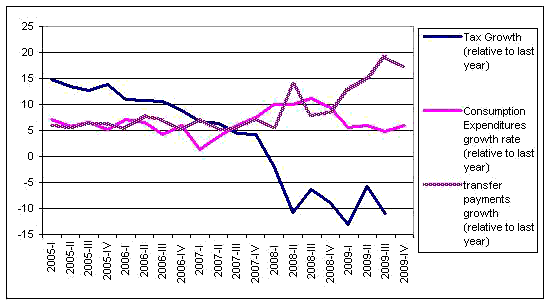

The graph below shows the rate of growth of tax revenues (automatic), government consumption expenditures (somewhat discretionary) and social transfer payments (again automatic) relative to the same quarter of the previous year:

While government consumption expenditures have remained relatively stable after a short spike in 2007-2008, the rate of growth of tax revenues has dropped sharply from 5 % growth to 10 % decline in just three quarters (from Q 4 of 2007 to Q 2 of 2008), reaching another low of -15% in Q1 of 2009. Transfer payments, as expected have been growing at an average rate of 10% since 2007. Decreasing taxes coupled with increased transfer payments have automatically pushed the budget into a larger deficit, notwithstanding the change in consumption expenditures. These automatic stabilizers and not the bailouts or much-belated and smaller-than-needed stimulus are the reason why the economy hasn’t been in a freefall similar to the Great Depression. As the economy slowed down, the budget automatically went into a deficit putting a floor on aggregate demand.

Conclusions: the federal government budget cannot be balanced or turned into surplus without killing the economy and causing another Great Depression, which again, will automatically cause the budget to turn into the negative territory. With the loss of 8 million jobs, and given the private sector’s unwillingness to go further into debt (it is now, finally, spending less than its income) there is no way that the federal budget can be balanced, unless the US becomes a net exporter, which is highly unlikely. So if a politician tells you that she is going to balance that budget, she either doesn’t understand what she is talking about or is trying to fool you to get elected.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply