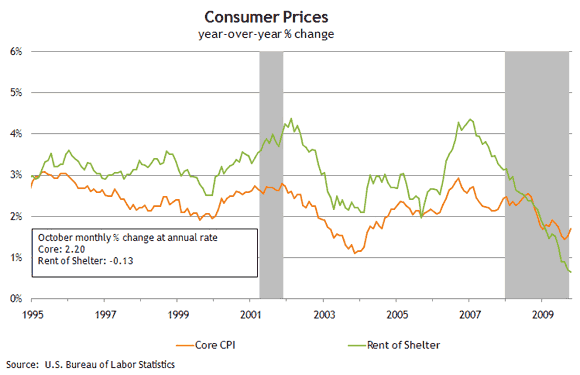

Two reports released this week remind us of the difficulties still confronting the residential real estate market. First, the consumer price index (CPI) showed continued moderation. Yes, the overall number was up 3.4 percent on a monthly annualized basis, and even the core measure ticked up 2.2 percent. But over half of the core rise was related to rising new and used car prices following the expiration of the cash-for-clunkers program. The Cleveland Fed’s median CPI, which isn’t influenced by these outliers, was up only 1.2 percent and still suggestive of some considerable disinflationary pressure.

What does the CPI have to do with housing? Well, the shelter component of the index, which is derived largely from rents, was unchanged and has risen only 0.7 percent over the past year (see chart below). This performance represents unprecedented lows for this, the largest of the major CPI categories, and is a good indication of the downward price pressures being felt in the residential housing market.

More directly related to the state of housing was Tuesday’s report on new home starts, which dropped sharply. Starts fell 10.6 percent in October, a surprising decline for a series that appeared to bottom out in April and stabilize in recent months. But perhaps a few bumps along the road to recovery are to be expected.

Some say that the falloff in new home construction last month was likely the result of uncertainty over the continuation of the first-time homebuyers program. That’s a possibility, but here’s something else to consider: There may be a lot more housing inventory out there than the official numbers suggest.

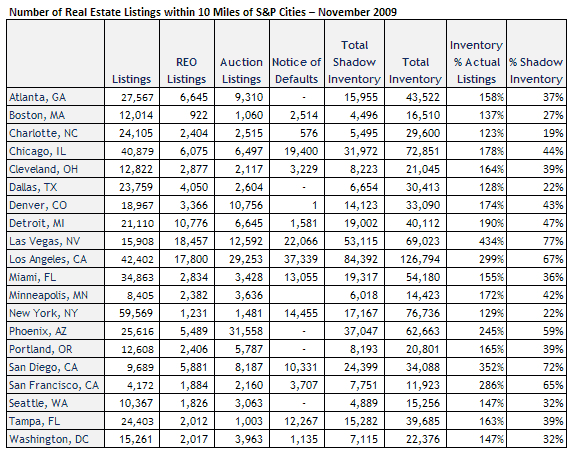

In recent months it appears that home prices as measured by the S&P/Case-Shiller Index have stabilized and begun to improve while home sales have picked up notably and listing inventories of new and existing homes have fallen. However, these listing inventories fail to capture a large share of the market including homes for sale by owner, potential buyers on the sideline waiting to see improvement, and foreclosure properties that have not yet made it to market but likely will eventually.

RealtyTrac reported that foreclosure activity slowed for the third straight month in October, down 3 percent from the previous month. However, those receiving notices of defaults increased 2 percent after declining 12 percent the prior month. Bottom line, foreclosure filings remain at high levels.

Amherst Securities released a report in September that took a stab at calculating the current shadow inventory of foreclosure properties using the Truilia listing database. In light of increased sales and slowing foreclosure filings, let’s see how things are going:

Comparing the September report and the November numbers, we see that listing inventories declined 3 percent, which is to be expected with the pick-up in existing home sales numbers that the National Association of Realtors has been reporting in recent months. However, the shadow inventory of foreclosed homes grew by 9 percent (real estate owned, or REO, properties grew by 4 percent), helping to drive total inventory up 2 percent from September to November.

Homebuilding was a driving force in the economy in the years leading into the recession. Looking forward, though, the homebuilding industry is continuing to face significant obstacles, including inventory challenges. Those challenges translate into homebuilders being understandably wary to move ahead on new construction until foreclosures and REO inventories measurably subside. Thus, the homebuilding challenge continues.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply