Ben Bernanke made a very revealing slip this week: he admitted he had refinanced his optionARM mortgage with a 30-yr fixed rate at 5%. He said he had to, as his loan had “exploded“, but it appears he was engaged in FedSpeak obfuscation: an analysis of his ARM showed it would not have exploded, and that he just refied at a higher rate! So why refi? The implication is he knows higher mortgage rates are coming, and wants to lock the rate in.

The implication of this unintended admission is: deflation!

For those of you who believe that inflation, even hyperinflation, is ahead, and take confirmation in the recent blip up in PPI and CPI, this month’s EWT is required reading. The deflationary forces are growing rapidly.

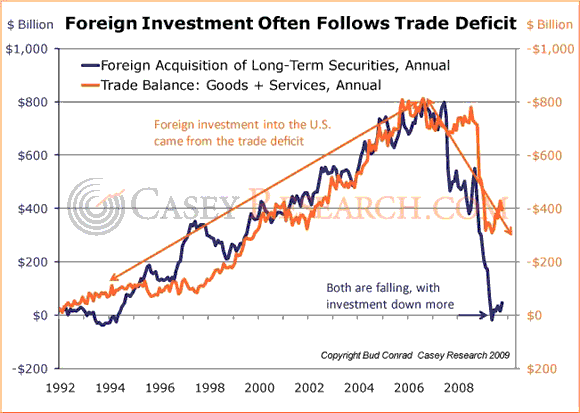

Normally higher rates presage either a recovery (demand for longer term loans) or inflation. We are not in normal times. Higher rates are the cost of financing huge US deficits. Bernanke is trying to exit QE, which was used to keep rates down, except he may be boxed in due to a deficit of foreign buyers. As this chart shows, foreign investment in long-term Treasuries is falling, as is the trade deficit.The trade deficit is the other side of a Dollar surplus (since the deficit results in Dollars flowing out). As the trade deficit shrinks, fewer Dollars are falling into foreign reserves, and hence they have less need to buy Treasuries to recycle them back. The Bank of China has admitted such.

At the same time they are pulling back, we are seeing more and more short-term Treasuries being placed, which need to be constantly refinanced. Think we can keep pushing short-term T-Bills and rolling over prior issuances? This makes it extremely problematic to exit QE, since if short term rates rise, we have a serious problem with the cost of financing the deficit.

Bernanke has focused most of the Fed’s activities in the past year on keeping mortgage rates low. He knows that the US won’t come out of a recession without a rebirth of housing; and he is painfully aware that most of the toxic waste clogging bank balance sheets are based on mortgages. Hence both to restart the economy and repair bank balance sheets, he has tried to keep rates low and spur the housing sector. Now he refinances his cheaper ARM! The end is nigh to QE.

To date his QE has not been inflationary. He hasn’t really created new money; he has swapped assets for reserves. He expected banks to then lend, because of reducing the uncertainty of those assets, but just as in the 1930s they have sat on those reserves. The excess liquidity has gone to Wall Street, not Main Street. This won’t change as he swaps those bad assets for Treasuries. What will change as he exits QE is the unleashing of deflation.

Robert Pechter was one of the first to predict a crushing deflation is ahead. His case is summarized here. He is now being joined by others, including Gary Shilling (who has been on this for a while) and Harry Dent (who has called this decade really well). In this EWT, Prechter continues building a case he started last month of deflationary forces gathering before a storm that should hit in late 2010 or in 2011. His case has two primary arguments and a prediction:

The Fed May Have Made a Fatal Mistake

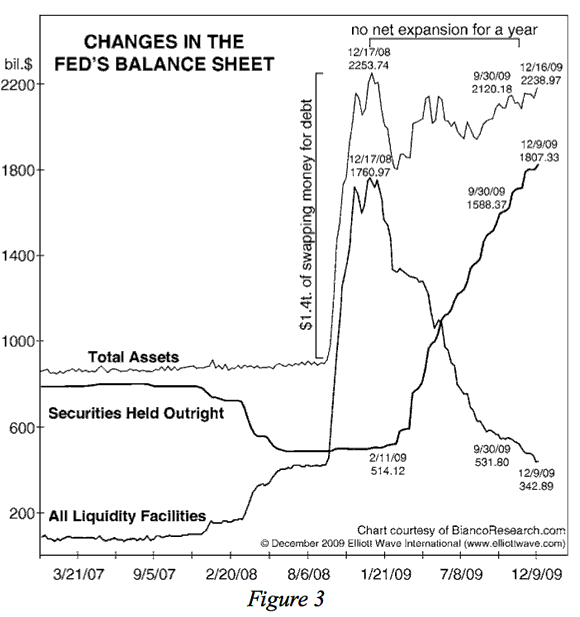

The EWT explains that the Fed first used TALF to back hedge funds and similar who invested in consumer debt, backed by collateral; but the collateral turned out to be bad. The Fed now owns a deserted shopping center in Oklahoma City as well as some bankrupt hotels. Thanks, Bear Stearns! So the Fed switched to directly buying mortgage-backed securities (MBS) in swaps with banks. It has since swapped (ie. bought) over $1T of MBS. See chart, from the EWT:

The purpose was to keep mortgage rates low, but “in buying up the mortgages, the Fed may have done something stupid.” When shoring up the banks or hedge funds, the Fed could always refi those loans in such a way that would force the banking entity to sell the toxic assets to repay. Now it is stuck with the direct collateral, the very thing it was trying to avoid after TALF! If the Fed is stiffed with losses, the member banks will have to make good since banks are required to cover the Fed’s losses. The banks will become more cautious, lending less, which is deflationary.

