I finished the first phase of a project today. But first let me tell you a story. It was 1990, and the Society of Actuaries Investment Section was holding a conference. It was a great conference; I still have the binder from it. There are few meetings from twenty years ago that still have relevance for me.

One of the presentations was by Stanley Diller, a managing director of Bear Stearns, who insulted all of the actuaries at the conference by telling them the the insurance industry was dead wrong for talking about yields and spreads. Everything was duration and convexity, and those that did not understand that would lose.

He ended his presentation suddenly, did not take questions, and stormed out of the room. I’m not sure why, but I had a seat in the back, and intercepted him. I said, “You can’t just say this and not give any justification for your views, how do you back it up?” He thrust a business card into my hand and said, “Call my secretary, she will send you the info.” He stormed away.

The next day I called the secretary, and she told me she would send the information. Two days later, I had it, and a few days later, I had replicated it in my own model.

Since then, I have used the model profitably many times. Today I use it to describe the yields in Treasury Notes and TIPS. I have used it to produce an estimate of future inflation expectations.

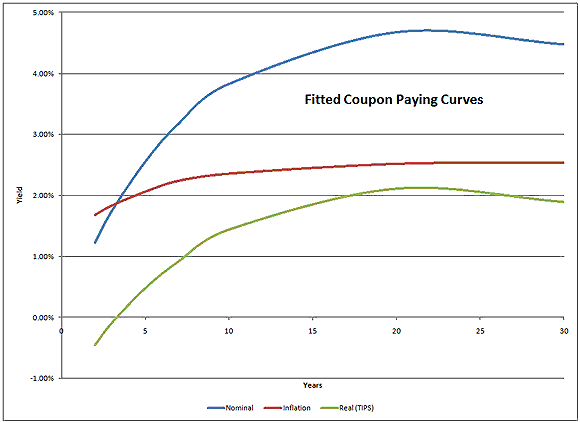

Using closing prices, here is my estimate of the coupon-paying yield curve:

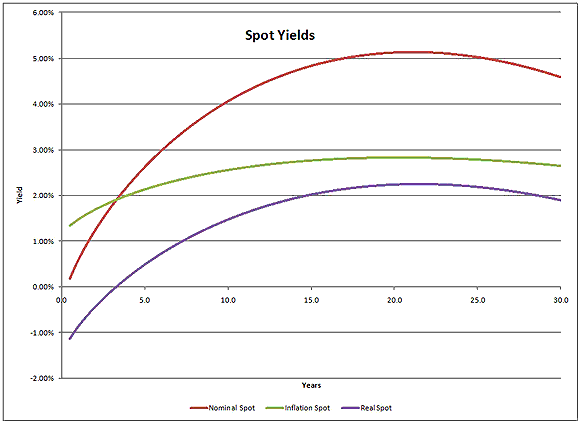

And here is the spot curve (estimating where zero coupon bonds would price):

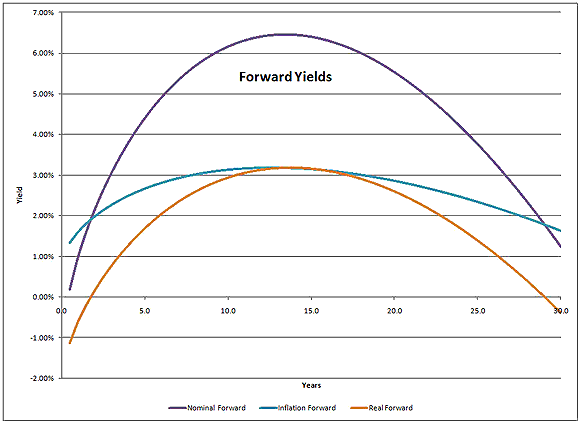

And finally, the forward curve, which estimates the expectations of future short-term rates, inflation, and real rates:

Pretty neat, huh? Let me tell you a little about the model:

- Values are as of the close 12/22/2009, but the model can be run in real time.

- It is estimated from the full coupon-paying Treasury Note and Bond markets — over 200 bonds in the model.

- The model estimates a nominal spot curve, fitting prices with 4 parameters, over 99% R-Squared.

- The model estimates a forward inflation curve, fitting TIPS prices with 4 parameters, over 99% R-Squared.

- The two models are estimated jointly, through nonlinear optimization.

- The model has one constraint — nominal spot yields must be positive after 4 months.

- Every other curve is derived from those two curves.

What are the useful things that we learn from the model?

- There are mispricings in the Treasury and TIPS curves, but they are typically small, and would be hard to make money off of. That’s demonstrated by the high R-Squareds.

- The Fed has achieved its goal of making real rates negative in the short term.

- And, has made made nominal rates negative for some very short instruments inside 6 months of maturity.

- Inflation expectations start low, and peak around 2022, then tail off.

- Long term inflation expectations are still under 3.5% — ignore the portion of the inflation and real curves after 23 years, they are extrapolations.

- Implied short-term real yields go positive in 2011, peak in 2024 and tail off thereafter.

- The nominal forward curve is steep as a mountain on both sides. Though there is a lot of fear over what will happen over the next 12-14 years, those fears have not been built into the prices of longer-dated Treasury securities.

- The nominal spot curve peaks after 22 years — in my experience, that is normal, and is a reason why longer nominal note yields decline. US Treasury — take note.

- Inspecting the differences between coupon-paying yields on Treasuries and TIPS makes inflation expectations look more tame than they really are. Federal Reserve — take note.

- 30-year TIPS would likely fund cheaper than 20-year TIPS — US Treasury, take note. The scarcity value would help as well.

This is just the beginning. I’m not planning on writing about this every day, but I should be able give you some updates every now and then. Hopefully the firm I work for should be able to benefit through research that this enables me to create for institutional clients.

Full disclosure: I own shares in Vanguard’s TIPS fund. And truth, we all own Treasuries somewhere if we look deep enough.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Nice work! So what is the takeaway? Invest in TBT or JNK? Buy TIPS? Data good, info better.

This is fantastic research and very useful. Thank you for publishing it and I look forward to the updates. It accords with the proprietary model of interest rate projections I saw yesterday from a Canadian Bank.

Isn’t the takeaway to allocate some to TBT and more to TIPs? I would also look at Canada’s XRB real return bond ETF. Keep your bond ladders short and stock up on 10’s when they tank.