Today’s 10% unemployment number sparked a rally at the open. News like this can ratchet a market momentarily, but then the sober analysis follows. As I write this, the market already has largely faded the pop. Neely put out a bulletin this morning to that point, suggesting the rally be shorted.

In my recent post Is Unemployment Sending the Wrong Signals? I noted that last month’s 10.2% rate was spurious – unemployment was essentially flat, but seasonal adjustments made it look worse. The primary adjustment this time of year is for temp workers in retail, and since we have many fewer retail outlets, the adjustments will overstate unemployment.

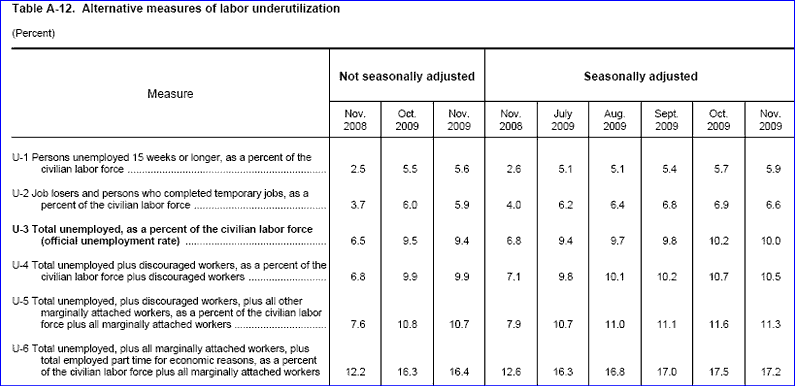

Similarly, this report is can be misinterpreted, as the market did at the open. Mish has provided a good table showing unadjusted and seasonally-adjusted numbers. Looking at U3, we see that the raw number last month was 9.5%, before seasonal adjustments took it to 10.2%. This morning’s raw number is 9.4% before adjustment to 10%. Even that raw number has data massaging in it. We actually lost about 69K jobs, with temporary retail and healthcare jobs ameliorating a larger decline for a net 11K loss.

click to enlarge

Jesse notes how the Labor Dept. has a running birth/death adjustment (for companies not people) that also may ratchet these numbers after the holiday retail season.

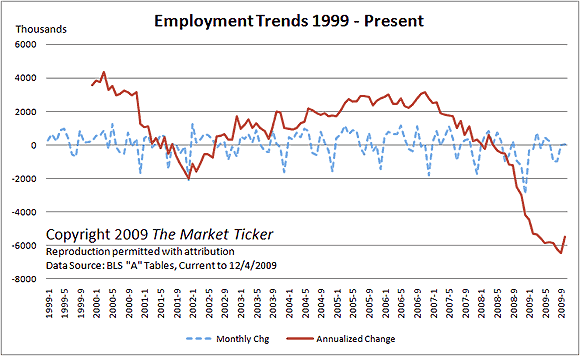

Overall, however, this report has good news in it: the job drop may be bottoming. Karl Denninger runs this chart showing the change of trend on a YoY basis:

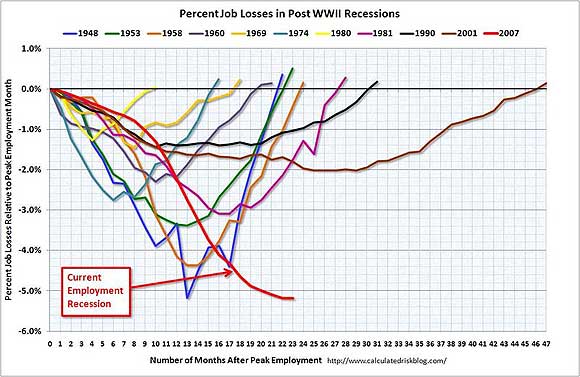

Calculated Risk has more on this theme. As you can see in comparisons with prior recessions, our current one is long and deep, but appears to be bottoming, albeit slowly. What to watch: what happens in the January report (which comes ou t in Feb) ater the temp workers for retail roll off.

The most interesting take on this: the Fed Funds futures have “come to life”, possibly due to a better jobs picture in 2010. Better jobs = rate rise = bearish for stocks. So it goes n the twisted logic of Wall Street.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

It’s probably not a good idea to use ANY government statistic. For example, the average income of 500000 California farm workers is BELOW the Federal poverty rate. Should these people be considered “employed?” Should anyone working at below the Federal poverty level (which is already criminally low) be considered “employed?” Of course they are now, by the U.S. But it gives a false idea of the economy, and you and organizations such as Shadowstats, should have nothing to do with it.

Better develop a “maintenance” rate, which includes the standard of living. In short, what do people actually DO and how do they actually LIVE?