Congress is a Financial Weapon of Mass Destruction

Prechter lists a growing number of actions Congress is taking which all have the effect of reducing lending. If you read Karl Denninger, you know this is a good thing in general. History will look back and ask what sort of theoretical nonsense led us to try to borrow our way out of a credit bubble – are we that much in thrall to a long-dead economist?

Nonetheless, this good thing will be deflationary because it reduces debt. Let’s step back. Many folk think that the Money Supply is the monetary base plus maybe a few other things like demand deposits and sweep accounts that can be rapidly turned into money via a check. The Austrian debate which money aggregate is real money, but this misses the larger problem: the inflationary or deflationary forces are based on the broadest view of money, which includes credit-money not just real-money. Credit can be turned into purchasing power, and because of fractional reserve banking, banks can lend well in excess of their reserves of real money. We have around $50T of credit on top of $2T of real money. It is the velocity of that $50T, and its rise and fall, that drives inflation or deflation. Hence anything which reduces the turnover or velocity of money, or reduces its stock, is deflationary.

Congress is finally facing up to fixing the financial crisis, not healthcare or global warming or other far off (or fake) crises. Their acts almost across the board will reduce lending and cause debt to be written off. The EWT has a long list which I won’t repeat here. Suffice to say they deter the whole food chain of lending. The list shows how dysfunctional and ineffective Congressional acts have been so far. My favorite examples:

- The original $300B mortgage bailout, and the recent $75B Obama program, have only “helped” 1700 homeowners so far. To fix it, they want twice daily reports on progress from the banking workout teams! I am sure that will work … the teams weren’t that effective anyway dealing with real problems, so why not pull them back to the office to fill out meaningless paperwork?

- The bailouts seemed destined to lose $30B on autos and another $30B on AIG. Such a deal!

The FHA Seems Doomed to Fail, Spectacularly

While attention has been focused on Fannie and Freddie, under Obama the FHA has become the lender of mass destruction last resort to housing. Even though 24% of its loans from 2007, and an astounding 20% of its loans from last year, are in default, the EWT notes with emphasis that it is “still writing mortgages at a frenetic pace”, four times faster than in 2006 at the peak of the housing bubble! Down payments are as low as 3.5%, and the more distressed the area, the higher the FHA percent of the market. This is clearly madness. The FHA insures $675B of mortgages. These loans are packaged with others and run through Ginnie Mae.When this mess blows up, the taxpayer will be on the hook.

Barney Frank justifies the horrifically high percent of bad loans as “policy” to keep housing from falling faster! Is he that big a fool? Maxine Waters recognizes that “without FHA, there would be no mortgage market right now.”

Exactly right! So what to expect?

- Fed reduces QE, rates go up, housing goes back down, economy gets even more sluggish, FHA defaults get too high to bear, housing becomes a market of distressed sales and foreclosures.

- OptionARMs begin to “explode” and the second wave of defaults washes over the system.

- Congress passes even more frenetic acts to “fix” the problem. As history shows, when you regulate something, you get less of it.

- As the mortgage problems accelerate, the Fed’s balance sheet becomes suspect, and losses mount. It no longer can “save” the system.

Yikes! Then what do we do?

Maybe the demise in 2012 ‘predicted‘ by the Mayan calendar is of the Fed, not the Planet.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Not bad, although I’ve been calling deflation for a year and a half, predicated on an obvious collapse in demand. Nevertheless, you are quite naive yourself when you suggest Bernanke has been quite naive himself.

There is no naivete involved. We are simply in the next phase of liquidation. I am in the camp which says Bill Gross moving into cash and the Citi stock thang, mean these insiders have just received a piece of disastrous news. Result? The powerful forces in the country are stepping up liquidation.

This doesn’t so much mean accelerated collapse in demand, as you are suggesting, because collapse in demand is in the lead at every moment when there is liquidation.

What it DOES mean, however, is that we are rapidly moving toward a more or less coordinated global sovereign default. The template for this is the way the U.S. treated the GM bondholders.

PIMCO a money market fund?!?

If they’re lucky!!!!!

But more seriously, what is accelerating and most disturbing, is a collapse of the supply chain. This is a result of liquidation, just as it was during the Depression.

However, we didn’t learn the lesson of supply chain collapse because 3/4 of workers had jobs through the Depression. That is not going to be the case here.

The next thing I suspect, once unemployment really starts surging around March or April, is a collapse of the political system. A crisis in which political decisions can’t be made. One wants to say, Weimar Republic 1932. However, a political crisis always accompanies liquidation, because it hits unevenly and so coalitions can’t stay together.

Blame suburbia. As long as unemployment among BA+ workers isn’t 40%, nothing will change. That is, no preventive measures can be taken. None have been taken so far.