We are past Peak Stimulus but Q4 GDP should be pretty strong due to the bullwhip effect: a snap-back of inventory rebalancing. The consensus for Q4 has increased quite dramatically, from around 3.5% to 5.5%:

- Bloomberg says 4.6%

- WSJ says 5%

- MarketWatch says 5.5%

- Goldman Sachs says 5.8%

That Keynesian cheerleader Paul Krugman (our next Fed Chair?) warns us to beware the blip: the 2Q02 GDP was first reported as 5.8% amidst rising unemployment – unemployment kept growing until the summer of 2003. That report also came after the 1Q02 numbers were revised downward, just as 3Q09 has been, from 3.8% to 2.2%. As then, the inventory rebalancing number is higher than the underlying consumer expenditure number. Inventory rebalancing is not sustained unless spending emerges – hence the risk of a blip.

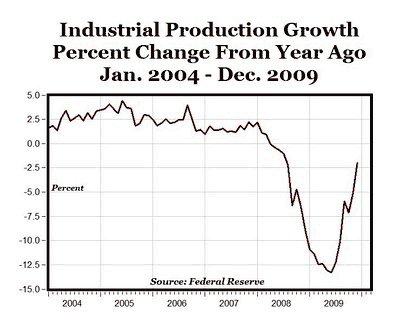

The blip is clear: inventories rose in both Oct and Nov, and are expected to continue in Dec. Accordingly, industrial production has continued to improve. See chart. But an inventory blip is not lasting. Goldman’s report tempered the upgrade in Q4 GDP with a risk of a slow 2H10, even a double dip, as the inventory surge abates.

The blip is clear: inventories rose in both Oct and Nov, and are expected to continue in Dec. Accordingly, industrial production has continued to improve. See chart. But an inventory blip is not lasting. Goldman’s report tempered the upgrade in Q4 GDP with a risk of a slow 2H10, even a double dip, as the inventory surge abates.

The railroads are not confirming growth in shipments, which is a big red flag. For the whole year, RR traffic was at a 20 year low. There is a quarterly pattern to RR traffic where it suffers in Q4 due to stock filling in Q3 for the holiday sales season, but it seems to be slowing in the new year as well. Worse, it is tracking below the disastrous 4Q08 when the economy seemed to be falling off a cliff. No recovery there. (These links have really good charts if you wish to explore this more deeply.)

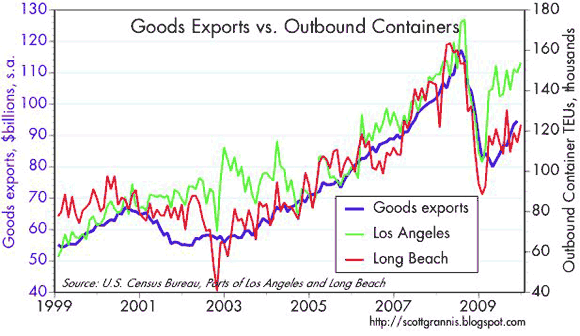

It is not all doom, however. Exports have been rising. This also adds to GDP, like inventory rebalancing, and is more likely to be sustainable since it indicates demand from outside the US is growingCombined with weak or down RR traffic, however, means the increase in exports is not making up for the decrease in domestic spending. Global shipping overall seems to have bottomed and is on a up trend that should last a while. Copper has also rebounded. Copper is a great leading indicator of industrial activity.

Spending is a huge concern. Retail sales in Dec ended up disappointing, although they show a slow improvement when unadjusted. Also, the whole quarter shows improvement, and some of the poor Dec may have been due to a more vigorous Nov and bad weather. Still, a good argument can be made that this slowdown represents a continued spending pulback, not a blip.

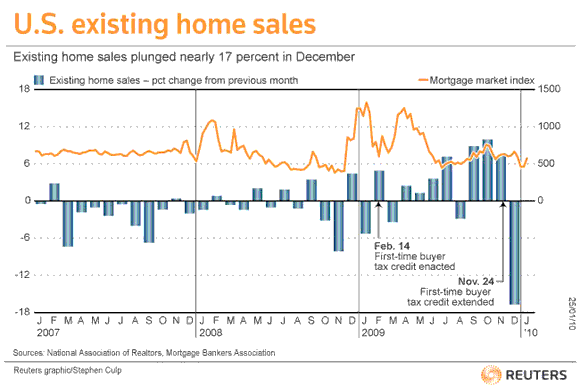

Housing seems poised for a double dip. The end of the housing credit has hammered both new and existing home sales. See second chart. In addition, the next wave of defaults is accelerating, with Alt-A delinquencies rising sharply and Moody’s putting almost $600B on a downgrade watch.

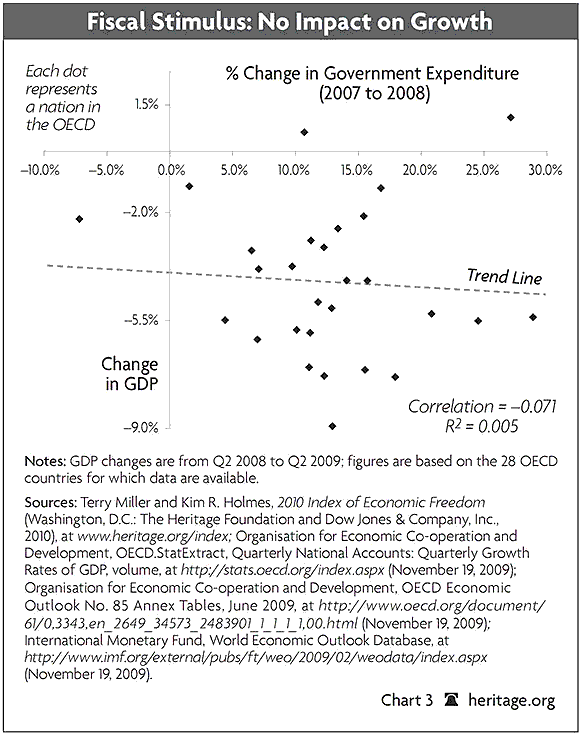

Outside the US we see ominous signs. The UK seems to already be heading into a double dip. I have earlier reported that Japan fell back to 0% growth, and may be the first to go negative. Overall it appears the massive global fiscal stimulus is not showing up in GDP growth. See final chart. That chart shows fiscal increase in 2008 over 2007, and GDP YoY from 2Q08 to 2Q09 declining, not rising as the stimulus hounds would have predicted. Now, the chart is not up to 4Q09, and perhaps the impact of increased fiscal stimulus is more delayed than a one-year lag. There are signs of life globally, so this analysis is not by itself convincing, but it does put a huge damper on the future impact of fiscal stimulus.

The real question after the Q4 numbers is what it means for the next few quarters. As I have said, a W first starts as a V.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply