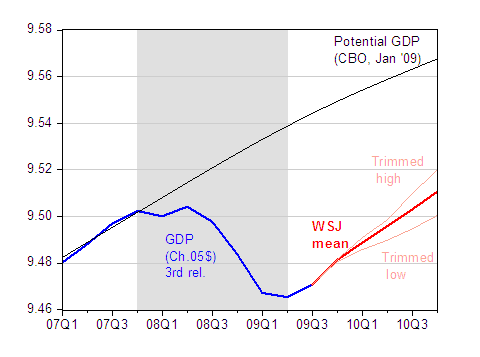

The WSJ survey for January is out. Growth is predicted to be fairly rapid, but hardly torrid, in 2010, with q4/q4 mean estimate at 3.0%. Here’s the mean forecast of the log level of GDP, and the trimmed high and low forecasts.

Figure 1: Log GDP in Ch.2005$ (blue), mean WSJ forecast (red), and 20% trimmed high (pink) and trimmed low (pink) forecasts. Trimming removed the top 6 and bottom 6 forecasts out of 56 responses. NBER defined recession dates shaded gray, assuming recession end is 2009Q2. Potential GDP from CBO obtained by multiplying January 2009 estimate in Ch.2000$ by 1.14. Source: BEA 2009Q3 3rd release, WSJ January survey, CBO, NBER, and author’s calculations.

The 09Q3 gap of 7.3% (log terms) shrinks to 5.7% in 10Q4 according to the WSJ mean forecast. The (trimmed) high forecast implies a 4.8% gap, while the low forecast, a 6.7%.

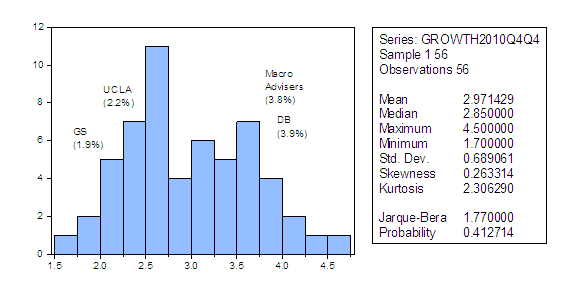

One interesting aspect of the survey is the fact that the q4/q4 2010 forecasts are bimodal.

Figure 2: Histogram of 2010 q4/q4 growth. “GS” is Goldman Sachs/Hatzius; “UCLA” is UCLA/Leamer &Schulman; “Macro Advisers” is Macroeconomic Advisers/Prakken & Varvares; “DB” is Deutsche Bank/Lavorgne. Source: WSJ January survey.

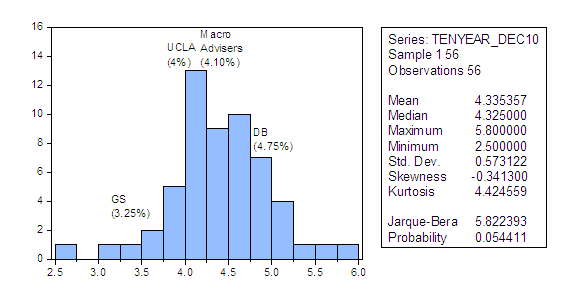

What about worries about a collision of deficits and demand for Treasuries? The mean forecast is for a 10 year t-bill rate of 3.98% and 4.34% at end June and end December, 2010, respectively. The current ten year rate is 3.67.

Figure 3: Histogram of end-December 2010 ten year t-bill rates. “GS” is Goldman Sachs/Hatzius; “UCLA” is UCLA/Leamer &Schulman; “Macro Advisers” is Macroeconomic Advisers/Prakken & Varvares; “DB” is Deutsche Bank/Lavorgne. Source: WSJ January survey.

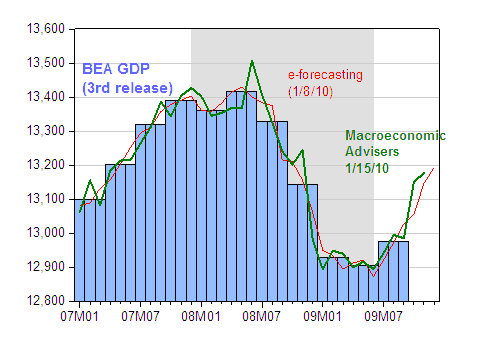

Finally, Macroeconomic Advisers released its estimates for December ’09 GDP.

Figure 4: Real GDP, 3rd release for ’09Q3, in billions of Ch.2005$ SAAR (blue bars), e-forecasting release of 8 January (red line), and Macroeconomic Advisers release of 14 January (green line). NBER defined recession dates shaded gray, assuming recession ends in 2009M06. Source: BEA, e-forecasting, Macroeconomic Advisers and NBER.

On a slightly different note, in terms of thinking whether output volatility will be substantially higher in the future, my coauthor Oli Coibion and his coauthor Yuriy Gorodnichenko have a VoxEU piece out which runs counter to the views of those who have declared the end of “The Great Moderation”.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply