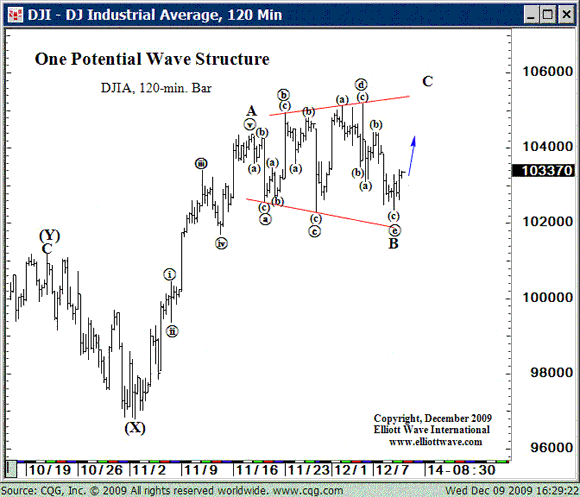

The bounce off the opening low today may signal the beginnings of a multi-week Santa Rally. We have been following a count by EWI, that we are in a wave 4 expanding triangle. It required a final leg down to around Dow10231, and it got to 10236 today. Tonight’s STU thinks this could be good enough to conclude the sideways motion for the past four weeks. The wave structure would also allow for a final jink up and jive down to below 10231 as well.

Such a jive down could get out of control, given other items they are watching, including sentiment, volume and overseas markets. They too have been watching what I pointed out in the prior post: the Dubai disease is spreading in Euroland, to Greece, Spain, Latvia, Lithuania, and possibly even Austria.

Global equity markets are beginning to diverge, with many falling and some (like Greece) crashing. This sort of divergence is to be expected near a top.

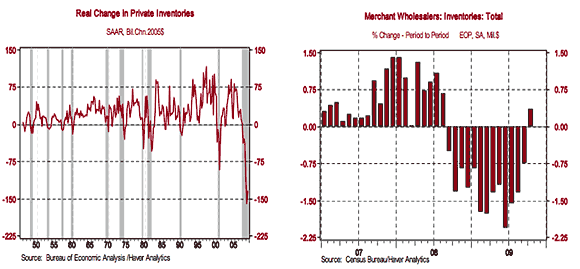

Back in the USSA (the extra S for Socialist), markets may have popped today on some good inventory news, albeit from Oct data. Inventories had fallen the most since the 1930s, but have now begun climbing back. See charts from Northern Trust’s analysis:

The caution is this restocking was expected, and was used to prepare for the holiday sales season. It was also driven by cash4clunkers, and after that treat we were in for the trick of how to maintain car sales. They plummeted after C4C then have stabilized a bit.

After the holiday sales season, inventories can be expected to slacken again.

We might get a hint in early January, as new product needs to be in the pipeline well before December. We will get confirmation in Feb when the Dec numbers come out. The timing of these later reports support the scenario of a Santa Rally followed by topping in January or at worst into February.

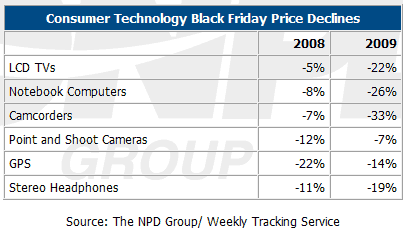

Another bit of caution comes from more solid Black Friday retail numbers than the pumpers’ flash estimates, and as Karl Denninger so elegantly puts it, they suck:

The NPD Group’s Weekly Tracking Service, the industry source for actual point-of-sale data (POS) from Black Friday. Total revenue for the week of Black Friday was slightly more than $2.7 billion, down 1.2 percent from 2008, but an improvement over the 3.4 percent decline noted last year.

Worse, prices are down considerably. This supports my thesis that retail will be late and discount-driven:

We are also seeing some reconsideration of the November “good” jobs report. From DowJones MarketTalk, we have this confession:

So even if you buy into Friday’s jobs report, the fact remains that hiring has not picked up, which is confirmed by the fact that long-term unemployment continues to rise.

And if you don’t buy into Friday’s report, well, you’re not alone. I’m still dubious. And certainly Fed Chairman Ben Bernanke didn’t think it was strong enough to get him to even hint that he might lift interest rates off the floor. And other folks are still deconstructing it.

East Shore Partners’ Frank Veneroso, who initially called the November jobs report “super strong,” is rethinking that position today. He was initially impressed by the increase in the work week and the upward revisions to prior months. But “after thinking about this for several days, I realize I may have overstated the implications for recovery strength.”

We are still not done with this retail season, and the jobs report may not be that good but it isn’t that bad either. In general we see signs of a real recovery, and short of that certainly are falling less fast. The pundits are in effect scratching their heads. All this seems to set up the Santa Rally followed by a January disappointment, probably confirmed in early Feb with a bad jobs report after all the seasonal adjustments are done, and maybe a weak inventory report as well.

In the meantime, Amazon comes out as the best online shopping site, according to the WSJ. Don’t worry, be happy! Shop online!

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply