He has politicized the Fed more than any other Fed chair. He seems easily manipulated by politicians. His fate is entwined in the new-found populism of Obama. His compatriot in populist ire, Tim Terrific, may already be walking dead at Treasury. Yet he may be reconfirmed! Should he?

1. He Was Behind the Bubble in the First Place

Greenspan takes blame for keeping rates too low for too long, and removing all sorts of restrictions on banks. It turns out the biggest cheerleader behind Greenspan was Bernanke, who was part of the FOMC before he became chairman; and when he took over, he continued the very policies which created the credit bubble. He gets credit for pushing liquidity out when needed after Lehman fell; but if he hadn’t, he should have been fired on the spot. The central bank MUST do what Ben did under a fractional-reserve system.

Bernanke knows he blew it on credit. He proffered a defense, arguing implausibly that the Fed had not caused the housing bubble, and claiming that under the Taylor Rule, rates weren’t too low. Economists didn’t buy it. John Taylor, the creator of that Taylor Rule, excoriated Bernanke: Bernanke had NOT followed the Taylor Rule, but had concocted a bastardized version of it.

This does not sound like an independent Fed, but a highly politicized Fed trying to hide its mistakes.

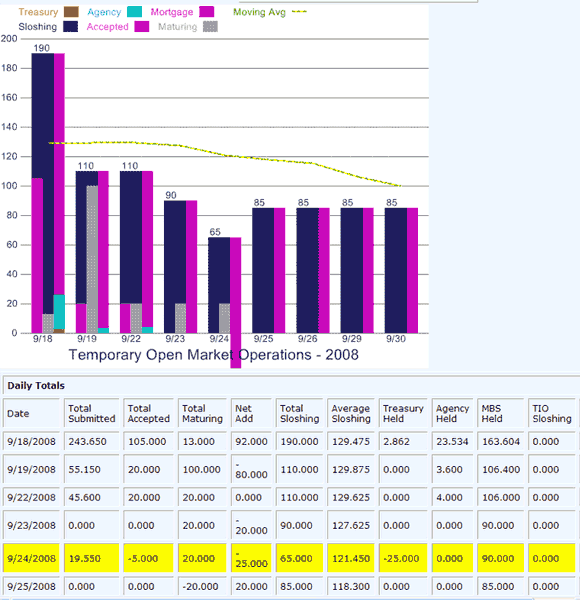

2. He May Have Caused the 2008 Crash

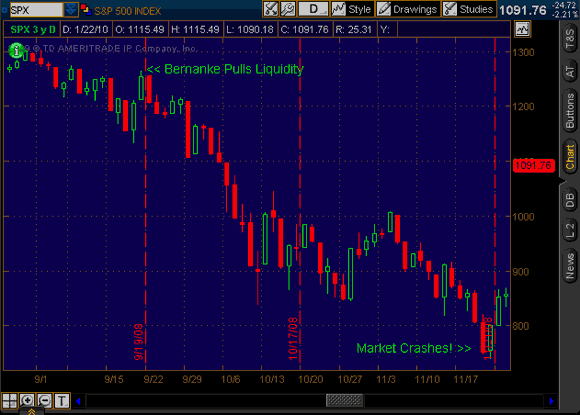

This is pretty shocking, and should immediately doom Bernanke: the Fed withdrew 65% of liquidity from the system in the four days after TARP was first announced to a very tepid reception, the same week McCain suspended his campaign and ran to Washington: Sep19-24, 2008. The facts are written in the record:

The market fell 500 pts in the next 10 days – it crashed! Check out this chart.

Was it intentional? Karl Denninger thinks so. The legal doctrine of res ipsa loquiter (let the thing speak for itself) would concur. This draining of liquidity was precisely designed to panic Congress into passing TARP. Bernanke would use the Jack Bauer defense: it was necessary to torture the victim in order to achieve the result. As things turned out, TARP was not needed. In fact, it was a huge bait & switch: Paulsen turned around and used it for different purposes than he said it was for to Congress. It was not used to stabilize mortgage markets, but to use the AIG bailout as cover for funneling the funds to the over-stretched banks. Was Bernanke in on out, or a dupe?

