Most mornings, Macro Man has a pretty good idea what he wants to right about, and tries to insert a theme underlying all of his comments and observations. Occasionally, however, he is somewhat bereft of inspiration….those days usually produce a “fun” post like 20 Questions or something. Sadly, Macro Man doesn’t even have the inspiration to rustle up 20 vaguely interesting questions, so he is sitting here this morning, scratching his head about what to write.

Today is the first equity option expiry day of the year, of course, and usually that means fireworks. But for some reason, unbeknownst to your author, the slate of earnings releases has shifted back, so we have relatively little information to go on. Normally, you’ve had a healthy dose of earnings announcements by the time options roll off, and Citi, for example, has usually announced on the morning of expiry- an easy one to remember, given the fireworks associated with the once-mighty C’s releases over the past couple of years.

Macro Man isn’t sure what’s happened…it’s a bit of a head-scratcher. OK, Intel beat expectations last night, but come on: they’ve very 1990’s. So if it seems like stuff has been relatively quiet, there is perhaps good reason: we’re getting less info than usual this time of year. (In fairness, there’s been a little bit more sizzle in Europe, but only just.)

To be sure, we do have one bank releasing before expiry today: the House of Morgan (and Chase, and Chemical, and Manny Hanny, etc. etc.) And while those numbers might be interesting, JP has of course been one of the rocks of the banking industry throughout the crisis, with less earnings vol than most of their competitors. And in any event, the real interest in the banking sector is now on earnings well forward, after Obama proposed a fee (not a tax, no sirreee, a fee, dammit!) on large banks’ liabilities to pay the tab for the bailout.

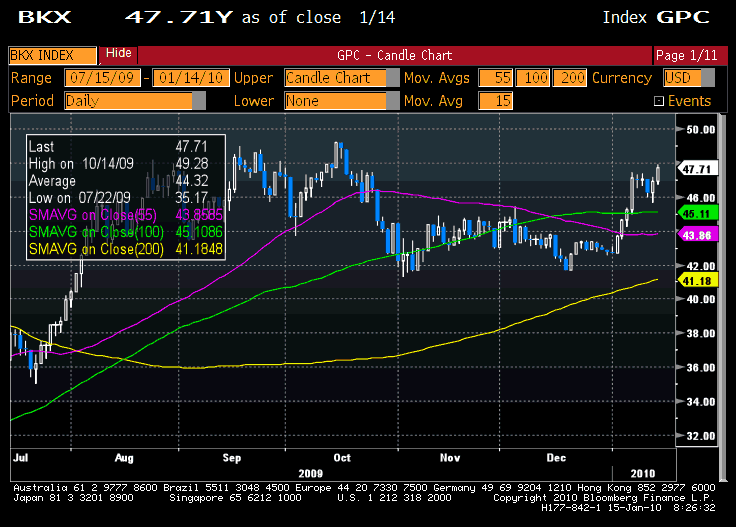

One early-cut analysis that Macro Man saw suggested that it would cost the likes of C, JPM, BAC, and GS in excess of $1 bio per annum for the next decade. For sure, in his conversation yesterday with a mate at one of those shops, his interlocutor suggested that everyone took the proposal seriously and was pretty bummed out. In any event, after this (perhaps justified, but clearly populist) measure was announced, the BKX naturally surged. Another head-scratcher.

(click to enlarge)

One somewhat puzzling development that has subsequently been cleared up (a bit) was the euro’s painful decline in December. China released data suggesting that FX reserves rose by “only” $11 bio in December. While the valuation adjustment from the euro’s decline will artificially depresee that number, it nevertheless suggests less piss-taking than usual in December…and thus less reason to play with EUR/USD like killer whales play with baby seals.

While the euro has tried mightily to recover thus far in January, the results have been tepid at best. JCT offered little support yesterday, particularly vis-a-vis Greece, where he essentially said “you’re on your own, sunshine” while downplaying the self-sustainability of the Eurozone recovery.

This morning, the EUR has been buffetted by the peculiar rumor that Angela Merkel will resign. There’s no obvious source, rhyme, or reason to that story, so naturally Macro Man has been left scratching his head once more to figure out why it’s out there to begin with.

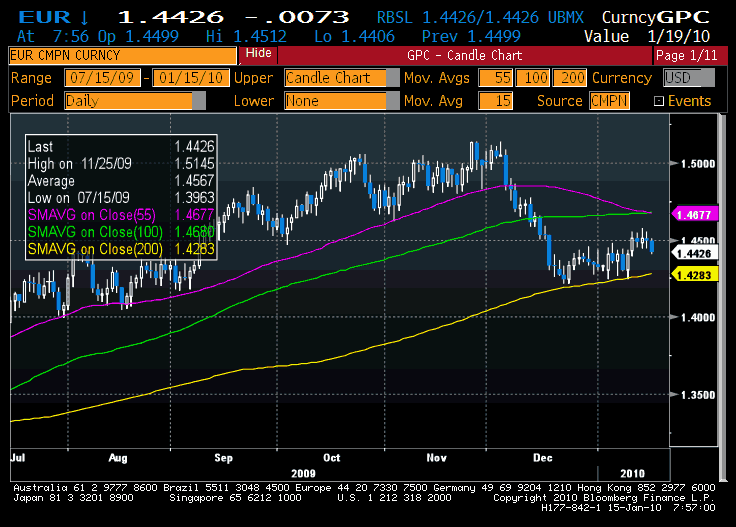

(click to enlarge)

You can observe from the chart that the 200 day moving average has provided good support for EUR/USD over the past month, much as the 55-day MA did for most of H2 2009. Should the 200 day mover break, it probably won’t take much head-scratching to figure out what the market will do….

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply