Just when it looked like equities had finally shifted to “sell the rally” mode after ten months of “buy the dip”, the SPX goes and rips 14 points to a new post-2008 closing high (cash basis.) While the rally came contrary to Macro Man’s expectations, it was nice to be flat for once and thus avoid that sinking feeling that he experienced all too often last year.

In any event, while stocks closed on their highs last night, risk assets have beaten a bit of a retreat overnight courtesy of developments in China. Despite the PBOC claiming that the recent hike in the RRR wasn’t actually a tightening, the news emerged overnight that the authorities have directed the big 4 banks to halt new lending for the time being. (As Macro Man types this, a PBOC source is on the tape suggesting that banks lent Y1.1 trillion in the first two weeks of January alone. Yowsah!) In an economy where loans and capital are largely directed by administrative diktat rather than prospective return/the price of money, that does in fact represent a tightening of policy.

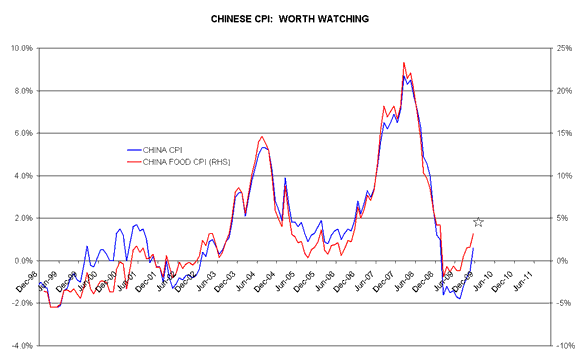

Moreover, the rumor mill in China was cranking at full speed last night. Stories circulated of another hike in the RRR and, more intriguingly, sharp upside surprises to forthcoming CPI and PPI data. While the y/y change in CPI has thus far been muted, the rumored print (marked by the star on the chart below) represents a pretty sharp bump and an uncomfortable trend.

That the authorities are finally starting to adjust policy is the clearest signal of all that they are becoming concerned about the trajectory of inflation. It appears, therefore, that we are entering a new phase in China-watching, where inflation may trump growth as the primary determinant of policy change. Will it be enough to prompt a CNY move? Probably not. But as noted a few days ago, the impact on Chinese equities could be substantial; the Shanghai Comp was slightly down on the year even with 1.1 trillion RMB of lending in the first half of January; how should we expect it to fare with the liquidity taps turned off? “Not well” is the obvious answer, at least judging from the market reaction today.

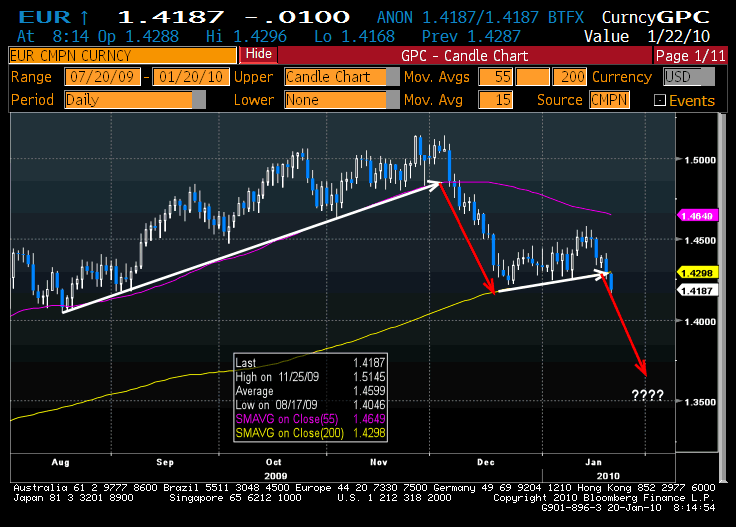

The dollar has performed pretty well overnight, perhaps driven by hints of tightening in the “Chimerica” complex. EUR/USD has broken the 200 day moving average, which could prove significant given the performance of the EUR following the break of the 55 day. As you can see, the latter supported EUR/USD for much of the past six months, and the euro shanked when it finally broke, only finding support at the 200d. Might the break of the 200d herald a similar collapse? Inquiring minds want to know. Certainly the performance of many “risk on” currencies over the past 24 hours does little to suggest that the dollar will slow down any time soon.

(click to enlarge)

Finally, Macro Man had to laugh at Merv the Swerve’s Exeter speech last night. Look up “dovish” in the dictionary and you might find a verbatim transcript. Particularly amusing were his comments that the inflationary episode will prove temporary and that CPI will soon move back towards target.

Macro Man had to shake his head. Courtesy of the VAT-hike base effect come January, it will be almost inconceivable that Merv does not have to write a letter to his Darling to explain why he’s let CPI drift so much above the target. Merv would do well to save the letter onto his hard drive, for he may well be needing it again. The BOE’s own track record of projecting inflation has been dismal to say the least, as a perusal of recent inflation report fan charts will confirm. They used the old forecasters’ trick of moving their near-term projections of inflation in line with the market while leaving their longer-term forecasts unchanged.

How dramatic has this shift been? In May, assuming “just” £125 bio of QE, it was literally inconceivable to the BOE that inflation could rise to more than 2.7%-2.8% by year end; that was the very top of the fan chart. In fact, even with an extra £75 bio of QE, December CPI came in at 2.9%. Ouch!

Not that private-sector forecasters have exactly covered themselves in glory, of course. The cumulative consensus forecasting miss on CPI in 2009 (measured by subtracting the consensus m/m CPI forecast from the actual out-turn, and summing the differences for the 12 months of 2009) was a whopping 1.6%!

It would be an interesting subject for an academic study as to why UK inflation has been so sticky; regardless, it certainly feels as if “Rip-off Britain” rides again. And the stickiness of inflation also raises the question of what will happen to prices if Macro Man is wrong and the UK ever does manage a period of strong self-sustaining growth.

And so your author cannot help but think that at some point, the Guv’nor will be for swerving once again. Whether that happens in 2010 is of course a matter for debate, and Macro Man doesn’t have a strong view on the timing. Merv has, after all, demonstrated in the past that he can remain irrational longer than “haters” can remain solvent. But with inflation set to exceed 3% and the Bank not particularly interested in lifting a finger, Macro Man cannot help but think that Gilts make an attractive short here, especially as a spread trade against something like Bunds.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply