I spent some time today updating my Treasury yield curve and inflation model. Anytime a new Treasury note/bond is issued, or we get a new CPI figure, or a coupon payment date passes, the model must be updated. Though I made some technical improvements to the program at the same time, what impressed me was the change in the forward inflation curve since I last wrote on the topic less than a month ago.

The big change is that inflation expectations rise continually out to 2038. Now the TIPS curve only goes out to 2032, so the extrapolation should be discounted. But the last time I wrote, inflation expectations peaked in 2022. That is a significant change. Investors have bid up the prices of long duration TIPS, to the point where I would be skittish about buying the long end of the TIPS curve.

Okay, let me post the graphs:

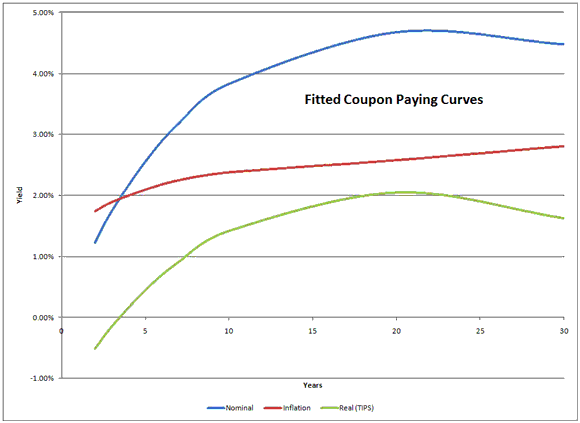

Using closing prices, here is my estimate of the coupon-paying yield curve:

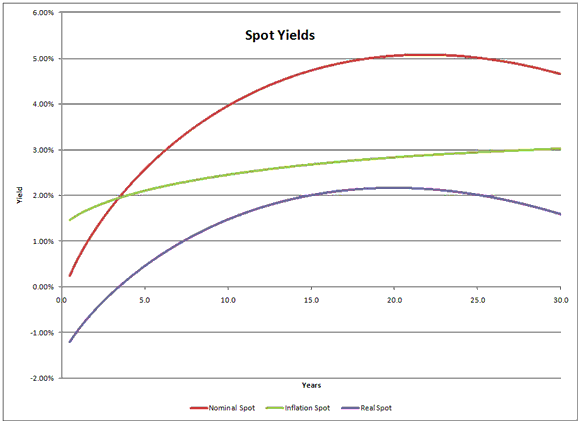

And here is the spot curve (estimating where zero coupon bonds would price):

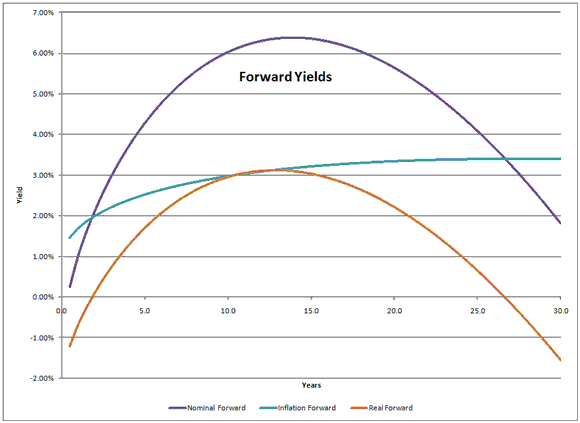

And finally, the forward curve, which estimates the expectations of future short-term rates, inflation, and real rates:

My model uses the whole Treasury and TIPS markets to estimate yields and inflation expectations. Here is what is notable:

- Inflation expectations on the long end have risen considerably over the last month.

- I suspect that the US Treasury will be able to issue 30-year TIPS at yields lower than 20-year TIPS. The new 30-year TIPS issue in February will prove me right or wrong.

- Real forward yields are lower than zero 27 years out — that is unlikely. I would expect nominal forward rates to rise on the long end.

There are at least two ways to view this situation:

1) Investor inflation expectations have overshot, and it is time to sell long TIPS and buy long nominal bonds, as long-term inflation expectations may fall in the future.

2) Time is running out — rapidly rising long-term inflation expectations indicate that the average investor does not trust monetary policy to succeed over the next 20+ years.

What would I do here? I would hedge my bets, and buy some long Treasury zeroes (not a lot), mostly intermediate-to-long TIPS, and some short nominal Treasuries. I would bias the portfolio in favor of bonds that are seemingly underpriced.

The hedged position is because I don’t know which direction the US Government and Fed intend to go with policy. They likely have no idea as well; this is a tough situation.

On the deflationist side there is Hoisington, Gary Shilling, Carpe Diem.

More inflation-oriented are Greg Mankiw, Tim Duy, and Pimco. But I don’t see anyone of significance screaming for high price inflation in the long-term future. Yes, that is the default view of much of the financial blogosphere, but the US Government had that option in the ’30s. It would have made things a lot easier if they had done it, but they didn’t do it. They acted in the interests of the wealthy, rather than the interests of the economy as a whole.

That’s what makes my model interesting. It shows that there is a lot of demand for long TIPS. If the US Treasury thinks it can get things under control, the rational thing to do is to stuff the long TIPS buyers with as much product as they can gulp before it becomes obvious that low inflation will continue because the government will soon balance the budget and pay down debt, as they did after WWII.

But if the US Treasury can’t get things under control, the long TIPS buyers will do well, as they have the most sensitivity to rising forward inflation expectations.

Where do we go from here? My guess is slowly rising inflation with a weak economy. But so much depends on the rest of the world, that I hold that opinion skeptically.

Disclosure: I own some of the Vanguard TIPS fund [VIPSX]

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply