I’m not sure. My version of the real business cycle model (some of my academic papers on it are here and here, and I began applying it to this recession about a year ago, such as here and here) does not give a definite answer, but it does drastically narrow the possibilities.

My model has no adverse productivity shocks, no shocks to capital markets (these variables just reaction to events in the labor market), no monetary policy, and no fiscal stimulus. Simply put: I view this as a one shock recession, and the labor market is ground zero for that shock.

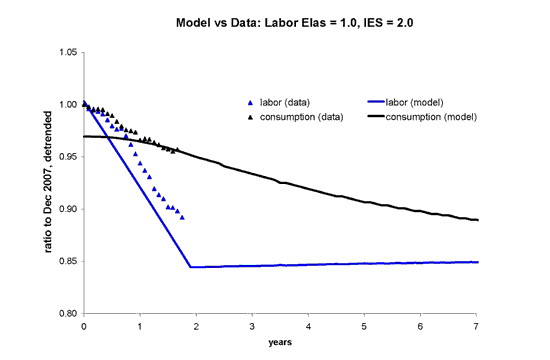

One version of the model has a labor market distortion that gets progressively worse for two years, at which point it remains at that higher distortion forever. Specifically, the average marginal tax rate ultimately increases about 10-15 percentage points (more accurately, the after tax share is cut by 22 percent), but it takes 2 years for the full marginal tax rate hike to occur.

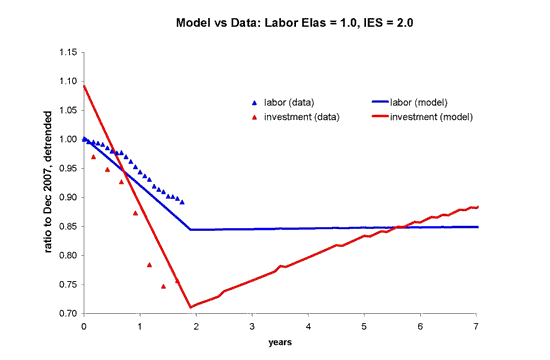

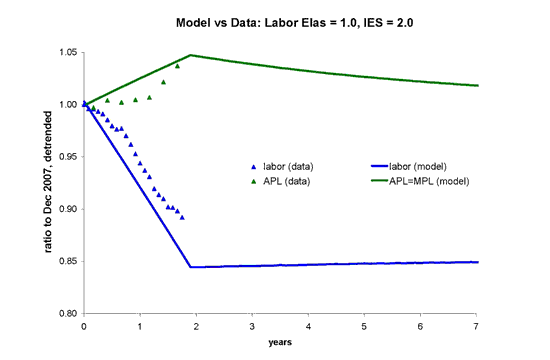

The model and data are shown below. Note that latest 12 months (4 quarters) of the data were not available when I first began writing about this model.

[APL is real GDP per hour worked — labor productivity — which in the model is in fixed proportions to the marginal product of labor]

The good news from this first scenario is that the labor market will stop getting worse in 2010 (ie, employment and hours will stop falling further below trend). The bad news is that aggregate hours will never return to that previous trend, even part way. Consumption will ultimately be further below trend than it is now.

I am still working on it, but I think there’s another version of the model that would fit the same data: the labor market gets even worse for a couple of more years, but eventually will be closer to the previous trend than we are now. The bad news from this second scenario is that the labor market will not stop getting worse until beyond 2010. The good news is that consumption and aggregate hours will eventually return to their previous trends, at least most of the way.

Either way, the inference I am making from consumption behavior — it has fallen a lot by historical standards, but far less than labor has fallen — is that the present value of lost labor is great, but much of that loss labor has not yet occurred. Whether the remaining lost labor is spread over the infinite future (the first scenario above), or concentrated in the next couple of years (the second scenario above), I do not know.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

By not taking into account monetary policy you might as well be writing a fiction. What ever you are saying is completely meaningless.