You decide: is this the type of independent Fed we want?

3. He is Fighting the Wrong War

First Anna Scwhwartz, Milton Friedman’s co-author, and then John Taylor, Stanford economist behind the Taylor Rule for interest rates, criticized Ben as trying to fix the problems in the 1930s, not those of today. Now economist Steve Keen wrote a devastating dissection of Bernanke’s thinking:

Bernanke is popularly portrayed as an expert on the Great Depression—the person whose intimate knowledge of what went wrong in the 1930s saved us from a similar fate in 2009.

In fact, his ignorance of the factors that really caused the Great Depression is a major reason why the Global Financial Crisis occurred in the first place.

Steve tells the story of Irving Fisher, the American Keynes, who is oft used as a foil for this unfortunate quote, in October 1929, right before the Great Crash:

Stock prices have reached what looks like a permanently high plateau.

Irving went on to truly understand what drove the 1931-32 banking crisis and deep depression, and came up with his Debt-Deflation Theory of the Great Depression, still the best analysis. As Steve writes, his analysis

[C]ompletely inverted the economic model on which he had previously relied.His pre-Great Depression model treated finance as just like any other market, with supply and demand setting an equilibrium price. …

[H]e realized that his equilibrium assumption blinded him to the forces that led to the Great Depression. The real action in the economy occurs in disequilibrium.

His debt-deflation theory is summarized in this chain of logic:

- Debt liquidation leads to distress selling and to …

- Contraction of deposit currency, as bank loans are paid off, and to a slowing down of velocity of circulation. This contraction of deposits and of their velocity, precipitated by distress selling, causes …

- A fall in the level of prices, in other words, a swelling of the dollar [we would call that deflation]. Assuming, as above stated, that this fall of prices is not interfered with by reflation or otherwise, there must be …

- A still greater fall in the net worths of business, precipitating bankruptcies and …

- A like fall in profits, which in a “capitalistic,” that is, a private-profit society, leads the concerns which are running at a loss to make …

- A reduction in output, in trade and in employment of labor. These losses, bankruptcies, and unemployment, lead to …

- Pessimism and loss of confidence, which in turn lead to …

- Hoarding and slowing down still more the velocity of circulation. The above eight changes cause …

- Complicated disturbances in the rates of interest, in particular, a fall in the nominal, or money, rates and a rise in the real, or commodity, rates of interest.

This sounds pretty close to what has been happening, again, 80 years later.

Steve points out that Bernanke dismissed Fisher’s theory because he presumed a form of equilibrium:

[D]ebt-deflation represented no more than a redistribution from one group (debtors) to another (creditors).

This argument has been disproven by the very events under Bernanke’s watch as Fed Chair: after a credit bubble, debt does NOT get repaid, it gets written off. Wanna buy some toxic debt? No one does. How about some subprime? This bad debt is being written off or rolled forward, despite Trillions in TARP & Bernanke’s credit facilities. It is not being repaid, except to pick the pockets of the taxpayers and feed it back to Goldman Sachs and their ilk.

Bernanke’s views on the Great Depression are simply wrong, and proven wrong before our eyes. He learned nothing from studying it! His economic prescriptions are colored by his ideology. His economic assumption, of equilibrium, is stuck in 1928. Is this the type of leadership we need right now at the Fed?

Steve’s conclusion:

Bernanke, as the neoclassical economist most responsible for burying Fisher’s accurate explanation of why the Great Depression occurred, is therefore an eminently suitable target for the political sacrifice that America today desperately needs. His extreme actions once the crisis hit have helped reduce the immediate impact of the crisis, but without the ignorance he helped spread about the real cause of the Great Depression, there would not have been a crisis in the first place.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply